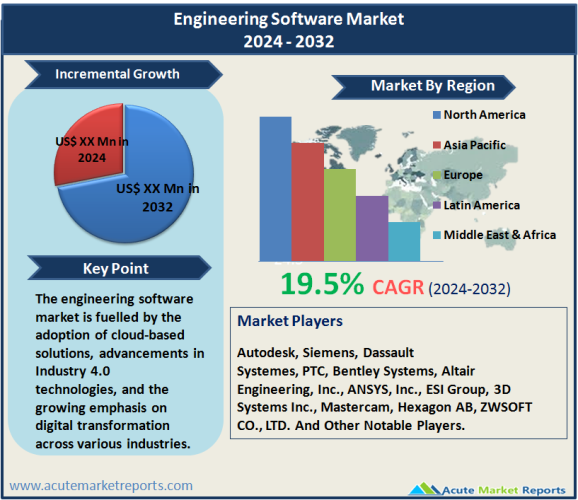

The engineering software market is expected to grow at a CAGR of 19.5% during the forecast period of 2026 to 2034, fuelled by the adoption of cloud-based solutions, advancements in Industry 4.0 technologies, and the growing emphasis on digital transformation across various industries. Despite the challenges associated with the high cost and complexity of implementation, the market offers substantial growth opportunities, particularly in regions like Asia-Pacific, where rapid economic growth and rising demand for advanced engineering solutions are driving the adoption of engineering software. The detailed analysis of market segmentation by component reveals that the Software segment generated the highest revenue in 2025, while the Services segment is expected to witness the highest CAGR during the forecast period. In terms of deployment, the On-premises segment led the market in 2025, whereas the Cloud segment is projected to register the highest growth rate from 2026 to 2034. Geographic trends indicate that North America generated the highest revenue in 2025, while the Asia-Pacific region is expected to experience the highest CAGR during the forecast period. The competitive landscape is marked by the presence of key players such as Autodesk, Siemens, Dassault Systemes, PTC, and Bentley Systems, who are adopting strategic initiatives to strengthen their market positions. As industries continue to innovate and adopt new technologies, the demand for advanced and reliable engineering software solutions is expected to remain strong, driving market growth during the forecast period.

Market Drivers

Increasing Adoption of Cloud-Based Solutions

One of the primary drivers of the engineering software market is the increasing adoption of cloud-based solutions. Cloud computing offers numerous advantages, including scalability, flexibility, and cost-efficiency, making it an attractive option for businesses of all sizes. In 2025, the adoption of cloud-based engineering software solutions saw a significant increase as companies sought to leverage the benefits of cloud infrastructure to enhance their operations. For instance, Autodesk, a leading player in the engineering software market, reported a substantial rise in the subscription of its cloud-based solutions, such as AutoCAD and Revit, driven by the growing demand for remote collaboration and access to design tools from anywhere. Cloud-based engineering software enables seamless collaboration among teams, improves data accessibility, and reduces the need for expensive on-premises infrastructure. Additionally, it allows companies to scale their operations based on demand, providing a cost-effective solution for managing engineering tasks. The integration of cloud-based solutions with other technologies such as AI and ML further enhances their capabilities, enabling predictive analytics and automated decision-making. This trend is expected to continue during the forecast period of 2026 to 2034, with the cloud segment anticipated to witness the highest CAGR due to the ongoing digital transformation initiatives and the increasing reliance on cloud infrastructure across various industries. The shift towards cloud-based solutions is driven by the need for operational efficiency, cost reduction, and improved collaboration, making it a key driver of the engineering software market.

Rise of Industry 4.0

The advent of Industry 4.0, characterized by the integration of digital technologies into manufacturing and industrial processes, is another significant driver of the engineering software market. Industry 4.0 encompasses a range of technologies, including the Internet of Things (IoT), AI, ML, and big data analytics, which are transforming the way industries operate. In 2025, the adoption of Industry 4.0 technologies saw a substantial increase, driving the demand for advanced engineering software solutions that support smart manufacturing and automation. Siemens, a leading provider of engineering software, reported a significant rise in the adoption of its Industry 4.0 solutions, such as Siemens Digital Industries Software, driven by the need for efficient and intelligent manufacturing processes. Engineering software plays a crucial role in the implementation of Industry 4.0 by enabling the design and simulation of complex systems, optimizing production processes, and improving product quality. The integration of AI and ML algorithms into engineering software allows for predictive maintenance, real-time monitoring, and automated decision-making, enhancing overall operational efficiency. The rise of smart factories and the increasing use of digital twins, which are virtual replicas of physical assets, further drive the demand for advanced engineering software solutions. As industries continue to embrace Industry 4.0 technologies, the demand for engineering software is expected to grow, contributing to the market's expansion during the forecast period.

Emphasis on Digital Transformation

The growing emphasis on digital transformation across various industries is a key driver of the engineering software market. Digital transformation involves the integration of digital technologies into all aspects of a business, fundamentally changing how companies operate and deliver value to their customers. In 2025, businesses across sectors, including automotive, aerospace, electronics, and construction, increasingly adopted digital transformation initiatives to stay competitive and meet evolving customer demands. Engineering software is a critical enabler of digital transformation, providing the tools and capabilities required to digitize design and manufacturing processes. For instance, Dassault Systemes, a leading engineering software provider, reported a significant increase in the adoption of its 3DEXPERIENCE platform, driven by the need for digital continuity and collaboration across the product lifecycle. Engineering software solutions facilitate the creation of digital models, simulations, and analyses, enabling companies to optimize their operations and reduce time-to-market. The use of digital twins and virtual simulations allows for the testing and validation of designs in a virtual environment, reducing the need for physical prototypes and minimizing costs. Additionally, the integration of AI and ML technologies into engineering software enables predictive analytics and data-driven decision-making, further enhancing operational efficiency. The ongoing digital transformation initiatives and the increasing reliance on digital technologies are expected to drive the demand for engineering software, contributing to the market's growth during the forecast period.

Restraint

High Cost of Software and Complexity of Implementation

Despite the numerous benefits and advancements associated with engineering software, the market faces challenges related to the high cost of software and the complexity of implementation. Engineering software solutions, particularly those that offer advanced capabilities and integrations, can be expensive, posing a significant barrier to adoption for small and medium-sized enterprises (SMEs). In 2025, several organizations reported difficulties in justifying the high upfront costs and ongoing subscription fees associated with engineering software. The need for specialized hardware, training, and support further adds to the overall cost of implementation. Additionally, the complexity of engineering software, particularly for solutions that integrate multiple technologies such as AI, ML, and IoT, can be daunting for companies lacking the necessary expertise and resources. The configuration, customization, and integration of engineering software with existing systems require skilled personnel and advanced technical knowledge. In 2025, several companies reported challenges in deploying and managing engineering software solutions due to the lack of skilled professionals and the complexity of the technology. These challenges can hinder the adoption of engineering software, particularly among SMEs with limited budgets and technical resources. To address these challenges, vendors are focusing on developing user-friendly and cost-effective solutions with simplified interfaces and extensive support services. However, until these challenges are fully addressed, the high cost and complexity of implementation are likely to restrain the growth of the engineering software market, particularly in regions and industries with limited access to skilled professionals and financial resources.

Market by Component

The engineering software market is segmented by component into Software and Services. In 2025, the Software segment generated the highest revenue due to the widespread adoption of engineering software solutions across various industries. Engineering software provides the necessary tools and capabilities to design, simulate, analyze, and manage engineering projects, making it an essential component of modern engineering processes. Leading vendors such as Autodesk, Dassault Systemes, Siemens, and PTC offer a comprehensive range of engineering software solutions that cater to different industries and applications. The increasing demand for automation, digitalization, and optimization in engineering tasks is driving the adoption of engineering software, resulting in significant revenue generation. In 2025, Autodesk reported substantial revenue growth from its engineering software solutions, driven by the growing adoption of its AutoCAD and Revit platforms in architecture, engineering, and construction (AEC) sectors. However, during the forecast period of 2026 to 2034, the segment expected to witness the highest CAGR is Services. The growing complexity of engineering projects and the need for specialized expertise are driving the demand for professional services, including consulting, training, support, and implementation services. Engineering software vendors are increasingly offering a range of services to help organizations successfully deploy and manage their software solutions, ensuring optimal performance and efficiency. Leading service providers such as IBM, HPE, and Accenture are offering a range of engineering services, including project management, system integration, and custom development, to help organizations navigate the complexities of engineering software. The increasing reliance on managed services and the need for specialized expertise in engineering tasks are expected to drive the growth of the Services segment, resulting in the highest CAGR during the forecast period. The focus on enhancing operational efficiency, reducing downtime, and ensuring optimal performance is further contributing to the demand for engineering services, driving market growth.

Market by Deployment

The engineering software market is segmented by deployment into Cloud and On-premises. In 2025, the On-premises segment generated the highest revenue due to the continued preference for on-premises solutions in industries with stringent security and compliance requirements. On-premises engineering software solutions offer greater control over data and infrastructure, making them suitable for industries such as aerospace and defense, healthcare, and government, where data security is paramount. Leading vendors such as Siemens, Dassault Systemes, and PTC offer robust on-premises engineering software solutions that cater to the specific needs of these industries. In 2025, Siemens reported significant revenue growth from its on-premises engineering software solutions, driven by the increasing demand for secure and compliant software in critical industries. However, during the forecast period of 2026 to 2034, the segment expected to witness the highest CAGR is Cloud. The growing adoption of cloud computing and the increasing demand for scalable and flexible software solutions are driving the shift toward cloud-based engineering software. Cloud-based solutions offer numerous advantages, including cost-efficiency, scalability, and remote accessibility, making them an attractive option for businesses of all sizes. The integration of cloud-based engineering software with other technologies such as AI and ML further enhances their capabilities, enabling predictive analytics and automated decision-making. In 2025, leading vendors such as Autodesk, Dassault Systemes, and Bentley Systems reported substantial growth in the adoption of their cloud-based engineering software solutions, driven by the increasing demand for remote collaboration and access to design tools from anywhere. The ongoing digital transformation initiatives and the increasing reliance on cloud infrastructure across various industries are expected to drive the demand for cloud-based engineering software, resulting in the highest CAGR during the forecast period. The shift towards cloud-based solutions is driven by the need for operational efficiency, cost reduction, and improved collaboration, making it a key driver of the engineering software market.

Market by Application

The engineering software market is segmented by application into Design Automation, Product Design & Testing, Plant Design, Drafting & 3D Modeling, and Others. In 2025, the Product Design & Testing segment generated the highest revenue due to the increasing demand for software solutions that enable the design, simulation, and testing of products across various industries. Product design and testing software provides the necessary tools to create, validate, and optimize designs, ensuring product quality and performance. Leading vendors such as Siemens, Dassault Systemes, and PTC offer comprehensive product design and testing solutions that cater to different industries and applications. In 2025, Dassault Systemes reported significant revenue growth from its product design and testing solutions, driven by the growing adoption of its CATIA and SIMULIA platforms in the automotive, aerospace, and electronics sectors. However, during the forecast period of 2026 to 2034, the segment expected to witness the highest CAGR is Drafting& 3D Modeling. The increasing demand for accurate and detailed 3D models, coupled with the growing adoption of 3D printing and additive manufacturing technologies, is driving the demand for drafting and 3D modeling software. Drafting and 3D modeling software provides the necessary tools to create precise and detailed designs, enabling efficient manufacturing processes and reducing the need for physical prototypes. Leading vendors such as Autodesk, Bentley Systems, and Trimble offer advanced drafting and 3D modeling solutions that cater to different industries and applications. The integration of AI and ML technologies into drafting and 3D modeling software further enhances their capabilities, enabling automated design generation and optimization. In 2025, Autodesk reported substantial growth in the adoption of its drafting and 3D modeling solutions, driven by the increasing demand for digital twins and virtual simulations in architecture, engineering, and construction (AEC) sectors. The ongoing digital transformation initiatives and the increasing reliance on digital technologies are expected to drive the demand for drafting and 3D modeling software, resulting in the highest CAGR during the forecast period. The focus on enhancing design accuracy, reducing time-to-market, and improving product quality is further contributing to the demand for drafting and 3D modeling software, driving market growth.

Market by End-Use

The engineering software market is segmented by end-use into Automotive, Aerospace & Defense, Electronics, Medical Devices, Architecture, Engineering, and Construction (AEC), and Others. In 2025, the Automotive segment generated the highest revenue due to the extensive use of engineering software in the design, simulation, and testing of automotive components and systems. The automotive industry relies heavily on engineering software to ensure product quality, performance, and compliance with regulatory standards. Leading vendors such as Siemens, Dassault Systemes, and PTC offer comprehensive engineering software solutions that cater to the specific needs of the automotive industry. In 2025, Siemens reported significant revenue growth from its engineering software solutions, driven by the increasing adoption of its NX and Simcenter platforms in the automotive sector. However, during the forecast period of 2026 to 2034, the segment expected to witness the highest CAGR is Medical Devices. The medical devices industry is increasingly adopting engineering software to enhance the design, simulation, and testing of medical devices, ensuring product safety and efficacy. The need for accurate and reliable design tools, coupled with the growing emphasis on regulatory compliance, is driving the demand for engineering software in the medical devices sector. Leading vendors such as Autodesk, Dassault Systemes, and ANSYS offer advanced engineering software solutions that cater to the specific needs of the medical devices industry. In 2025, several medical device manufacturers reported significant investments in engineering software solutions to support their product development and regulatory compliance efforts. The ongoing digital transformation initiatives and the increasing reliance on digital technologies are expected to drive the demand for engineering software in the medical devices sector, resulting in the highest CAGR during the forecast period. The focus on enhancing product safety, improving design accuracy, and ensuring regulatory compliance is further contributing to the demand for engineering software, driving market growth.

Geographic Trends

The geographic segmentation of the engineering software market reveals significant trends and regional dynamics. In 2025, North America generated the highest revenue, driven by the extensive adoption of engineering software solutions in the United States and Canada. The region's focus on enhancing digital infrastructure, technological advancements, and the strong presence of leading vendors have been major contributors to this growth. The United States, in particular, has been a leader in adopting engineering software, with significant investments in research and development. For example, major technology companies such as Autodesk, Siemens, and PTC have been at the forefront of engineering software innovation, driving its adoption across various industries. The favorable regulatory environment, advanced technological infrastructure, and substantial government funding have further supported the growth of the market in North America. However, during the forecast period of 2026 to 2034, the region expected to witness the highest CAGR is Asia-Pacific. The rapid economic growth, increasing urbanization, and rising demand for advanced engineering solutions in countries like China, India, Japan, and South Korea are driving the adoption of engineering software. Governments in Asia-Pacific are focusing on modernizing their digital infrastructure and enhancing technological capabilities to support the growing demand for digital services. China's extensive investments in digital infrastructure, driven by its Belt and Road Initiative, are contributing to the high growth potential in the region. In 2025, China's Ministry of Industry and Information Technology announced plans to deploy advanced engineering software solutions across major cities and industrial zones, enhancing the overall digital infrastructure. Similarly, India is witnessing significant investments in digital infrastructure to support its economic growth and ensure efficient connectivity. The growing emphasis on smart city initiatives and the need for efficient engineering solutions in urban environments are further driving the demand for engineering software in Asia-Pacific. As a result, the region is expected to lead the market in terms of growth rate during the forecast period, driven by the need for advanced and reliable engineering solutions to address the evolving demands and challenges.

Competitive Trends

The competitive landscape of the engineering software market is characterized by the presence of several key players, including Autodesk, Siemens, Dassault Systemes, PTC, Bentley Systems, Altair Engineering, Inc., ANSYS, Inc., ESI Group, 3D Systems Inc., Mastercam, Hexagon AB and ZWSOFT CO., LTD. In 2025, these companies dominated the market due to their extensive product portfolios, strong brand recognition, and widespread distribution networks. Autodesk led the market with its advanced engineering software solutions, known for their high performance and reliability. The company's strategic focus on research and development, along with its partnerships with various technology providers and cloud service providers worldwide, has strengthened its market position. For example, Autodesk's AutoCAD and Revit platforms are widely used in major architecture, engineering, and construction (AEC) projects across North America, Europe, and Asia-Pacific, contributing to significant revenue generation. Siemens, another major player, has been focusing on expanding its engineering software offerings and enhancing its technological capabilities. Siemens' NX and Simcenter platforms, which integrate advanced engineering tools and capabilities, are renowned for their efficiency and operational flexibility, making them a popular choice for various engineering applications globally. The company's strong presence in the automotive and aerospace sectors has further bolstered its market share. Dassault Systemes has also made significant strides in the engineering software market with its comprehensive range of solutions, including CATIA, SOLIDWORKS, and SIMULIA. Dassault's emphasis on innovation and customer-centric solutions has positioned it as a key player in the market, with notable projects in the automotive, aerospace, and electronics sectors. PTC and Bentley Systems are also important contributors to the market, offering a range of advanced engineering software solutions and focusing on expanding their presence in emerging markets. The competitive trends highlight a growing focus on mergers and acquisitions, strategic partnerships, and collaborations among key players. These strategies are aimed at expanding product portfolios, enhancing technological capabilities, and gaining access to new markets. For instance, partnerships between engineering software providers and cloud service providers facilitate the development of customized solutions that address specific operational challenges in various industries. As the demand for advanced engineering solutions continues to grow, the competitive landscape of the engineering software market is expected to remain dynamic, with companies focusing on innovation, strategic investments, and expanding their global footprint to maintain and enhance their market positions.

Historical & Forecast Period

This study report represents analysis of each segment from 2024 to 2034 considering 2025 as the base year. Compounded Annual Growth Rate (CAGR) for each of the respective segments estimated for the forecast period of 2026 to 2034.

The current report comprises of quantitative market estimations for each micro market for every geographical region and qualitative market analysis such as micro and macro environment analysis, market trends, competitive intelligence, segment analysis, porters five force model, top winning strategies, top investment markets, emerging trends and technological analysis, case studies, strategic conclusions and recommendations and other key market insights.

Research Methodology

The complete research study was conducted in three phases, namely: secondary research, primary research, and expert panel review. key data point that enables the estimation of Engineering Software Market By Component (Software, Services), By Deployment (Cloud, On-premises), By Application (Design Automation, Product Design & Testing, Plant Design, Drafting & 3D Modeling, Others), By End-Use (Automotive, Aerospace & Defense, Electronics, Medical Devices, Architecture, Engineering, and Construction (AEC), Others) - Growth, Share, Opportunities & Competitive Analysis, 2026 - 2034 market are as follows:

Market forecast was performed through proprietary software that analyzes various qualitative and quantitative factors. Growth rate and CAGR were estimated through intensive secondary and primary research. Data triangulation across various data points provides accuracy across various analyzed market segments in the report. Application of both top down and bottom-up approach for validation of market estimation assures logical, methodical and mathematical consistency of the quantitative data.

| ATTRIBUTE | DETAILS |

|---|---|

| Research Period | 2024-2034 |

| Base Year | 2025 |

| Forecast Period | 2026-2034 |

| Historical Year | 2024 |

| Unit | USD Million |

| Segmentation | |

Component

|

|

Deployment

|

|

Application

|

|

End-Use

|

|

|

Region Segment (2024-2034; US$ Million)

|

Key questions answered in this report