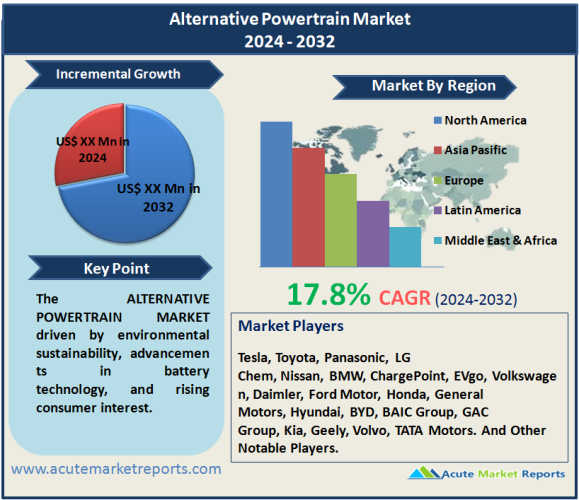

The alternative powertrain market is expected to grow at a CAGR of 17.8% during the forecast period of 2026 to 2034, driven by environmental sustainability, advancements in battery technology, and rising consumer interest. Challenges in infrastructure development present a significant hurdle that needs to be addressed for the market to reach its full potential. The segmentation by powertrain highlights the dominance of battery electric vehicle powertrains, while hybrid powertrains maintain a significant market share. The market dynamics for components indicate a shift towards increased demand for battery management systems and on-board chargers. Geographically, North America leads in 2025, with Asia-Pacific expected to surpass in CAGR. The competitive landscape showcases key players adopting strategic approaches, with Tesla, Toyota, and Panasonic at the forefront. As the industry progresses from 2026 to 2034, the alternative powertrain market is poised for continued growth, playing a crucial role in shaping the future of sustainable transportation globally.

Environmental Sustainability and Regulatory Pressures

The increasing emphasis on environmental sustainability, coupled with stringent regulatory pressures, is a significant driver in the alternative powertrain market. Leading automakers, such as Tesla and Toyota, have strategically positioned themselves by prioritizing electric vehicles (EVs) in response to global efforts to reduce carbon emissions. For example, Tesla's success in the electric vehicle market is evident in the surge in demand for its models, driven by environmentally conscious consumers and government incentives. Regulatory measures, such as emission standards and incentives for electric vehicle adoption, further propel the market's growth, creating a conducive environment for alternative powertrains.

Advancements in Battery Technology

Technological advancements, particularly in battery technology, play a pivotal role in driving the alternative powertrain market. Companies like Panasonic and LG Chem are at the forefront of developing high-performance batteries that enhance the range, efficiency, and overall appeal of electric vehicles. The evolution of lithium-ion battery technology, as witnessed in the Tesla Model S, has significantly contributed to the increased adoption of electric powertrains. The continuous innovation in battery technology addresses concerns related to range anxiety and charging infrastructure, fostering consumer confidence and driving the market's expansion.

Rising Consumer Interest and Awareness

The growing interest and awareness among consumers regarding the environmental impact of traditional internal combustion engine vehicles contribute to the market's growth. Automakers like Nissan and BMW have successfully marketed electric and hybrid models, capitalizing on the shifting consumer preferences towards sustainable and fuel-efficient alternatives. Increased public awareness, driven by initiatives promoting eco-friendly transportation and the benefits of alternative powertrains, has led to a surge in demand for electric and hybrid vehicles, shaping the market dynamics.

Challenges in Infrastructure Development

While the alternative powertrain market is driven by several factors, challenges associated with infrastructure development present a significant restraint. Companies such as ChargePoint and EVgo face obstacles in establishing a comprehensive charging infrastructure to support the growing number of electric vehicles. The lack of standardized charging stations, coupled with concerns about charging times and accessibility, hinders the widespread adoption of electric powertrains. Overcoming these challenges is crucial for ensuring the seamless integration of alternative powertrains into mainstream transportation.

Market Analysis by Powertrain: BEV Powertrains Dominates the Market

The market segmentation by powertrain includes battery electric vehicle (BEV) powertrain and hybrid powertrain. In 2025, BEV powertrains dominated the market, contributing significantly to revenue. The forecast for 2026 to 2034 indicates sustained dominance by BEV powertrains, with the highest expected CAGR. Hybrid powertrains, combining internal combustion engines with electric components, are expected to maintain a substantial market share during the forecast period, showcasing a balanced approach to alternative powertrains.

Market Analysis by Component: BMS and On-Board Chargers to Promise Top Opportunities during the Forecast Period

The market segmentation by component includes batteries, motor/generators, battery management systems (BMS), and on-board chargers. In 2025, batteries and motor/generators generated the highest revenue, driven by these components' critical role in alternative powertrains. However, during the forecast period from 2026 to 2034, BMS and on-board chargers are expected to exhibit the highest CAGR. The market dynamics indicate a shift towards increased demand for advanced systems that manage battery performance and efficient on-board charging.

North America remains the Global Leader

The alternative powertrain market exhibits diverse geographic trends. In 2025, North America led in terms of both highest revenue and CAGR, driven by a robust market for electric vehicles and supportive government policies. However, Asia-Pacific is expected to surpass North America in terms of CAGR during the forecast period, indicating the region's rapid adoption of alternative powertrains. Europe is anticipated to maintain a substantial market share, with government initiatives promoting sustainable transportation. The Middle East and Africa showcase a growing interest in alternative powertrains, contributing to the overall market expansion.

Market Competition to Intensify during the Forecast Period

The competitive landscape of the alternative powertrain market is characterized by key players such as Tesla, Toyota, Panasonic, LG Chem, Nissan, BMW, ChargePoint, EVgo, Volkswagen, Daimler, Ford Motor, Honda, General Motors, Hyundai, BYD, BAIC Group, GAC Group, Kia, Geely, Volvo, and TATA Motors. These companies have strategically positioned themselves by focusing on technological innovation, infrastructure development, and expanding their electric vehicle portfolios. In 2025, Tesla reported significant revenue, leveraging its leadership in electric vehicle technology and charging infrastructure. Toyota excelled in hybrid powertrain technology, while Panasonic and LG Chem demonstrated leadership in advancing battery technology. The key strategies of these players involve continuous research and development, strategic partnerships, and addressing challenges related to infrastructure development.

Historical & Forecast Period

This study report represents analysis of each segment from 2024 to 2034 considering 2025 as the base year. Compounded Annual Growth Rate (CAGR) for each of the respective segments estimated for the forecast period of 2026 to 2034.

The current report comprises of quantitative market estimations for each micro market for every geographical region and qualitative market analysis such as micro and macro environment analysis, market trends, competitive intelligence, segment analysis, porters five force model, top winning strategies, top investment markets, emerging trends and technological analysis, case studies, strategic conclusions and recommendations and other key market insights.

Research Methodology

The complete research study was conducted in three phases, namely: secondary research, primary research, and expert panel review. key data point that enables the estimation of Alternative Powertrain Market By Powertrain (Battery Electric Vehicle Powertrain, Hybrid Powertrain), By Component (Battery, Motor/Generator, Battery Management System (BMS), On-board Charger) - Growth, Share, Opportunities & Competitive Analysis, 2026 - 2034 market are as follows:

Market forecast was performed through proprietary software that analyzes various qualitative and quantitative factors. Growth rate and CAGR were estimated through intensive secondary and primary research. Data triangulation across various data points provides accuracy across various analyzed market segments in the report. Application of both top down and bottom-up approach for validation of market estimation assures logical, methodical and mathematical consistency of the quantitative data.

| ATTRIBUTE | DETAILS |

|---|---|

| Research Period | 2024-2034 |

| Base Year | 2025 |

| Forecast Period | 2026-2034 |

| Historical Year | 2024 |

| Unit | USD Million |

| Segmentation | |

Powertrain

|

|

Component

|

|

|

Region Segment (2024-2034; US$ Million)

|

Key questions answered in this report