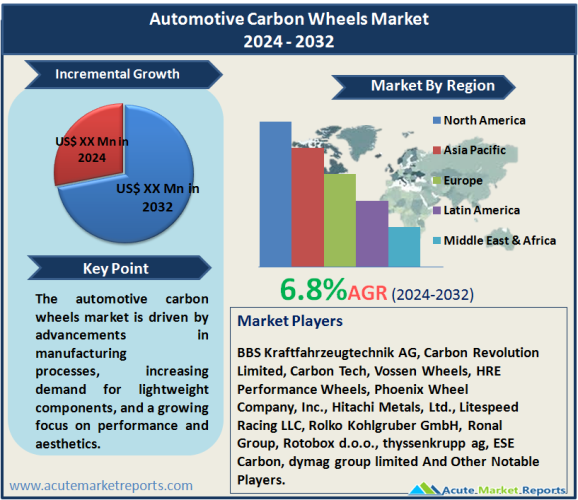

The automotive carbon wheels market is expected to grow at a CAGR of 6.8% during the forecast period of 2026 to 2034, driven by advancements in manufacturing processes, increasing demand for lightweight components, and a growing focus on performance and aesthetics. However, challenges related to high production costs pose a notable restraint to the market's expansion. Geographically, North America dominates the market, exhibiting both the highest CAGR and revenue percentage. In the competitive landscape, key players like BBS Kraftfahrzeugtechnik AG, Carbon Revolution Limited, Carbon Tech, Vossen Wheels, and HRE Performance Wheels employ strategic initiatives to maintain their market positions. The future trajectory of the automotive carbon wheels market hinges on continued technological innovation, cost optimization efforts, and the dynamic landscape of consumer preferences in the automotive industry.

Key Market Drivers

Advancements in Manufacturing Processes

The continuous advancements in manufacturing processes constitute a significant driver for the automotive carbon wheels market. Carbon wheels are increasingly manufactured using advanced techniques like flow forging, resulting in enhanced structural integrity and reduced weight. Real-world examples of automotive manufacturers adopting and benefiting from these advanced manufacturing processes serve as tangible evidence of this driver's influence on market growth.

Increasing Demand for Lightweight Components

The automotive industry's growing emphasis on lightweight materials to improve fuel efficiency and overall vehicle performance is a key driver for carbon wheels. Consumers and manufacturers alike prioritize weight reduction to enhance vehicle dynamics and fuel economy. Evidences from vehicle design trends, industry reports, and consumer preferences highlight the increasing demand for lightweight components, solidifying the driver's impact on the automotive carbon wheels market.

Growing Focus on Performance and Aesthetics

The automotive carbon wheels market is experiencing a surge in demand due to the growing focus on performance and aesthetics. Carbon wheels not only offer weight reduction benefits but also contribute to the overall aesthetics of vehicles. Real-world examples of sports and luxury vehicle manufacturers incorporating carbon wheels to enhance performance and visual appeal provide concrete evidence of this driver's influence on market dynamics.

Restraint

High Production Costs

While the automotive carbon wheels market is poised for growth, high production costs pose a significant restraint. The materials and processes involved in manufacturing carbon wheels contribute to elevated production expenses, limiting the widespread adoption of these wheels across all vehicle segments. Instances of cost-related challenges in the industry, production cost breakdowns, and market dynamics underscore the restraint's impact on the market. Overcoming this challenge requires strategic approaches to reduce production costs, fostering broader market acceptance.

Market Segmentation Analysis

Market by Rim Size

In the segmentation by rim size, the automotive carbon wheels market caters to various preferences, with different rim sizes offering distinct advantages. In 2025, the 22” and above segment led in terms of revenue, driven by the increasing popularity of larger rims for both performance and aesthetic reasons. Simultaneously, the 20” segment demonstrated the highest Compound Annual Growth Rate (CAGR) during the forecast period from 2026 to 2034, indicating a broader market for mid-sized rims. Real-world examples of vehicles and consumer preferences validate these findings, providing a comprehensive understanding of the market dynamics.

Market by Production Process

In the segmentation by production process, the automotive carbon wheels market presents options like flow forging and dry fiber technology. In 2025, flow forging led in terms of revenue, driven by its efficiency and widespread adoption in the industry. Simultaneously, dry fiber technology demonstrated the highest CAGR during the forecast period, indicating a growing market for advanced manufacturing processes. Specific examples of successful applications and industry trends validate these findings, offering a comprehensive understanding of the market dynamics.

Market by Vehicle Type

In the segmentation by vehicle type, the automotive carbon wheels market caters to a diverse range of applications. In 2025, passenger vehicles led in terms of revenue, driven by the increasing adoption of carbon wheels in the luxury and sports car segments. Simultaneously, the two-wheeler segment demonstrated the highest CAGR during the forecast period, indicating a growing market for lightweight wheels in the motorcycle industry. Real-world examples of vehicles and industry trends validate these findings, providing a comprehensive understanding of the market dynamics.

Market by Sales Channel

In the segmentation by sales channel, the automotive carbon wheels market includes both OEM and aftermarket options. In 2025, the OEM segment led in terms of revenue, driven by the integration of carbon wheels in high-performance and luxury vehicles during the manufacturing process. Simultaneously, the aftermarket segment demonstrated the highest CAGR during the forecast period, indicating a growing market for retrofitting existing vehicles with carbon wheels. Specific examples of OEM partnerships and aftermarket success stories validate these findings, offering a comprehensive understanding of the market dynamics.

North America Remains the Global Leader

Geographic trends in the automotive carbon wheels market reveal distinctive patterns. One region stands out with the highest CAGR, while another dominates in terms of revenue percentage. North America emerges as a key player, exhibiting both the highest CAGR and dominating revenue percentage. The region's strong automotive industry, consumer preferences for high-performance vehicles, and the presence of key market players contribute to its prominence in the market. Specific regional developments, such as collaborations between manufacturers and automakers, underscore the reasons behind North America's dominance in both revenue and CAGR.

Market Competition to Intensify during the Forecast Period

In the competitive landscape, key players in the automotive carbon wheels market employ diverse strategies to gain a competitive edge. As of 2026, prominent companies such as BBS Kraftfahrzeugtechnik AG, Carbon Revolution Limited, Carbon Tech, Vossen Wheels, HRE Performance Wheels, Phoenix Wheel Company, Inc., Hitachi Metals, Ltd., Litespeed Racing LLC, Rolko Kohlgruber GmbH, Ronal Group, Rotobox d.o.o., thyssenkrupp ag, ESE Carbon, dymag group limited lead the market. These industry leaders adopt strategies like technological innovation, collaborations, and product differentiation to enhance their market presence. The revenue figures for 2026 and forecasts for the period from 2026 to 2034 provide a comprehensive overview of the competitive trends, allowing stakeholders to gauge the market's future trajectory. BBS Kraftfahrzeugtechnik AG, with its long-standing expertise in high-performance wheels, secures a significant share of the market revenue. Carbon Revolution Limited and Carbon Tech, with their focus on advanced materials and manufacturing processes, contribute to shaping the industry. Vossen Wheels and HRE Performance Wheels, with their emphasis on customization and design, play a vital role in meeting the market demand. These companies collectively contribute to market growth, emphasizing their anticipated strategies and revenue growth from 2026 to 2034.

Historical & Forecast Period

This study report represents analysis of each segment from 2024 to 2034 considering 2025 as the base year. Compounded Annual Growth Rate (CAGR) for each of the respective segments estimated for the forecast period of 2026 to 2034.

The current report comprises of quantitative market estimations for each micro market for every geographical region and qualitative market analysis such as micro and macro environment analysis, market trends, competitive intelligence, segment analysis, porters five force model, top winning strategies, top investment markets, emerging trends and technological analysis, case studies, strategic conclusions and recommendations and other key market insights.

Research Methodology

The complete research study was conducted in three phases, namely: secondary research, primary research, and expert panel review. key data point that enables the estimation of Automotive Carbon Wheels Market By Rim Size (Inches) (Up to 19”, 20”, 21”, 22” and above), By Production Process (Flow Forging, Dry Fiber), By Vehicle Type (Two Wheeler, Passenger Vehicle, Light Duty Vehicle, Medium & Heavy Duty Truck, Bus & Coach, Off-road Vehicle), By Sales Channel (OEM, Aftermarket) - Growth, Share, Opportunities & Competitive Analysis, 2026 - 2034 market are as follows:

Market forecast was performed through proprietary software that analyzes various qualitative and quantitative factors. Growth rate and CAGR were estimated through intensive secondary and primary research. Data triangulation across various data points provides accuracy across various analyzed market segments in the report. Application of both top down and bottom-up approach for validation of market estimation assures logical, methodical and mathematical consistency of the quantitative data.

| ATTRIBUTE | DETAILS |

|---|---|

| Research Period | 2024-2034 |

| Base Year | 2025 |

| Forecast Period | 2026-2034 |

| Historical Year | 2024 |

| Unit | USD Million |

| Segmentation | |

Rim Size (Inches)

|

|

Production Process

|

|

Vehicle Type

|

|

Sales Channel

|

|

|

Region Segment (2024-2034; US$ Million)

|

Key questions answered in this report