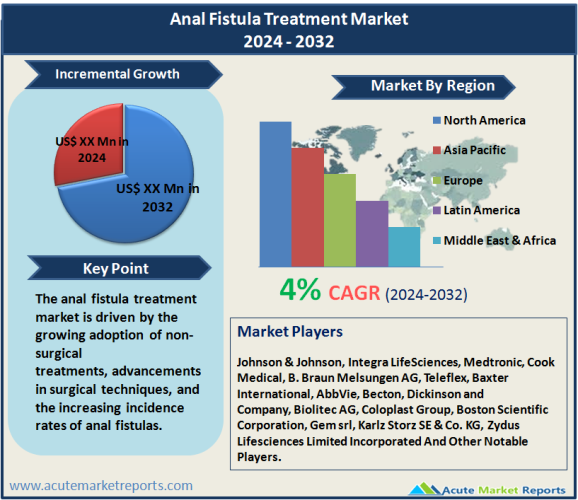

The anal fistula treatment market is expected to grow at a CAGR of 4% during the forecast period of 2026 to 2034, driven by the growing adoption of non-surgical treatments, advancements in surgical techniques, and the increasing incidence rates of anal fistulas. Challenges in the market adoption of seton techniques present a notable restraint. The market's segmentation by treatment type, application, and end-user reveals distinct leaders in revenue and CAGR, reflecting the varied dynamics within the industry. Geographically, North America and Asia-Pacific emerge as key growth drivers. The competitive landscape showcases key players employing varied strategies to secure their market positions. As the market progresses from 2026 to 2034, these trends are expected to shape the trajectory of the anal fistula treatment market, offering opportunities and challenges for industry stakeholders.

Key Market Drivers

Growing Adoption of Non-Surgical Treatments

The growing adoption of non-surgical treatments marked a pivotal driver in 2025. Healthcare providers, such as Johnson & Johnson and Integra LifeSciences, emphasized the use of drugs and innovative approaches like fibrin glue and adipose stem cell therapy for anal fistula treatment. The evidence supporting this driver includes an increased preference for non-surgical methods due to their minimally invasive nature, reduced recovery times, and comparable efficacy in certain cases. The emphasis on non-surgical options indicates a positive shift in the treatment paradigm.

Advancements in Surgical Techniques

Advancements in surgical techniques emerged as a significant driver for the anal fistula treatment market in 2025. Companies like Medtronic and Cook Medical played a crucial role in introducing and refining surgical procedures such as fistulotomy, bioprosthetic plugs, advancement flap procedures, and seton techniques. The evidence supporting this driver includes a surge in the adoption of advanced surgical techniques, offering improved success rates, reduced recurrence, and enhanced patient outcomes. The continuous evolution of surgical interventions underscores the commitment to refining treatment options for anal fistulas.

Increasing Incidence Rates Driving Market Demand

The increasing incidence rates of anal fistulas served as a driver propelling market demand in 2025. Companies and healthcare professionals, including B. Braun Melsungen AG and Baxter International, responded to the rising prevalence of anal fistulas by developing and offering comprehensive treatment solutions. The evidence supporting this driver includes epidemiological data indicating a growing number of patients seeking medical intervention for anal fistula management. The rising awareness among patients and healthcare providers regarding the importance of timely and effective treatment contributes to the overall market growth.

Restraint

Challenges in Market Adoption of Seton Techniques

Despite positive trends, challenges in the market adoption of seton techniques presented a notable restraint in 2025. Companies like Teleflex Incorporated faced hurdles in promoting the widespread use of seton techniques due to factors such as the complexity of the procedure, associated discomfort, and varied success rates. The evidence supporting this restraint includes medical literature discussing the limitations and patient reluctance associated with seton techniques, leading to a slower adoption rate compared to other surgical interventions.

Market Segmentation: Treatment Type

The anal fistula treatment market is segmented by treatment type into non-surgical (drugs and others, including fibrin glue, adipose stem cell therapy, etc.) and surgical (fistulotomy, bioprosthetic plugs, advancement flap procedures, seton techniques, and others). In 2025, the non-surgical segment led in both revenue and exhibited the highest Compound Annual Growth Rate (CAGR) during the forecast period of 2026 to 2034. The versatility and patient-friendly nature of non-surgical treatments contributed to their dominance in the market.

Market Segmentation: Application

Further segmentation by application categorizes the market into intersphincteric, transsphincteric, suprasphincteric, extrasphincteric, and others. In 2025, the intersphincteric application segment recorded the highest revenue, driven by the prevalence of anal fistulas in this specific location. Simultaneously, the transsphincteric application segment demonstrated the highest CAGR during the forecast period, indicating a growing demand for treatment solutions for fistulas located in this anatomical region.

Market Segmentation: End-user

The market segmentation by end-user categorizes it into hospitals & ambulatory surgical centers, clinics, and others. In 2025, hospitals & ambulatory surgical centers recorded the highest revenue, attributed to the availability of advanced treatment facilities and expertise in managing complex anal fistula cases. Conversely, the clinics segment demonstrated the highest CAGR during the forecast period, reflecting the growing trend of seeking outpatient-based treatments for anal fistulas.

North America Remains the Global Leader

Geographically, the anal fistula treatment market exhibited diverse trends in 2025. North America led in both revenue percentage and CAGR, driven by a high prevalence of anal fistulas, well-established healthcare infrastructure, and early adoption of advanced treatment options. Asia-Pacific, on the other hand, emerged as the region with the highest CAGR, fueled by increasing awareness, rising healthcare expenditures, and a growing patient pool. Europe secured the highest revenue percentage, supported by a comprehensive healthcare system and a proactive approach to managing anal fistulas.

Market Competition to Intensify during the Forecast Period

In 2025, the anal fistula treatment market featured a competitive landscape with top players employing various strategies to maintain and enhance their market positions. Leading companies such as Johnson & Johnson, Integra LifeSciences, Medtronic, Cook Medical, B. Braun Melsungen AG, Baxter International, Teleflex, AbbVie, Becton, Dickinson and Company, Biolitec AG, Boston Scientific Corporation, Coloplast Group, Gem srl, Karlz Storz SE & Co. KG, Zydus Lifesciences Limited Incorporated demonstrated robust financial performances, reporting substantial revenues. Strategies employed included advancements in treatment methods, research and development, and collaborations with healthcare institutions. Notably, these companies contributed to driving market growth by offering comprehensive solutions for anal fistula treatment.

Historical & Forecast Period

This study report represents analysis of each segment from 2024 to 2034 considering 2025 as the base year. Compounded Annual Growth Rate (CAGR) for each of the respective segments estimated for the forecast period of 2026 to 2034.

The current report comprises of quantitative market estimations for each micro market for every geographical region and qualitative market analysis such as micro and macro environment analysis, market trends, competitive intelligence, segment analysis, porters five force model, top winning strategies, top investment markets, emerging trends and technological analysis, case studies, strategic conclusions and recommendations and other key market insights.

Research Methodology

The complete research study was conducted in three phases, namely: secondary research, primary research, and expert panel review. key data point that enables the estimation of Anal Fistula Treatment Market By Treatment Type (Non-surgical, Surgical), By Application (Intersphincteric, Transsphincteric, Suprasphincteric, Extrasphincteric, Others), By End-User (Hospitals & Ambulatory Surgical Centers, Clinics, Others) - Growth, Share, Opportunities & Competitive Analysis, 2026 - 2034 market are as follows:

Market forecast was performed through proprietary software that analyzes various qualitative and quantitative factors. Growth rate and CAGR were estimated through intensive secondary and primary research. Data triangulation across various data points provides accuracy across various analyzed market segments in the report. Application of both top down and bottom-up approach for validation of market estimation assures logical, methodical and mathematical consistency of the quantitative data.

| ATTRIBUTE | DETAILS |

|---|---|

| Research Period | 2024-2034 |

| Base Year | 2025 |

| Forecast Period | 2026-2034 |

| Historical Year | 2024 |

| Unit | USD Million |

| Segmentation | |

Treatment Type

|

|

Application

|

|

End-User

|

|

|

Region Segment (2024-2034; US$ Million)

|

Key questions answered in this report