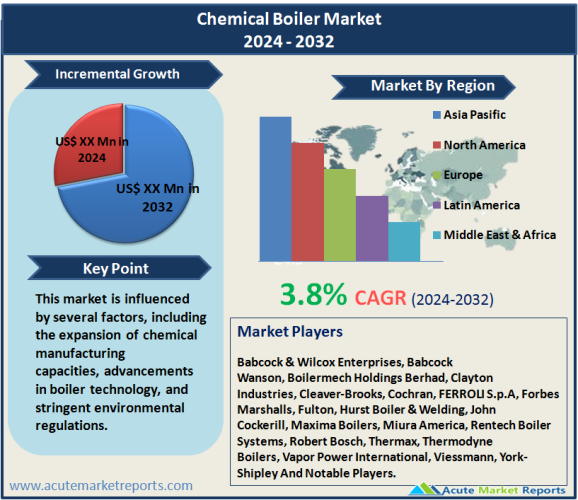

The chemical boiler market is expected to grow at a CAGR of 3.8% during the forecast period of 2026 to 2034. Chemical boiler market is a specialized segment within the industrial boiler industry, catering primarily to the chemical manufacturing sector. Chemical boilers are essential for producing steam that is used in various chemical processes such as separation, reaction, and concentration. This market is influenced by several factors, including the expansion of chemical manufacturing capacities, advancements in boiler technology, and stringent environmental regulations.

Driver 1 : Expansion of Chemical Manufacturing

Global Growth in Chemical Production

The chemical industry is experiencing robust growth worldwide, driven by increasing demand for chemicals in various sectors such as automotive, pharmaceuticals, and agriculture. This growth necessitates the expansion of production facilities, including the installation of new chemical boilers. For example, regions like Asia Pacific are seeing significant investments in chemical production facilities, boosting the demand for high-efficiency boilers.

Emergence of Specialty Chemicals

The rise in the production of specialty chemicals, which require precise thermal management, is also propelling the chemical boiler market. Specialty chemicals, such as high-purity acids and performance chemicals, need specialized steam generation systems that can maintain exact temperature and pressure levels, leading to higher demand for advanced boiler systems.

Infrastructure Development in Emerging Economies

Emerging economies such as India and Brazil are witnessing substantial infrastructure development, leading to increased investments in chemical plants. These developments are directly linked to a heightened need for chemical boilers that can support large-scale chemical production efficiently.

Driver 2 : Technological Advancements in Boiler Systems

Integration of IoT and Automation

Technological advancements, particularly the integration of IoT and automation in boiler systems, have significantly improved the efficiency and operational control of chemical boilers. These technologies enable real-time monitoring and adjustment of boiler operations, optimizing energy use and reducing downtime.

Advancements in Thermal Efficiency

New materials and designs in boiler construction have improved thermal efficiency, reducing fuel consumption and operational costs for chemical producers. For instance, modern boilers are equipped with better insulation and heat recovery systems that minimize heat loss during operations.

Regulatory Compliance

As regulations regarding emissions and energy efficiency tighten, chemical producers are compelled to adopt newer, more efficient boiler technologies. These regulations drive the development and adoption of advanced boilers that meet or exceed environmental standards.

Driver 3 : Environmental Regulations

Emission Control Requirements

Strict environmental regulations across the globe mandate the reduction of harmful emissions such as NOx and SOx from boiler operations. Chemical producers are increasingly adopting green boiler technologies that incorporate emission control systems to comply with these regulations.

Energy Efficiency Standards

Energy efficiency regulations require chemical plants to use boilers that minimize energy waste. This has led to a surge in demand for boilers with better heat utilization capabilities, influencing boiler design and material use to enhance energy conservation.

Sustainability Initiatives

With the chemical industry under scrutiny for its environmental impact, there is a growing trend towards sustainability. This trend encourages the adoption of boilers that support sustainable operations, such as those utilizing renewable energy sources or those that are highly energy-efficient.

Restraint: High Initial Investment Costs

Capital Intensive Nature

The adoption of high-efficiency boiler systems in the chemical industry is often hindered by the high initial costs associated with these technologies. Advanced boilers that feature enhanced control systems, superior materials, and emissions reduction technologies typically require a significant upfront investment. While these boilers offer long-term savings through reduced operational costs and compliance with stringent environmental regulations, the initial financial barrier can be a significant restraint for smaller chemical producers or those in developing regions. This factor slows down the market growth as potential buyers delay upgrades or new installations.

Market Segmentation by Capacity

The chemical boiler market is segmented by capacity, which includes a broad range of units from less than 10 MMBTU/hr to over 250 MMBTU/hr. The segment of 100-175 MMBTU/hr boilers is experiencing the highest Compound Annual Growth Rate (CAGR), driven by their versatility and suitability for a wide range of medium to large-scale chemical production processes that require substantial but not excessive steam output. This capacity range strikes a balance between efficiency and power, making it ideal for emerging market entrants and expanding facilities in developing regions. On the revenue front, the largest share is held by the 50-75 MMBTU/hr segment. These boilers are commonly used in established chemical plants with considerable production capacities, providing the necessary steam output to meet extensive process demands while also supporting compliance with environmental regulations. The robust demand for this segment is primarily due to the extensive installation base and replacement market in mature industrial regions such as North America and Europe, where stringent efficiency standards and environmental regulations drive the replacement of older, less efficient units with modern, high-performance models.

Market Segmentation by Product

In terms of product segmentation, the chemical boiler market differentiates between fire-tube and water-tube boilers. Water-tube boilers are leading with the highest Compound Annual Growth Rate (CAGR) due to their ability to operate at higher pressures and temperatures than fire-tube boilers. This capability makes them particularly suitable for high-capacity applications typical in large chemical manufacturing plants. They are favored for their efficiency and safety features, which are essential in high-stakes chemical production environments. In contrast, fire-tube boilers dominate in terms of revenue generation. These boilers are preferred in small to medium-scale operations where initial cost, simplicity, and ease of operation are prioritized. Fire-tube boilers have a substantial market presence due to their long-term reliability and lower maintenance requirements, making them suitable for a wide range of applications in less intensive chemical processes where the cost considerations outweigh the benefits of higher pressure and temperature capabilities offered by water-tube boilers. Both segments reflect the evolving needs of the chemical industry, with technological advancements and regulatory pressures shaping the market dynamics.

Geographic Segment

The chemical boiler market exhibits varied geographic trends, reflecting the economic, industrial, and regulatory landscapes of different regions. Asia Pacific stands out with the highest Compound Annual Growth Rate (CAGR), primarily due to rapid industrialization, growth in chemical manufacturing, and substantial investments in infrastructure development across countries like China, India, and Southeast Asia. This region's dominance is further buoyed by its increasing environmental regulations, pushing for more efficient and cleaner energy sources in industrial applications. In terms of revenue, North America holds the largest share, attributed to its mature chemical industry, stringent environmental regulations, and technological advancements in boiler technology.

Competitive Trends

The competitive landscape in this market is robust, featuring key players such as Babcock & Wilcox Enterprises, Babcock Wanson, Boilermech Holdings Berhad, Clayton Industries, Cleaver-Brooks, Cochran, FERROLI S.p.A, Forbes Marshalls, Fulton, Hurst Boiler & Welding, John Cockerill, Maxima Boilers, Miura America, Rentech Boiler Systems, Robert Bosch, Thermax, Thermodyne Boilers, Vapor Power International, Viessmann, and York-Shipley. These companies employ various strategies to sustain and enhance their market positions, including product innovation, mergers and acquisitions, and geographic expansion to tap into emerging markets. In 2025, these companies reported significant revenues, reflecting their dominance and competitive edge in the market. From 2026 to 2034, these players are expected to focus on integrating more advanced technologies such as IoT and automation to improve boiler efficiency and performance, adhere to stricter emissions regulations, and meet the rising demand for energy-efficient systems. Their strategies are expected to emphasize sustainability and adaptability, aligning with global shifts towards renewable energy and reduced carbon footprints in industrial operations. This forward-looking approach is poised to drive continuous growth and technological evolution in the chemical boiler market, ensuring these companies remain at the forefront of the industry.

Historical & Forecast Period

This study report represents analysis of each segment from 2024 to 2034 considering 2025 as the base year. Compounded Annual Growth Rate (CAGR) for each of the respective segments estimated for the forecast period of 2026 to 2034.

The current report comprises of quantitative market estimations for each micro market for every geographical region and qualitative market analysis such as micro and macro environment analysis, market trends, competitive intelligence, segment analysis, porters five force model, top winning strategies, top investment markets, emerging trends and technological analysis, case studies, strategic conclusions and recommendations and other key market insights.

Research Methodology

The complete research study was conducted in three phases, namely: secondary research, primary research, and expert panel review. key data point that enables the estimation of Chemical Boiler Market By Capacity (< 10 MMBTU/hr, 10-25 MMBTU/hr, 25-50 MMBTU/hr, 50-75 MMBtu/hr, 75-100 MMBTU/hr, 100-175 MMBTU/hr, 175-250 MMBTU/hr, > 250 MMBTU/hr), By Product (Fire-tube, Water-tube), By Technology (Condensing, Non-condensing), By Fuel (Natural gas, Oil, Coal, Others) - Growth, Share, Opportunities & Competitive Analysis, 2026 - 2034 market are as follows:

Market forecast was performed through proprietary software that analyzes various qualitative and quantitative factors. Growth rate and CAGR were estimated through intensive secondary and primary research. Data triangulation across various data points provides accuracy across various analyzed market segments in the report. Application of both top down and bottom-up approach for validation of market estimation assures logical, methodical and mathematical consistency of the quantitative data.

| ATTRIBUTE | DETAILS |

|---|---|

| Research Period | 2024-2034 |

| Base Year | 2025 |

| Forecast Period | 2026-2034 |

| Historical Year | 2024 |

| Unit | USD Million |

| Segmentation | |

Capacity

|

|

Product

|

|

Technology

|

|

Fuel

|

|

|

Region Segment (2024-2034; US$ Million)

|

Key questions answered in this report