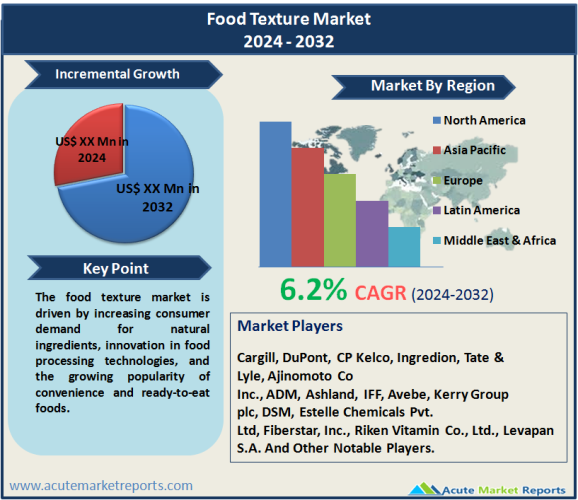

The food texture market is expected to grow at a CAGR of 6.2% during the forecast period of 2026 to 2034, driven by increasing consumer demand for natural ingredients, innovation in food processing technologies, and the growing popularity of convenience and ready-to-eat foods. Despite regulatory challenges related to labeling requirements and ingredient classification, the market remains dynamic and competitive, with opportunities for companies to differentiate through product innovation and strategic partnerships. Regional variations in consumer preferences and market dynamics further underscore the importance of understanding local trends and tailoring strategies accordingly. As the food industry continues to evolve, texture will remain a critical determinant of product success, highlighting the significance of texture-modifying ingredients in delivering superior sensory experiences and meeting consumer expectations for quality, taste, and convenience.

Key Market Drivers

Increasing Consumer Demand for Natural Ingredients

Consumer preferences have shifted towards natural and clean-label products, prompting food manufacturers to prioritize natural ingredients in their formulations. This trend is particularly evident in the food texture market, where products derived from natural sources such as cellulose derivatives, gums, and pectin are witnessing heightened demand. Consumers are increasingly seeking food products with recognizable and minimally processed ingredients, driving the adoption of natural texture enhancers. For instance, the rising popularity of plant-based alternatives has spurred the demand for gums and starches derived from sources like guar gum and tapioca starch. Furthermore, natural texture ingredients offer functional benefits such as improved mouthfeel and stability, aligning with consumers' health and wellness aspirations. Companies leveraging natural ingredients in their product portfolios are expected to gain a competitive edge, capitalizing on this burgeoning consumer trend.

Innovation in Food Processing Technologies

Advancements in food processing technologies are revolutionizing the texture modification landscape, enabling manufacturers to enhance product quality and sensory attributes. Novel techniques such as extrusion, microencapsulation, and emulsification have expanded the possibilities for texture manipulation, facilitating the development of innovative food products across various categories. These technologies enable precise control over parameters such as viscosity, elasticity, and particle size distribution, allowing manufacturers to tailor textures according to consumer preferences. For example, the use of high-pressure processing (HPP) has gained traction for preserving the texture of fresh foods while extending shelf life, and meeting the demand for minimally processed and convenient products. Additionally, techniques like ultrasound-assisted extraction (UAE) offer efficient extraction of texture-modifying compounds from natural sources, contributing to the formulation of clean-label products with superior textural properties.

Growing Demand for Convenience and Ready-to-Eat Foods

The busy lifestyles of modern consumers have fueled the demand for convenience foods that offer quick preparation and on-the-go consumption. This trend has significantly impacted the food texture market, driving the need for texture-modifying ingredients that enhance the sensory experience of ready-to-eat and processed foods. Manufacturers are incorporating texturizers such as gelatin, starch, and inulin to improve the mouthfeel, viscosity, and stability of convenience food products like soups, sauces, and ready meals. Moreover, the rising popularity of snacking occasions has created opportunities for texture innovation in snack formulations, with a focus on crispiness, crunchiness, and indulgent textures. As consumers seek convenient yet indulgent food options, manufacturers are increasingly investing in texture technologies to meet these evolving preferences and differentiate their product offerings in a competitive market landscape.

Restraint

Regulatory Challenges and Labeling Requirements

Despite the growing demand for natural ingredients, the food texture market faces challenges related to regulatory compliance and labeling requirements. Government regulations regarding the use of additives, stabilizers, and emulsifiers impose stringent guidelines on food manufacturers, limiting the formulation options available for achieving desired textures. Additionally, evolving consumer perceptions towards food additives and artificial ingredients have prompted regulatory bodies to enforce stricter labeling standards, necessitating transparent disclosure of texture-modifying agents on product labels. Compliance with these regulations poses logistical and formulation challenges for manufacturers, impacting product development timelines and potentially limiting the market growth of certain texture ingredients. Moreover, the ambiguity surrounding the classification of certain ingredients as natural or synthetic further complicates regulatory compliance efforts, posing a significant restraint to market expansion.

Market Segmentation Analysis

Market by Type

Among the various types of texture-modifying ingredients, cellulose derivatives emerged as the highest revenue-generating segment in 2025, driven by their widespread applications in food and beverage formulations. Cellulose derivatives exhibit versatile functionality as thickeners, stabilizers, and bulking agents, catering to diverse product categories such as dairy, bakery, and processed foods. Additionally, cellulose derivatives offer benefits such as improved texture, moisture retention, and fat replacement, addressing consumer demand for healthier and functional food options. Meanwhile, inulin registered the highest compound annual growth rate (CAGR) during the forecast period of 2026 to 2034, attributed to its increasing utilization in functional food and dietary supplement applications. With rising awareness of prebiotic fibers and digestive health benefits, inulin is experiencing heightened demand as a texturizing agent in various food products, including beverages, snacks, and bakery goods.

Market by Source

The market segmentation by source reveals natural ingredients as the dominant revenue contributor in 2025, reflecting consumer preferences for clean-label and minimally processed foods. Natural texture ingredients such as gums, pectin, and gelatin are favored by consumers seeking authentic and wholesome food experiences, driving their widespread adoption across food and beverage applications. Conversely, synthetic texture modifiers witnessed a higher CAGR during the forecast period, fueled by technological advancements and cost-effective formulations. Synthetic ingredients offer functional benefits such as enhanced stability, texture uniformity, and prolonged shelf life, appealing to manufacturers seeking efficient solutions for texture optimization. Despite regulatory scrutiny and consumer skepticism towards synthetic additives, technological innovations continue to drive the market penetration of synthetic texture modifiers, especially in processed and convenience food segments.

Market by Form

The segmentation by form indicates dry texture ingredients as the leading revenue contributor in 2025, owing to their versatility and ease of handling in food processing operations. Dry ingredients such as starches, dextrins, and cellulose powders are widely utilized for their functional properties, including thickening, binding, and moisture control. These ingredients find extensive applications in bakery, confectionery, and savory products, where precise texture control is essential for product quality and consistency. Conversely, the liquid texture ingredient segment exhibited a higher CAGR during the forecast period, driven by the growing demand for liquid formulations in beverages, sauces, and dressings. Liquid texturizers offer advantages such as rapid dispersion, homogenous blending, and improved sensory attributes, catering to manufacturers seeking convenient solutions for texture modification and product differentiation.

Market by Application

The segmentation by application highlights bakery and confectionery products as the primary revenue-generating segment in 2025, driven by the widespread use of texture modifiers to enhance product quality and sensory appeal. Texture ingredients such as gums, starches, and hydrocolloids play a crucial role in optimizing texture parameters such as mouthfeel, structure, and shelf stability in baked goods and confections. Meanwhile, the meat and poultry products segment exhibited the highest CAGR during the forecast period, driven by the growing demand for processed meat alternatives and value-added protein products. Texture modifiers such as gelling agents, emulsifiers, and stabilizers enable manufacturers to improve the texture, juiciness, and bite characteristics of meat analogs and convenience meat products, catering to evolving consumer preferences for plant-based protein options and convenient meal solutions.

Market by Functionality

In terms of functionality, thickening agents emerged as the leading revenue contributor in 2025, driven by their extensive applications in food and beverage formulations requiring viscosity control and texture enhancement. Thickening agents such as starches, gums, and cellulose derivatives are utilized across various product categories, including soups, sauces, dressings, and dairy products, to achieve desired textural attributes and sensory experiences. Conversely, emulsifying agents exhibited the highest CAGR during the forecast period, attributed to their critical role in stabilizing oil-in-water and water-in-oil emulsions in food and beverage systems to ensure product uniformity, stability, and sensory appeal. Emulsifiers such as lecithin, mono- and diglycerides, and polysorbates play a vital role in preventing ingredient separation, enhancing mouthfeel, and prolonging product shelf life, especially in emulsion-based formulations like dressings, spreads, and dairy alternatives. Moreover, the demand for natural emulsifiers derived from plant sources is on the rise, driven by consumer preferences for clean labels and sustainable ingredients. Manufacturers are exploring plant-based alternatives to traditional emulsifiers, such as soy lecithin and sunflower lecithin, to meet regulatory requirements and consumer expectations for transparent labeling.

North America Remains the Global Leader

Geographic trends in the food texture market reflect regional variations in consumer preferences, dietary habits, and market dynamics. North America emerged as the region with the highest revenue in 2025, driven by the robust demand for texture-modifying ingredients in a diverse range of food and beverage applications. The region's mature food industry, coupled with a strong emphasis on product innovation and premiumization, contributed to the dominance of North America in terms of market share. However, Asia-Pacific is expected to exhibit the highest CAGR during the forecast period, fueled by rapid urbanization, changing lifestyles, and growing disposable incomes. The burgeoning food and beverage sector in countries like China, India, and Japan presents lucrative opportunities for texture ingredient manufacturers, particularly in segments such as convenience foods, snacks, and functional beverages. Moreover, increasing consumer awareness of health and wellness trends is driving demand for texture-modified products with clean-label formulations and natural ingredients, further propelling market growth in the Asia-Pacific region.

Market Competition to Intensify during the Forecast Period

In the competitive landscape of the food texture market, several key players are implementing strategic initiatives to strengthen their market position and capitalize on emerging opportunities. Leading companies such as Cargill, DuPont, CP Kelco, Ingredion, Tate & Lyle, Ajinomoto Co Inc., ADM, Ashland, IFF, Avebe, Kerry Group plc, DSM, Estelle Chemicals Pvt. Ltd, Fiberstar, Inc., Riken Vitamin Co., Ltd., and Levapan S.A. are actively engaged in product innovation, portfolio diversification, and strategic partnerships to gain a competitive edge in the market. These companies leverage their extensive research and development capabilities to develop novel texture solutions that cater to evolving consumer preferences and industry trends. For example, CP Kelco focuses on expanding its portfolio of plant-based texturizers and clean-label ingredients to meet the growing demand for natural and sustainable products. Similarly, Cargill emphasizes collaboration with food manufacturers to co-create texture solutions tailored to specific product applications and regional preferences. Moreover, DuPont's acquisition of International Flavors & Fragrances (IFF) strengthens its position in the texture ingredients market, enabling synergies in product development and customer engagement. Overall, the competitive landscape of the food texture market is characterized by innovation, collaboration, and strategic alliances among key players striving to maintain market leadership and drive future growth.

Historical & Forecast Period

This study report represents analysis of each segment from 2024 to 2034 considering 2025 as the base year. Compounded Annual Growth Rate (CAGR) for each of the respective segments estimated for the forecast period of 2026 to 2034.

The current report comprises of quantitative market estimations for each micro market for every geographical region and qualitative market analysis such as micro and macro environment analysis, market trends, competitive intelligence, segment analysis, porters five force model, top winning strategies, top investment markets, emerging trends and technological analysis, case studies, strategic conclusions and recommendations and other key market insights.

Research Methodology

The complete research study was conducted in three phases, namely: secondary research, primary research, and expert panel review. key data point that enables the estimation of Food Texture Market By Type (Cellulose Derivatives, Gums, Pectin, Gelatin, Starch, Inulin, Dextrin, Other Types), By Source (Natural, Synthetic), By Form (Dry, Liquid), By Application (Bakery & Confectionery Products, Dairy & Frozen Foods, Meat & Poultry Products, Beverages, Snacks & Savory, Sauces & Dressings, Other Applications), By Functionality (Thickening, Gelling, Emulsifying, Stabilizing, Other Functionalities) - Growth, Share, Opportunities & Competitive Analysis, 2026 - 2034 market are as follows:

Market forecast was performed through proprietary software that analyzes various qualitative and quantitative factors. Growth rate and CAGR were estimated through intensive secondary and primary research. Data triangulation across various data points provides accuracy across various analyzed market segments in the report. Application of both top down and bottom-up approach for validation of market estimation assures logical, methodical and mathematical consistency of the quantitative data.

| ATTRIBUTE | DETAILS |

|---|---|

| Research Period | 2024-2034 |

| Base Year | 2025 |

| Forecast Period | 2026-2034 |

| Historical Year | 2024 |

| Unit | USD Million |

| Segmentation | |

Type

|

|

Source

|

|

Form

|

|

Application

|

|

Functionality

|

|

|

Region Segment (2024-2034; US$ Million)

|

Key questions answered in this report