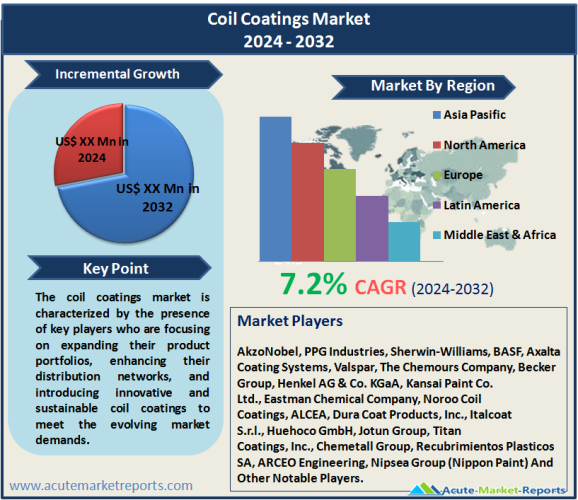

The coil coatings market is expected to grow at a CAGR of 7.2% from 2026 to 2034, driven by the demand from various % end-use industries such as building and construction, automotive, and appliances. This growth is primarily attributed to the increased need for durable and aesthetically appealing coatings for metal surfaces. In 2025, the market experienced significant revenue generation, and it is projected to continue expanding at a notable compound annual growth rate (CAGR) from 2026 to 2034. However, the market faces challenges due to the volatility in raw material prices. Regarding market segmentation, the polyester segment generated the highest revenue in 2025, while the fluoropolymer segment is expected to register the highest CAGR during the forecast period. The steel segment accounted for the highest revenue in 2025, while the aluminum segment is expected to witness the highest CAGR. The building and construction segment generated the highest revenue in 2025, while the automotive segment is expected to register the highest CAGR. Geographically, the Asia-Pacific region dominated the market in 2025, while the North American region is expected to register the highest CAGR during the forecast period. The competitive landscape of the coil coatings market is characterized by the presence of key players who are focusing on expanding their product portfolios, enhancing their distribution networks, and introducing innovative and sustainable coil coatings to meet the evolving market demands. The coil coatings market is poised for significant growth, driven by the increasing demand for high-performance and eco-friendly coatings in various end-use industries.

Drivers

Rising Demand in the Building & Construction Industry

The building and construction industry has been a major driver for the coil coatings market. With the global population rising and urbanization accelerating, there is an increasing need for residential, commercial, and industrial infrastructure. Coil coatings offer several advantages, such as corrosion resistance, UV protection, and enhanced aesthetic appeal, which make them ideal for use in roofing, cladding, and other building materials. For instance, the Asia-Pacific region, particularly China and India, has seen massive investments in infrastructure projects. According to a report by Global Construction Perspectives and Oxford Economics, the global construction market is expected to grow by $8 trillion by 2034, with China, India, and the United States leading the way. This surge in construction activities boosts the demand for coil coatings, as these regions focus on modernizing their infrastructure and enhancing the durability of buildings. Additionally, green building initiatives and stringent environmental regulations have encouraged the use of eco-friendly and energy-efficient materials, further propelling the coil coatings market. The adoption of sustainable construction practices is expected to drive the demand for coil coatings that offer low VOC emissions and improved energy efficiency.

Advancements in Coating Technologies

Technological advancements in coil coatings have significantly contributed to market growth. Innovations in coating formulations, such as the development of advanced polyester, fluoropolymer, and siliconized polyester coatings, have enhanced the performance characteristics of these products. For example, fluoropolymer coatings are known for their exceptional weatherability, chemical resistance, and color retention, making them suitable for harsh environments. In 2025, the demand for high-performance coatings surged, driven by the need for durable and long-lasting solutions in various industries. Companies like AkzoNobel, PPG Industries, and Sherwin-Williams have been at the forefront of developing cutting-edge coil coatings that meet stringent industry standards. Moreover, the integration of nanotechnology in coil coatings has opened new avenues for product development. Nanocoatings offer superior properties such as scratch resistance, self-cleaning capabilities, and enhanced barrier protection. These advancements have led to the adoption of coil coatings in applications where traditional coatings may fall short, thereby driving market growth. The increasing emphasis on research and development activities by key players to introduce innovative products is expected to fuel the demand for advanced coil coatings during the forecast period.

Growing Automotive Industry

The automotive industry has been a significant driver for the coil coatings market. Coil coatings are extensively used in the automotive sector for coating various components, including body panels, roofs, and interior parts. The demand for coil coatings in this industry is primarily driven by the need for corrosion resistance, aesthetic appeal, and durability. In 2025, the global automotive industry witnessed a rebound in production and sales after the COVID-19 pandemic. This recovery was fueled by increased consumer demand, government incentives, and investments in electric vehicles (EVs). The shift towards lightweight materials and the growing adoption of electric vehicles have further amplified the demand for high-performance coil coatings. For instance, EV manufacturers require coatings that offer superior heat resistance and electrical insulation properties to enhance the performance and safety of battery packs. Additionally, the automotive industry's focus on sustainability and reducing carbon emissions has led to the adoption of eco-friendly coil coatings. Companies like BASF and Axalta Coating Systems have introduced environmentally friendly coil coatings that meet the industry's stringent requirements. The increasing production of electric vehicles and the automotive industry's push towards sustainable practices are expected to drive the demand for coil coatings in the coming years.

Restraint

Volatility in Raw Material Prices

One of the primary restraints for the coil coatings market is the volatility in raw material prices. Coil coatings are formulated using various raw materials, including resins, pigments, solvents, and additives. The prices of these raw materials are influenced by several factors, such as fluctuations in crude oil prices, supply-demand imbalances, and geopolitical tensions. In 2025, the coil coatings market faced challenges due to the fluctuating prices of raw materials, particularly resins and pigments. For instance, the price of crude oil, a key raw material for resin production, experienced significant volatility due to geopolitical tensions in the Middle East and the Russia-Ukraine conflict. This volatility directly impacted the production costs of coil coatings, leading to increased prices for end-users. Additionally, supply chain disruptions caused by the COVID-19 pandemic and trade restrictions affected the availability of raw materials, further exacerbating the price volatility. The uncertainty in raw material prices poses a challenge for manufacturers, as it affects their profit margins and pricing strategies. To mitigate this restraint, companies are exploring alternative raw materials and developing strategies to optimize their supply chains. However, managing the impact of raw material price volatility remains a critical challenge for the coil coatings market.

Market Segmentation by Resin Type

In 2025, the polyester segment dominated the coil coatings market, generating the highest revenue. Polyester coil coatings are widely used due to their excellent weatherability, flexibility, and cost-effectiveness. They are preferred for applications in the building and construction industry, where long-term durability and aesthetic appeal are crucial. The increasing construction activities, particularly in emerging economies, have driven the demand for polyester coil coatings. Additionally, the automotive and appliance industries have also contributed to the high revenue generation of polyester coatings due to their use in various components and panels. On the other hand, the fluoropolymer segment is expected to register the highest CAGR during the forecast period from 2026 to 2034. Fluoropolymer coatings offer superior resistance to UV radiation, chemicals, and extreme weather conditions. They are increasingly adopted in applications requiring high-performance coatings, such as architectural panels, automotive components, and industrial equipment. The growing emphasis on sustainability and the need for longer-lasting coatings have driven the demand for fluoropolymer coil coatings. Companies like Valspar, Beckers Group, and Kansai Paint have been actively involved in developing advanced fluoropolymer coatings to cater to the evolving needs of various industries. The technological advancements in fluoropolymer coatings and their increasing adoption in diverse applications are expected to drive their market growth at the highest CAGR during the forecast period.

Market Segmentation by Application

In 2025, the steel segment accounted for the highest revenue in the coil coatings market. Steel is extensively used in the building and construction industry for applications such as roofing, cladding, and structural components. The durability, strength, and versatility of steel make it a preferred choice for construction projects, driving the demand for coil coatings. Additionally, the automotive industry also contributes significantly to the high revenue generation of steel coil coatings, as steel is commonly used in vehicle bodies and components. The increasing investments in infrastructure development and the growing automotive production have fueled the demand for steel coil coatings. However, the aluminum segment is expected to witness the highest CAGR during the forecast period from 2026 to 2034. Aluminum is gaining popularity in various industries due to its lightweight, corrosion-resistant, and recyclable properties. The automotive industry, in particular, is shifting towards aluminum for manufacturing lightweight vehicles to improve fuel efficiency and reduce emissions. The rising adoption of electric vehicles, which require lightweight materials, is further driving the demand for aluminum coil coatings. Companies like Henkel, Nippon Paint Holdings, and Wacker Chemie are focusing on developing advanced aluminum coil coatings to cater to the growing demand from the automotive and construction sectors. The increasing use of aluminum in diverse applications and its advantages over traditional materials are expected to drive the highest CAGR for aluminum coil coatings during the forecast period.

Market Segmentation by End User

In 2025, the building and construction segment generated the highest revenue in the coil coatings market. The rapid urbanization, population growth, and increasing infrastructure investments have led to a surge in construction activities worldwide. Coil coatings are extensively used in the construction industry for applications such as roofing, cladding, and facades. The need for durable, weather-resistant, and aesthetically appealing coatings has driven the demand for coil coatings in this segment. Additionally, government initiatives to promote green buildings and energy-efficient infrastructure have further boosted the adoption of coil coatings. However, the automotive segment is expected to register the highest CAGR during the forecast period from 2026 to 2034. The automotive industry's focus on lightweight materials, electric vehicles, and sustainability has increased the demand for high-performance coil coatings. Coil coatings offer advantages such as corrosion resistance, UV protection, and enhanced aesthetics, making them ideal for automotive applications. The increasing production of electric vehicles and the shift towards sustainable practices in the automotive industry are expected to drive the highest CAGR for coil coatings in this segment. Companies like AkzoNobel, PPG Industries, and Sherwin-Williams are investing in research and development to introduce innovative coil coatings that meet the evolving requirements of the automotive sector. The growing emphasis on reducing carbon emissions and improving vehicle performance is expected to fuel the demand for coil coatings in the automotive industry during the forecast period.

Geographic Trends

In 2025, the Asia-Pacific region dominated the coil coatings market, generating the highest revenue. The region's rapid industrialization, urbanization, and infrastructure development have driven the demand for coil coatings in various end-use industries. China, India, and Japan are the major contributors to the market growth in this region. China, in particular, has witnessed significant investments in construction projects, automotive production, and manufacturing activities. The country's focus on modernizing its infrastructure and increasing urbanization has boosted the demand for coil coatings. Additionally, the presence of key market players and the availability of raw materials at competitive prices have further supported the market growth in the Asia-Pacific region. However, the North American region is expected to register the highest CAGR during the forecast period from 2026 to 2034. The region's growing automotive industry, coupled with the increasing demand for sustainable and energy-efficient coatings, is driving the market growth. The United States and Canada are the major contributors to the market growth in North America. The automotive industry's shift towards electric vehicles and the emphasis on lightweight materials have increased the demand for coil coatings in this region. Furthermore, stringent environmental regulations and the focus on reducing carbon emissions are encouraging the adoption of eco-friendly coil coatings. Companies like BASF, Axalta Coating Systems, and Beckers Group are actively expanding their presence in the North American market to capitalize on the growing opportunities. The increasing investments in research and development and the presence of advanced manufacturing facilities are expected to drive the highest CAGR for coil coatings in North America during the forecast period.

Competitive Trends

The coil coatings market is highly competitive, with several key players actively involved in expanding their market presence and introducing innovative products. In 2025, major players like AkzoNobel, PPG Industries, Sherwin-Williams, BASF, Axalta Coating Systems, Valspar, The Chemours Company, Becker Group, Henkel AG & Co. KGaA, Kansai Paint Co. Ltd., Eastman Chemical Company, Noroo Coil Coatings, ALCEA, Dura Coat Products, Inc., Italcoat S.r.l., Huehoco GmbH, Jotun Group, Titan Coatings, Inc., Chemetall Group, Recubrimientos Plasticos SA, ARCEO Engineering, and Nipsea Group (Nippon Paint) held significant market shares. These companies have adopted various strategies to strengthen their market positions and cater to the growing demand for coil coatings. For instance, AkzoNobel has focused on expanding its product portfolio through acquisitions and partnerships. In 2025, the company acquired Titan Paints in Spain, enhancing its presence in the European market. PPG Industries, on the other hand, has emphasized research and development to introduce advanced coil coatings with enhanced performance characteristics. The company invested heavily in its technology centers to develop innovative solutions for the automotive and construction industries. Sherwin-Williams has leveraged its extensive distribution network and strong customer relationships to expand its market reach. The company has also focused on sustainability initiatives, introducing eco-friendly coil coatings to meet the evolving industry requirements. BASF has been actively involved in strategic collaborations and joint ventures to enhance its product offerings. In 2025, the company entered into a partnership with Nippon Paint Holdings to develop advanced coil coatings for the automotive industry. Axalta Coating Systems has emphasized expanding its global footprint through acquisitions and partnerships. The company acquired Capital Paints LLC in 2025, strengthening its presence in the Middle East and North Africa region. Valspar has focused on innovation and product development to cater to the diverse needs of its customers. The company introduced a range of high-performance coil coatings for the building and construction industry, enhancing its market position. The competitive landscape of the coil coatings market is characterized by continuous investments in research and development, strategic collaborations, and acquisitions to gain a competitive edge. The key players are expected to focus on expanding their product portfolios, enhancing their distribution networks, and introducing sustainable and high-performance coil coatings to meet the evolving market demands during the forecast period.

Historical & Forecast Period

This study report represents analysis of each segment from 2024 to 2034 considering 2025 as the base year. Compounded Annual Growth Rate (CAGR) for each of the respective segments estimated for the forecast period of 2026 to 2034.

The current report comprises of quantitative market estimations for each micro market for every geographical region and qualitative market analysis such as micro and macro environment analysis, market trends, competitive intelligence, segment analysis, porters five force model, top winning strategies, top investment markets, emerging trends and technological analysis, case studies, strategic conclusions and recommendations and other key market insights.

Research Methodology

The complete research study was conducted in three phases, namely: secondary research, primary research, and expert panel review. key data point that enables the estimation of Coil Coatings Market By Resin Type (Polyester, Fluoropolymer, Siliconized polyester, Plastisol, Others), By Application (Steel, Aluminum), By End User (Building & construction, Automotive, Appliance, Others) - Growth, Share, Opportunities & Competitive Analysis, 2026 - 2034 market are as follows:

Market forecast was performed through proprietary software that analyzes various qualitative and quantitative factors. Growth rate and CAGR were estimated through intensive secondary and primary research. Data triangulation across various data points provides accuracy across various analyzed market segments in the report. Application of both top down and bottom-up approach for validation of market estimation assures logical, methodical and mathematical consistency of the quantitative data.

| ATTRIBUTE | DETAILS |

|---|---|

| Research Period | 2024-2034 |

| Base Year | 2025 |

| Forecast Period | 2026-2034 |

| Historical Year | 2024 |

| Unit | USD Million |

| Segmentation | |

Resin Type

|

|

Application

|

|

End User

|

|

|

Region Segment (2024-2034; US$ Million)

|

Key questions answered in this report