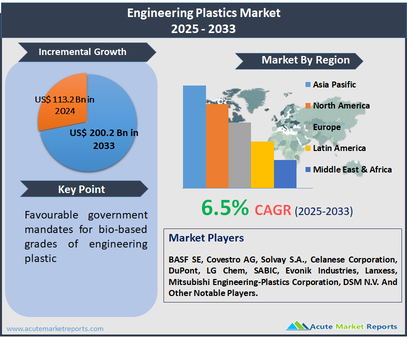

In 2025, the size of the engineering plastics market was estimated to be US $113.2 billion, and it is anticipated that the total revenue will expand at a CAGR of 6.54% from 2026 to 2034, reaching almost US $200.2 billion by 2034. Plastics used in engineering are those that have physical qualities that allow them to function effectively for extended periods of time in structural applications, across a broad temperature range, while being subjected to mechanical stress, and in challenging chemical and physical conditions. In the manufacturing of mechanical parts, container construction, and the packaging of various substances, engineering plastics are typically utilised. Due to the fact that they are far lighter than both metal and ceramic, they have found widespread application as a favoured alternative to the former. In addition to this, they offer great load capacity, mechanical strength, thermal stability, and longevity, as well as flexible design options. Polysulphone, polyamides (PA), polycarbonates (PC), acrylonitrile butadiene styrene (ABS), and acrylonitrile butadiene styrene (PA) are some examples of the several types of technical plastics that are frequently utilised (PSU).

Favourable government mandates for bio-based grades of engineering plastic

Metals are being replaced in automobiles by a variety of engineering plastics as a result of increasingly rigorous laws aimed at lowering emission levels and increasing fuel economy. OEMs (Original Equipment Manufacturers) are doing this in response to these regulations. Recent breakthroughs have led to the creation of bio-based grades of various engineering plastics. These bio-based grades are now available. It is anticipated that the expansion of the engineering plastics market would be driven by these factors. Applications for bio-based engineered plastics such as PLA, PHA, and PET have found a tremendous breadth of use in the packaging, food service ware, bag, and agricultural industries. There is a growing demand for products derived from bio-based materials, which has led to an increase in the number of sellers who offer bio-based engineering plastics on the market.

Need for electric and hybrid vehicles presents opportunity for the new entrants in this market

Because of the growing need for engineering plastics and the plethora of new applications for these materials, this industry already has a significant number of participants due to the fact that it is so versatile. an increasing number of global and local players in each nation. This increase in competition, when combined with the high level of market fragmentation that already exists for engineering plastics, is symptomatic of how desirable the market now is.

Fluctuation in raw material prices

It is projected that the high costs of engineering plastics, which are caused by variations in the costs of raw materials, will be an impediment to the expansion of the market for engineering plastics. This is due to the fact that engineering plastics are made from raw materials. Both the more advanced properties of engineering plastics and the more complicated production of those polymers contribute to the higher total cost of engineering plastics. Engineering plastics can be broken down into three categories: As a direct consequence of this, it is projected that the high price of engineering plastics will slow down the growth of the industry.

Market Segmentation by Plastic Type

The polyacetals (POM) segment is anticipated to experience the largest compound annual growth rate of 12.21% during forecast period. Formaldehyde polymerization results in the production of an engineering plastic known as polyacetal, which is also frequently referred to as polyoxymethylene (POM). It has great mechanical, thermal, chemical, and electrical capabilities and is resistant to high temperatures, solvents, and abrasion. Additionally, it has a wide range of electrical properties. Because it is resistant to a wide variety of solvents in addition to having great electrical qualities, it is an ideal material for use in applications involving electricity. Polyoxymethylene's properties make it ideally suited for application in industrial machinery, electrical and electronic equipment, automotive and transportation, as well as consumer items, which contributes to the expansion of the engineering plastics industry.

Market Segmentation by End-use

It is anticipated that the automotive and transportation segment would hold the greatest market share of 33% by the year 2034. In the automotive industry, engineering plastics are used for a variety of applications, including interior and exterior furnishings, motor trains, chassis, electrical components, and objects found under the hood. It is utilised in the construction of components like as dashboards, bumpers, seats, body panels, fuel systems, interior trim, under-bonnet components, lights, external trim, liquid reservoirs, and upholstery. It is anticipated that current environmental and economic concerns will lead to an increase in demand for lightweight engineering plastic, which, in turn, would boost market growth in the industry that has been analysed.

Regional Insights

The Asia Pacific region is anticipated to hold the largest share of the engineering plastics market. It is anticipated that the Asia Pacific region will hold the greatest market share of 38% by the year 2034. The markets in the region are expanding at a rapid rate as a direct result of the rising levels of demand coming from countries such as China, Japan, and India. It is anticipated that China will constitute the most lucrative market for engineering plastics in the Asia Pacific and India will be the market with the quickest growth rate in both the region and the world. As a result of the expansion of the automotive, electrical, and electronics sectors, as well as the fabrication of semiconductors and the export of televisions and other consumer appliances, there has been a significant increase in the demand for engineering plastics.

Competition to Intensify Among the Key Players During the Forecast Period

The market for engineering plastics is moderate to highly competitive and dominated by large companies. The companies BASF SE, Covestro AG, Solvay S.A., Celanese Corporation, DuPont, LG Chem, SABIC, Evonik Industries, Lanxess, Mitsubishi Engineering-Plastics Corporation, DSM N.V. are among the most significant competitors in this market. Researchers from all over the world are focusing their efforts on the development of cutting-edge technologies that will make the process of creating plastics more straightforward. Because of this, the growth of the market during the period of time that is expected to follow will benefit.

Historical & Forecast Period

This study report represents analysis of each segment from 2024 to 2034 considering 2025 as the base year. Compounded Annual Growth Rate (CAGR) for each of the respective segments estimated for the forecast period of 2026 to 2034.

The current report comprises of quantitative market estimations for each micro market for every geographical region and qualitative market analysis such as micro and macro environment analysis, market trends, competitive intelligence, segment analysis, porters five force model, top winning strategies, top investment markets, emerging trends and technological analysis, case studies, strategic conclusions and recommendations and other key market insights.

Research Methodology

The complete research study was conducted in three phases, namely: secondary research, primary research, and expert panel review. key data point that enables the estimation of Engineering Plastics Market By Plastic Type (Acrylonitrile Butadiene Styrene (ABS), Polyamides, Thermoplastic Polyesters, Polycarbonates, Polyacetals, Fluoropolymers, Others), By End-use (Automotive, Electrical & Electronics, Packaging, Consumer appliances, Constructions, Medical, Others) - Growth, Share, Opportunities & Competitive Analysis, 2026 - 2034 market are as follows:

Market forecast was performed through proprietary software that analyzes various qualitative and quantitative factors. Growth rate and CAGR were estimated through intensive secondary and primary research. Data triangulation across various data points provides accuracy across various analyzed market segments in the report. Application of both top down and bottom-up approach for validation of market estimation assures logical, methodical and mathematical consistency of the quantitative data.

| ATTRIBUTE | DETAILS |

|---|---|

| Research Period | 2024-2034 |

| Base Year | 2025 |

| Forecast Period | 2026-2034 |

| Historical Year | 2024 |

| Unit | USD Million |

| Segmentation | |

Plastic Type

|

|

End-use

|

|

|

Region Segment (2024-2034; US$ Million)

|

Key questions answered in this report