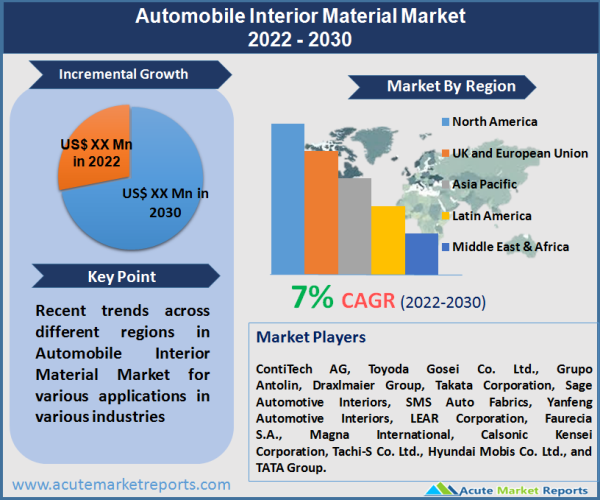

The global automobile interior material market is expected to grow at a CAGR of 7% during the forecast period 2026 and 2034. In comparison to other regions throughout the world, the markets for car interior materials are most developed in the Asia Pacific and the Middle East. This expansion can be ascribed to improving economic conditions and increasing urbanisation in nations located in the Middle East and Africa, as well as Asia and the Pacific. The market for automotive interior materials is being driven by a number of factors, including the strong demand for new technologies and customization, increased globalisation, and the optimization of fuel efficiency by reducing the overall weight of the vehicle. The expansion of the market, on the other hand, is being hindered by the inappropriate disposal of effluents that are produced during the tanning process of transforming raw animal hide into real leather. The wastewater that is produced as a result of the beam house processes, such as soaking, liming, and deliming, is extremely alkaline. This wastewater contains decomposing organic matter, hair, lime, sulphide, and organic nitrogen, and it has a high biochemical oxygen demand (BOD) as well as a high chemical oxygen demand (COD). The expansion of the market is being stunted as a direct result of this problem. This market is a challenge because of the difficulty of maintaining profitability while adhering to the regulatory structure.

The increasing preference for innovative designs in automotive interiors, the rising demand for electric, shared, and connected vehicles and the increasing use of bio-composites and lightweight polymers in the production of automotive interiors are some of the standard features that boost the market growth. Other features that boost the market growth include the introduction of new connected and shared vehicles. There are a number of important factors that, over the course of the forecast period, are anticipated to create growth opportunities in the market for automotive interior materials. These factors include the growing demand for high-quality and long-lasting interior materials in developed regions, as well as aesthetic and luxurious interiors.

Need for Comfort and Custom Solutions Driving the Market Growth

As a result of an increase in the number of travellers in recent years, the number of reasonably priced vehicles that are available in the market has expanded significantly. As a direct consequence of this, increasing expectations have been placed on the interior design of automobiles to meet the requirements of being both aesthetically pleasing and comfortable. The market is being driven by the rising demand for customised automotive interior materials as well as the increased technical developments in the industry. As a result, businesses are beginning to offer individualised customisation options in order to develop cutting-edge indoor spaces in response to the needs of their clientele. In addition, the growing health consciousness among customers is prompting businesses to develop environmentally friendly materials for the inside of automobiles, which will contribute to an increase in the level of comfort experienced by drivers. The market for vehicle interior materials is growing, and these variables are having an effect on that expansion.

Market Trend of Embracing Veganism and Bioplastics Fuelling the Market Growth

Plastics offer a number of benefits such as reduced weight, flexibility, and design, which is why the automotive industry has been using them for a long time for a variety of applications including interior, exterior, under the hood, and others. Because fossil fuel is a resource for plastics that is running out, the industry is currently adopting bio-based plastics to continue using autos for the purpose of ensuring weight reduction and robust performance. This is being done in order to continue using automobiles. As an illustration, the Lexus HS 250h has an interior that is fabricated from bioplastics. Numerous bio-based plastics, including bio-polyesters, bio-PET (polyethylene terephthalate), and PLA-blends (polylactic acid), have been incorporated by major automakers like Toyota into a variety of interior components of vehicles. These bioplastics are used in place of traditional petroleum-based alternatives. Headliners, sun visors, floor mats, and a number of other components in the Toyota Prius and Toyota SAI vehicles are all constructed of bio-plastics. Additionally, the term "veganism" has been implemented in the sector of the automobile business that deals with vehicles. As a result of the growing demand, automakers are beginning to provide customers with vegan inside leather options for their vehicles. At the Shanghai Motor Show in 2019, for instance, the German automaker Volkswagen debuted its full-size electric car called the "ID Roomzz," which boasts interiors made from apple leather. Other car manufacturers, including Volvo and Audi, have made similar announcements on new projects that will have vegan-friendly interiors.

Regulatory Environment and Need for Less Weighing Materials is Favouring the Market Expansion

The primary goal of the automobile industry is to lessen the amount of fuel consumed and pollutants produced by vehicles while simultaneously cutting down on their overall weight. As a result of this, customers are gravitating toward purchasing a variety of lightweight materials, which is expected to boost the overall market growth. As a result of the implementation of severe regulations such as CAFE (Corporate Average Fuel Economy), automotive manufacturers are striving to increase their use of lightweight materials in vehicles. These materials include plastics and textiles, among others. For example, the CAFE rules that will be in effect in North America in the year 2026 will require automakers to achieve a fleet average of at least 54.5 mpg. In addition, the adoption of materials such as plastics and composites gives automobile manufacturers more leeway to alter the design in order to achieve the highest possible level of performance. In addition, limits on the use of natural leather imposed by PETA (People for the Ethical Treatment of Animals) are driving up demand in the automotive sector for lightweight synthetic leather. This demand is being driven by rising levels of consumer awareness.

Increasing Demand for E-Vehicle Market is Accelerating the Market Growth

In response to growing worries about the environment and the impending depletion of fossil fuels, the market for electric vehicles is booming at a rapid rate across the globe. Plastics and other lightweight materials are used extensively in the construction of electric vehicles in order to achieve greater fuel efficiency and lower the amount of time required for recharging the batteries. When compared to more conventional forms of vehicle technology, electric vehicles are seen as a more economically and environmentally viable alternative by legislators all over the world. Customers of electric vehicles are being offered a wide variety of programmes and financial incentives in order to encourage greater uptake of environmentally friendly technology. The result of this has been an increase in the number of people purchasing electric vehicles, and many consumers are feeling inspired to join the "clean league" in the years to come. As an illustration, the number of electric vehicles sold all over the world increased by 73% in 2018.

Stringent Environment Regulations Limits the Use of Leather Products

The most expensive material that is now utilised for automobile upholstery is genuine leather, which may be rather pricey. However, because the tanning and tanning processes leave a negative impact on the environment, their use has remained mostly unchanged in developed countries. The strict environmental rules that have made it difficult for local manufacturers in these locations to remain viable have had a negative impact on the leather processing business in most of the developed markets. This has caused the leather processing industry to suffer in these markets. As a direct result of this, an increase in the quantity of leather that was imported from countries in Africa (heavy leather) and the Asia Pacific region (India, light leather) was seen. However, due to the high cost of imports, the availability of alternatives (such as synthetic leather), and the shifting attitude that customers have about genuine leather, the majority of producers have been forced to transition to environmentally friendly alternatives.

Uncertainty in the International Automotive Industry Will Have a Limiting Effect on the Market

In recent years, the progress of the automobile interior materials market has been hindered by factors such as the weak growth of the major automotive markets throughout the world. According to statistics compiled by the Organization Internationale des Constructeursd'Automobiles (OICA), several countries in 2018, including China, Spain, Turkey, Canada, and South Korea, all had negative growth rates in the automobile sector. Even huge countries like India saw their economies contract in 2019, which had a significant impact on the revenue of the regional industry. The outbreak of the coronavirus in China has further hampered the expansion of the automobile industry in that country as well as in a number of other regions. For example, Hyundai, a South Korean carmaker, halted vehicle manufacturing for a few days in February 2021 due to the disruption in the supply of automotive parts from China, which was further attributed to the spread of the coronavirus. It's possible that the scenario may continue to impede market growth in 2021. Changing regulatory standards on vehicle emissions, such as BSIV (India) "Bharat Stage 6," Euro6, etc., have also wreaked havoc on the automobile sector around the world. Consequently, as a result of the growing number of occurrences of this kind of disruption in the automobile industry, it is anticipated that the expansion of the market would be impeded over the period under consideration.

Environment-Friendly Products to Attract Significant Opportunities

The most polluting stage of the leather processing industry is the tanning process, which is part of the leather manufacturing process. The usage of metals such as chromium, aluminium chlorides, sulphates of potassium and aluminium, and zirconium sulphates are all components of this technique. Because of this, manufacturers have created, with the assistance of green chemistry, techniques for the use of safer chemicals that can be disposed of in an easier manner. The tanning of skins with glutaraldehyde in the presence of unnatural d-AA, such as d-alanine or d-lysine, is one of the more notable techniques among them. This technique results in high stability of the leather due to the bridging feature of the carboxylic as well as the amine group of the amino acids. Because the stated procedure does not include the use of toxic tanning agents, the wastewater that is created does not contain any dangerous chemicals; as a result, wastewater treatment plants benefit from the appropriate management and eventual disposal of waste.

The Polymer Will Be the Most Widely Material In 2022

Polymers that are used in the automotive interior are typically thermoplastics. Thermoplastics are multiphase compositions in which one phase consists of a material that is rigid at room temperature and fluid when heated, and the other phase consists of an elastomeric material that is soft and rubberlike when it is at room temperature. They are made of pliable materials that, when heated, become more malleable and may be shaped into any desired mould. After being allowed to cool, they took on a new shape that was smooth yet had a firm surface. In the automobile sector, thermoplastic polymers are utilised for a variety of components located both inside and outside of vehicles. These polymers assist original equipment manufacturers (OEMs) in the production of lightweight and long-lasting interior components. Polypropylene (PP), polyurethane (PU), polyvinyl chloride (PVC), and various other polymers are utilised in the interiors of automobiles. Because of their low weight, these polymers contribute to the increased fuel efficiency of cars.

Components made using injection moulding are commonly used in the vehicle interior trim because they enable a decrease in the amount of noise, vibration, and harshness (NVH) within the cabin. On the other hand, when it comes to value, the leather sector controls the majority of the market. When compared to synthetic leather, the cost of natural leather is significantly higher. The demand placed by consumers of luxury and premium vehicles for interiors and seating made of real leather is the primary factor driving the market for natural leather in automotive interiors. A significant amount of natural leather is also utilised in the construction of mid-sized premium vehicles. The market for a natural leather segment, on the other hand, may experience sluggish growth in the automobile industry as a result of the enhancement of the performance and appearance of synthetic leather as well as the introduction of vegan leather.

Automotive Interior Materials to Be Led by Passenger Vehicles

Passenger vehicles dominated the market in 2022 and this trend is expected to continue during the forecast period. It is anticipated that the trend of passenger cars capturing the biggest revenue share, which was more than 50% in the year 2021, will continue unabated during the forecast period. The expansion of the market is mostly attributable to the rising sales of passenger vehicles, in addition to the advent of driverless and electric vehicles. In addition to the aforementioned tendencies, the breakout of COVID-19 has also had a significant role in speeding the sale of privately owned passenger cars, which helps to maintain the social distance between individuals. This has slowed the development of shared mobility, but it has accelerated the trend of individuals purchasing their own vehicles, which has led to an increase in the number of people buying passenger automobiles. The usage of automotive interior materials in passenger vehicles is being driven due to rising standards of living in developing economies and the relocation of production facilities from a variety of manufacturers to these areas. On the other hand, the market for light commercial vehicles is expected to experience significant growth over the next few years due to an increase in e-commerce and retail logistics, particularly in emerging countries. The spread of the Coronavirus has contributed significantly to the rise of the practise of shopping online rather than physically going to stores. As a result, there was an increase in the size of the markets for e-commerce and retail logistics, which promotes the expansion of the market for light commercial vehicles.

Door Panel Application Dominates the Application Market

Door panel applications constituted the majority of the automobile interior materials market in the year 2022. Automobile door panels are components that help lessen the effect of side crashes and boost the occupant's overall safety. They achieve this by increasing the stiffness of the door. The door panel on the inside of the vehicle is constructed out of a variety of materials, and its finish is determined by the rest of the interior of the vehicle, which may include the dashboard and carpets, among other things. Depending on the vehicle type and market niche, door panels can be made of anything from basic plastic to leather that has been hand-stitched. The door panel is designed to improve the functionality and ergonomics of the car in addition to producing a more aesthetically pleasing appearance for the vehicle. This makes the interior of the vehicle a more pleasant place to be. The NVH, packing, storage, and aesthetics of the vehicle are all essential aspects that are affected by the door panels. Approximately 40% of an average vehicle's entire consumption of plastic is accounted for by the amount of plastic utilised in the vehicle's interior trim. In addition, the door panel and trims make up a significant portion of the automotive interior market, which allows manufacturers more room for customization and a significant reduction in weight in comparison to other components. The various materials that are used in these applications include, but are not limited to, acrylonitrile butadiene styrene (ABS), polypropylene (PP), polyethylene terephthalate (PET), polyoxymethylene (POM), polyvinyl chloride (PVC Because customers frequently tailor automotive carpeting and headliners to meet their specific needs, this market category is experiencing the highest rate of growth among all others.

APAC Remains as the Market Leader

Because of the region's robust economic expansion, the Asia-Pacific region has the world's largest market for automobile interior materials. The market for vehicle interior materials is propelled to a significant extent by these variables, which play an important role. The most important automobile manufacturers in the world are based in the developed countries of Asia and the Pacific. This area is important not only for its role as a manufacturing hub but also for the research and development facilities it contains. It is anticipated that the manufacturing and automotive industries will expand in emerging countries across Asia and the Pacific as a result of the general improvement in economic conditions and the surge in activity in the manufacturing sector. As a result of the movement of industrial bases to emerging nations, it is anticipated that the market in North America will expand at a rate that is only slightly above average during the period covered by the forecast. However, there will be a greater need for automobile interior materials in the region as a result of the growing popularity of luxury vehicles.

During the time period covered by the forecast, it is anticipated that Europe would represent the second-largest market for car interior materials. The increase in demand for automobile interior materials can be attributed to both the region's expanding industrial sector and its rapid technological advancement. The expansion of the market is also anticipated to be aided by the strengthening of the economy in the rest of the world. The automotive industry is recognised as one of Europe's most important sectors of business. The growing need for technology, the rising requirement for a safe and secure driving experience, and an increase in the development of connected automobiles are some of the primary growth drivers for the market for automotive interior materials in Europe. The biggest players in the automotive interior components and solution providers market include companies like Faurecia and Grupo Antolin, both of which are based in Spain. It is anticipated that there would be a rise in demand for vehicle interior materials as a result of ongoing innovations in the automotive sector and the expansion of distribution networks.

A robust automotive sector in countries such as China, India, South Korea, Japan, and Thailand has propelled Asia-Pacific to the forefront of the worldwide market for car interior materials. In addition, it is predicted that the region will increase rapidly throughout the course of the forecast period as a result of the rapidly increasing number of individuals belonging to the middle class in growing countries such as India, China, Taiwan, Thailand, and others. Additionally, the increasing sales and acceptance of electric vehicles in the region are projected to drive the growth of the market throughout the period of time that is still in the foreseeable future. Europe has established itself in the number two position in the industry and is anticipated to have moderate growth on the basis of the expanding market for electric vehicles. It is anticipated that the automobile industry in North America will continue its steady improvement, which will contribute to the region's moderate economic expansion. The increasing popularity of electric vehicles in the region is projected to serve as a driving force behind the expansion of the industry in the years to come. Because of the growing automotive sectors in Brazil and Mexico, Latin America has been positioned to experience robust growth in the near future. On the other hand, significant portions of the region, including Venezuela, Honduras, Ecuador, and others, are experiencing economic instability and political unrest at the present time, which is expected to impede the expansion of the market throughout the course of the projection period.

Market Remains Fragmented, Competition to Intensify During the Forecast Period

The market for vehicle interior materials is extremely fragmented, with regional and local firms controlling more than 70% of the overall market share. This indicates that there are a large number of participants in this market. The fact that the dominant businesses only control 27-32% of the revenue share is a clear indication that there are minimal barriers to entry into this competitive market area. Therefore, the market participants are pouring investments into the establishment of new production facilities across Asia Pacific and Latin America. The establishment of major strategic relationships has been and will continue to be the core of growth strategies for manufacturers. Key market players include ContiTech AG, Toyoda Gosei Co. Ltd., Grupo Antolin, Draxlmaier Group, Takata Corporation, Sage Automotive Interiors, SMS Auto Fabrics, Yanfeng Automotive Interiors, LEAR Corporation, Faurecia S.A., Magna International, Calsonic Kensei Corporation, Tachi-S Co. Ltd., Hyundai Mobis Co. Ltd., and TATA Group are some of the most important players in this market.

Key manufacturers are diversifying their product offerings in order to provide customers with a wide selection of materials for vehicle interiors. These materials must have qualities that are compatible with and customised to the ever-changing requirements of customers. For example, prominent carmaker Continental AG is getting ready to introduce high-end interior trimmings for automobiles by the year 2021. These trims will include dashboard covers, door trims, seat covers, and other similar components. Continental is prepared to place its bets on the launch of these premium interior trims in order to further solidify its position in the market. This decision was made after the company became aware of the fact that end-users continue to consider premium interiors to be an important selection criterion. In order to achieve their goal of producing novel materials for distinctive vehicle interiors, the market participants are working to gain complete awareness of the varied cultural trends, environmental goals and design preferences across the globe. Players such as DuPont have launched an entirely new series of automotive interior materials that are sourced from renewably available resources. It is anticipated that the market will restructure itself in the next years and move toward sustainability as a result of growing environmental concerns as well as a shift in customer demand away from non-renewable items and toward renewable ones.

Historical & Forecast Period

This study report represents analysis of each segment from 2024 to 2034 considering 2025 as the base year. Compounded Annual Growth Rate (CAGR) for each of the respective segments estimated for the forecast period of 2026 to 2034.

The current report comprises of quantitative market estimations for each micro market for every geographical region and qualitative market analysis such as micro and macro environment analysis, market trends, competitive intelligence, segment analysis, porters five force model, top winning strategies, top investment markets, emerging trends and technological analysis, case studies, strategic conclusions and recommendations and other key market insights.

Research Methodology

The complete research study was conducted in three phases, namely: secondary research, primary research, and expert panel review. key data point that enables the estimation of Automobile Interior Material Market By Type, By Vehicle, By Application, By End-users- Growth, Future Prospects And Competitive Analysis, 2026 - 2034 market are as follows:

Market forecast was performed through proprietary software that analyzes various qualitative and quantitative factors. Growth rate and CAGR were estimated through intensive secondary and primary research. Data triangulation across various data points provides accuracy across various analyzed market segments in the report. Application of both top down and bottom-up approach for validation of market estimation assures logical, methodical and mathematical consistency of the quantitative data.

| ATTRIBUTE | DETAILS |

|---|---|

| Research Period | 2024-2034 |

| Base Year | 2025 |

| Forecast Period | 2026-2034 |

| Historical Year | 2024 |

| Unit | USD Million |

| Segmentation | |

Type

|

|

Vehicle

|

|

Application

|

|

End-users

|

|

|

Region Segment (2024-2034; US$ Million)

|

Key questions answered in this report