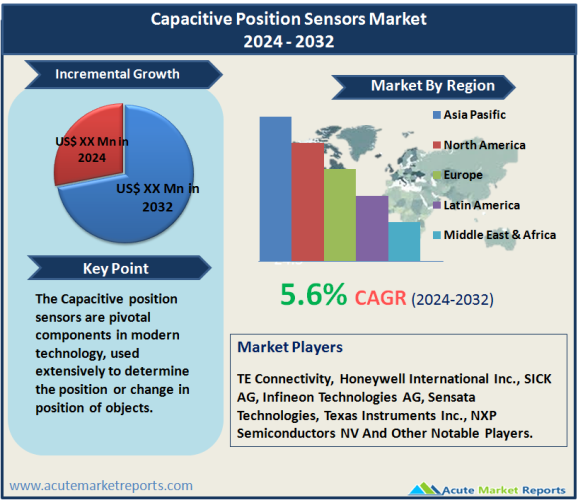

The capacitive position sensors market is expected to grow at a CAGR of 5.6% during the forecast period of 2026 to 2034. Capacitive position sensors are pivotal components in modern technology, used extensively to determine the position or change in position of objects. These sensors operate by detecting changes in capacitance within a given environment, influenced by the proximity or displacement of a conductive or non-conductive object. Their applications span across various industries including automotive, consumer electronics, aerospace, and industrial automation. The inherent accuracy, responsiveness, and cost-effectiveness of capacitive position sensors make them highly favored in applications requiring precise position control and measurement, contributing to the consistent expansion of their market.

Key Drivers of the Capacitive Position Sensors Market

Expansion of the Consumer Electronics Sector

The consumer electronics sector's rapid expansion significantly drives the demand for capacitive position sensors. These sensors are integral in numerous devices, from smartphones and tablets to wearables and smart home devices, where they facilitate user interface innovations such as touchscreens and gesture-based controls. The proliferation of interactive displays and the integration of advanced user interfaces in personal electronics compel continuous advancements in sensor technology, enhancing sensitivity and accuracy. The increasing consumer demand for sophisticated technology in daily devices sustains a robust market for capacitive sensors, ensuring their integration in new consumer electronics to improve functionality and user experience.

Advancements in Automotive Technology

Automotive technology advancements also contribute profoundly to the growth of the capacitive position sensors market. Modern vehicles, both conventional and electric, increasingly incorporate these sensors for various applications, including position sensing in electronic gear shifter systems, pedals, and automotive touchscreens. The shift towards autonomous and semi-autonomous vehicles has further elevated the importance of reliable and precise sensors to ensure safety and functionality. Capacitive position sensors are favored for their ability to operate effectively in the demanding automotive environment, dealing with factors such as vibration, dust, and moisture while providing critical data for vehicle control systems.

Industrial Automation and Robotics

The third driver is the surge in industrial automation and robotics. In industries, capacitive position sensors are crucial for precision control in robotic arms, assembly lines, and automated quality control systems. The transition towards Industry 4.0 underscores the integration of smart technologies and IoT, where capacitive position sensors play a vital role in enabling machines to perform complex tasks with high precision and minimal human intervention. Their robustness and long service life under harsh industrial conditions make them ideal for these applications, fueling their adoption across manufacturing sectors aiming to boost efficiency and productivity through automation.

Market Restraint

High Sensitivity to Environmental Factors

A major restraint in the capacitive position sensors market is their high sensitivity to environmental factors. These sensors can be significantly affected by changes in temperature, humidity, and the presence of dirt or other contaminants, which can alter capacitance readings and lead to inaccuracies in position sensing. This sensitivity limits their applicability in environments where such factors are uncontrollable, potentially leading to operational failures or the need for frequent recalibrations. Despite the advantages they offer, the requirement for stable environmental conditions to maintain accuracy and reliability can be a substantial hindrance, particularly in outdoor or harsh industrial settings where such conditions are difficult to manage. This limitation poses challenges to market growth, as potential users in certain sectors may seek alternative technologies that are less affected by environmental variations.

Market Segmentation by Type

The capacitive position sensors market is segmented by type into linear type, rotary sensor, and others. Linear type capacitive sensors hold the highest revenue share due to their widespread applications across various industries such as automotive, manufacturing, and consumer electronics. These sensors are prized for their ability to provide precise and continuous position measurement along a straight line, making them integral in processes that require exact linear positioning like CNC machining, robotics, and vehicle control systems. On the other hand, rotary sensors are projected to witness the highest CAGR. This growth is driven by the increasing use of these sensors in angular positioning and rotational measurements essential in automotive steering systems, industrial automation, and robotics. Rotary capacitive sensors are increasingly preferred for their accuracy and reliability in applications requiring detailed rotational feedback, such as in wind turbines and satellite positioning systems, where precise angular data is critical.

Market Segmentation by Contact Type

Regarding the contact type, the capacitive position sensors market is categorized into direct and indirect contact types. The direct contact type sensors dominate the market in terms of revenue due to their direct interaction with the target object, which often results in higher accuracy and faster response times. These sensors are extensively used in applications where physical contact with the measured object is feasible and can be done without compromising the integrity or operation of the system, such as in touch screen devices and user interface controls in consumer electronics and automotive systems. Conversely, indirect contact capacitive sensors are expected to experience the highest CAGR. This increase is attributed to their non-invasive measuring capability which is crucial in environments where direct contact with the target can lead to contamination or damage, such as in chemical processing or semiconductor manufacturing. Indirect sensors are also increasingly utilized in healthcare and biomedical applications, where non-contact measurement of displacement and positioning is essential, driving their demand in advanced medical devices and equipment.

Geographic Trends

The capacitive position sensors market is defined by strong geographic trends with Asia-Pacific (APAC) leading in terms of both current revenue and projected growth rates. This dominance is due to the extensive manufacturing base in the region, particularly in countries like China, South Korea, and Taiwan, where there's a high concentration of consumer electronics, automotive, and industrial automation companies. The expansion of these sectors, coupled with supportive government policies aimed at enhancing technological advancements, drives substantial demand for capacitive position sensors in the region. Moreover, APAC's emphasis on adopting advanced technologies in manufacturing and the automotive industry fuels the region's higher compound annual growth rate (CAGR) expectations from 2026 to 2034.

Competitive Trends

In terms of competitive trends, the market features a robust presence of leading players such as TE Connectivity, Honeywell International Inc., SICK AG, Infineon Technologies AG, Sensata Technologies, Texas Instruments Inc., and NXP Semiconductors NV. These companies are pivotal in shaping the market dynamics through continuous innovation and strategic expansions. In 2025, they reported substantial revenues driven by increased demand across various applications of capacitive position sensors. From 2026 to 2034, these companies are expected to further solidify their market positions by focusing on technological advancements, expanding into new geographic markets, and forming strategic alliances. For instance, TE Connectivity and Infineon Technologies are likely to enhance their R&D investments to develop more sophisticated, miniaturized sensors with enhanced capabilities suitable for emerging applications in connected devices and IoT. Honeywell and Sensata Technologies are anticipated to expand their product offerings to include sensors that can operate in harsher environments, targeting sectors such as aerospace and defense where robustness and reliability are critical. Moreover, strategic mergers and acquisitions are expected to be prevalent as companies aim to broaden their technological capabilities and market reach. NXP Semiconductors and Texas Instruments are projected to leverage their expertise in semiconductor technologies to innovate in sensor ICs, which are integral to enhancing sensor performance and integration with other system components. These strategies are crucial for companies aiming to stay competitive in a market that is becoming increasingly sophisticated with demands for higher accuracy, durability, and cost-effectiveness in sensor solutions.

Historical & Forecast Period

This study report represents analysis of each segment from 2024 to 2034 considering 2025 as the base year. Compounded Annual Growth Rate (CAGR) for each of the respective segments estimated for the forecast period of 2026 to 2034.

The current report comprises of quantitative market estimations for each micro market for every geographical region and qualitative market analysis such as micro and macro environment analysis, market trends, competitive intelligence, segment analysis, porters five force model, top winning strategies, top investment markets, emerging trends and technological analysis, case studies, strategic conclusions and recommendations and other key market insights.

Research Methodology

The complete research study was conducted in three phases, namely: secondary research, primary research, and expert panel review. key data point that enables the estimation of Capacitive Position Sensors Market By Type (Linear Type, Rotary Sensor, Others), By Contact Type (Direct Contact Type, Indirect Contact Type) - Growth, Share, Opportunities & Competitive Analysis, 2026 - 2034 market are as follows:

Market forecast was performed through proprietary software that analyzes various qualitative and quantitative factors. Growth rate and CAGR were estimated through intensive secondary and primary research. Data triangulation across various data points provides accuracy across various analyzed market segments in the report. Application of both top down and bottom-up approach for validation of market estimation assures logical, methodical and mathematical consistency of the quantitative data.

| ATTRIBUTE | DETAILS |

|---|---|

| Research Period | 2024-2034 |

| Base Year | 2025 |

| Forecast Period | 2026-2034 |

| Historical Year | 2024 |

| Unit | USD Million |

| Segmentation | |

Type

|

|

Contact Type

|

|

|

Region Segment (2024-2034; US$ Million)

|

Key questions answered in this report