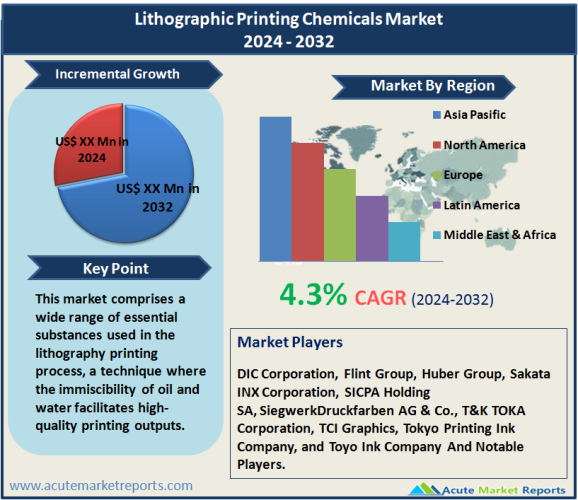

The lithographic printing chemicals market is expected to grow at a CAGR of 4.3% during the forecast period of 2026 to 2034. Lithographic printing chemicals market encompasses a range of substances crucial for the printing process that involves lithography - a printing technique based on the immiscibility of oil and water. These chemicals are integral to maintaining the quality and efficiency of the lithographic printing process. The market has been adapting to changing demands, particularly with the rise of digital media, which influences both the types of chemicals needed and their environmental impact. Lithographic printing is predominantly used for high-volume items such as newspapers, posters, and books, and the chemicals involved include fountain solutions, inks, plate cleaners, and gum solutions. As the industry evolves, so too does the composition and demand for these chemicals, guided by both technological advancements and regulatory standards aimed at reducing environmental footprints.

Driver 1: Increasing Demand for High-Quality Printed Packaging

Growth in Packaging Industries

The demand for high-quality printed packaging is a significant driver for the lithographic printing chemicals market. As global consumerism increases, so does the need for attractive packaging that can lure customers at point-of-sale locations. The packaging industry's growth, especially in food and beverage, personal care, and healthcare sectors, directly correlates with higher consumption of lithographic printing chemicals. These sectors require precise and high-quality printing to create vibrant and detailed graphics that are crucial for brand identity and product information.

Technological Advancements in Printing Techniques

Technological advancements have enabled lithographic printing to achieve higher standards of print quality and speed, thereby enhancing production efficiency. Modern lithographic presses can handle a variety of substrates and ink formulations, which are less harmful to the environment while maintaining the vibrancy and durability of the prints. This compatibility with various high-performance inks and substrates has expanded the applicability of lithographic printing in packaging, further propelling the chemical market.

Impact of E-commerce

E-commerce has been a game-changer in the packaging sector, significantly influencing the lithographic printing chemicals market. The shift towards online shopping has increased the demand for shipping boxes, labels, and other packaging materials that require high-quality printing. This trend is anticipated to continue as global e-commerce sales grow, underscoring the importance of durable and visually appealing packaging that withstands shipping and handling while also appealing to consumers.

Driver 2: Regulatory Compliance and Sustainability Initiatives

Stringent Environmental Regulations

The push for environmental sustainability is profoundly influencing the lithographic printing chemicals market. Regulatory bodies worldwide are imposing stricter guidelines on the use of volatile organic compounds (VOCs) and other hazardous substances in printing chemicals. This has driven the development of newer, greener formulations that comply with these regulations while maintaining or enhancing print quality.

Advancements in Eco-friendly Chemicals

Manufacturers are increasingly investing in research and development to produce eco-friendly chemicals that reduce the environmental impact of printing operations. These advancements include water-based inks and sustainable cleaning solutions that offer an eco-friendlier alternative to traditional petroleum-based products. As sustainability becomes a more significant part of corporate responsibility, the demand for these greener lithographic printing chemicals is expected to rise, reflecting a commitment to environmental stewardship and sustainable practices.

Corporate Sustainability Goals

Many companies in the printing sector are setting ambitious sustainability targets to reduce their carbon footprint and promote environmental conservation. This shift is not only a response to regulatory pressure but also a strategic move to appeal to a more eco-conscious consumer base. The increased adoption of sustainable practices in the printing industry is a powerful driver for the lithographic printing chemicals market, as it aligns with global efforts to combat climate change and promote sustainability.

Driver 3: Technological Innovation in Lithographic Printing

Integration of Digital Technologies

The integration of digital technologies into lithographic printing processes represents a significant market driver. Innovations such as computer-to-plate (CTP) systems have streamlined the printing process, reducing chemical waste and improving operational efficiency. These technological advancements have also enhanced the precision and speed of lithographic printing, making it more competitive with digital printing technologies.

Improved Print Quality and Efficiency

Technological innovations have led to the development of faster, more efficient printing presses that support a broader range of chemical formulations and applications. These improvements have enabled printers to produce higher-quality outputs at reduced costs and turnaround times, crucial factors for competitiveness in the printing industry.

Customization and Flexibility

The ability to quickly modify printing plates and adapt chemical formulations has allowed lithographic printers to offer more customized solutions. This flexibility is particularly valuable in a market where print runs are becoming shorter and more tailored to specific customer needs. The ongoing advancements in lithographic technology and chemicals are key drivers in adapting to these market demands, providing both quality and versatility in printing.

Restraint: Decline in Traditional Print Media

Shift to Digital Media

A significant restraint on the lithographic printing chemicals market is the global decline in traditional print media. As digital platforms become the primary source for news, entertainment, and advertising, the demand for printed newspapers, magazines, and brochures has seen a marked decrease. This shift has led to a reduced need for lithographic printing and associated chemicals in these sectors. Despite the growth in packaging and labeling, the overall reduction in traditional print volumes poses challenges to the market's long-term sustainability and growth. The market must continuously innovate and possibly pivot towards areas still reliant on high-quality printing to mitigate this decline.

Market Segmentation by Product

Diverse Product Offerings Fueling Market Growth : In the lithographic printing chemicals market, segmentation by product includes Inks, Fountain Solutions, Cleaning Solutions, and Others. Among these, Inks have traditionally dominated the market in terms of revenue due to their essential role in the printing process and the sheer volume required for large-scale printing operations. The continuous demand for high-quality inks that offer precision, longevity, and vibrant colors supports their leading revenue position. However, the highest Compound Annual Growth Rate (CAGR) is observed in the Fountain Solutions segment. This growth is attributed to innovations aimed at improving the environmental profile of these solutions and enhancing the efficiency and quality of lithographic printing. Fountain solutions are crucial for maintaining the chemical balance on the printing plate, which directly impacts print quality and machine performance. The shift towards more sustainable and efficient fountain solutions is driven by stringent environmental regulations and the industry's push towards reducing volatile organic compound (VOC) emissions. Additionally, the Cleaning Solutions segment is also witnessing significant advancements with the development of eco-friendly and highly effective products that comply with global safety and environmental standards, further supporting the market's growth dynamics.

Market Segmentation by Application

Expanding Applications in Diverse Industries : The application-based segmentation of the lithographic printing chemicals market includes Consumer Electronics, Publication, Packaging, Promotion, and Others. The Packaging sector leads in revenue generation, driven by the increasing demand for consumer goods and the corresponding need for effective and attractive packaging. High-quality printing is critical in this sector to ensure product differentiation and brand recognition in competitive market environments. The highest CAGR, however, is found in the Consumer Electronics segment, where the demand for lithographic printing chemicals is propelled by the need for durable and precise printing on electronic devices and components. This segment benefits from the rapid growth of the electronics industry, where lithographic printing is used not just for packaging but also for creating labels and functional elements on the devices themselves. Both the high revenue from the Packaging segment and the high growth rate in the Consumer Electronics segment highlight the lithographic printing chemicals market's essential role across varied industries, each with unique requirements and growth potentials.

Geographic Trends

The lithographic printing chemicals market exhibits significant geographic diversity, with trends varying widely by region. Asia Pacific leads in both highest revenue and Compound Annual Growth Rate (CAGR), driven by robust manufacturing sectors, particularly in China and India, where rapid industrialization and urbanization have spurred demand for printed materials. The region benefits from a strong presence of key industries such as packaging, publications, and consumer electronics, which extensively utilize lithographic printing. Additionally, Asia Pacific's dominance is supported by increasing investments in printing technologies, a growing consumer base, and rising disposable incomes. Europe and North America also show substantial market activity, characterized by high demand for sustainable and eco-friendly printing chemicals, reflecting stringent environmental regulations prevalent in these regions. These markets are seeing a shift towards greener alternatives, which is influencing global trends in chemical formulations in lithography. The Middle East and Africa, along with Latin America, although smaller in comparison, are expected to show significant growth from 2026 to 2034, driven by expanding urban populations and increasing local manufacturing and industrial activities.

Competitive Trends and Key Strategies among Top Players

In the competitive landscape of the lithographic printing chemicals market, major players such as DIC Corporation, Flint Group, Huber Group, Sakata INX Corporation, SICPA Holding SA, SiegwerkDruckfarben AG & Co., T&K TOKA Corporation, TCI Graphics, Tokyo Printing Ink Company, and Toyo Ink Company are strategically positioning themselves to capitalize on market opportunities. In 2025, these companies collectively exhibited robust revenue generation through a combination of advanced technological implementations and broad product portfolios that cater to the diverse needs of the printing industry. From 2026 to 2034, these top players are expected to continue their dominance by leveraging key strategies such as mergers and acquisitions, global expansion, and increased investment in R&D to develop innovative and environmentally friendly solutions. For instance, DIC Corporation and Flint Group have been focusing on expanding their geographic footprint by establishing new facilities and acquiring regional companies to bolster their market presence. Similarly, companies like SiegwerkDruckfarben AG & Co. and T&K TOKA Corporation are heavily investing in technology to enhance the efficiency and sustainability of their products, aligning with global shifts towards reducing environmental impact. The strategic movements of these companies not only aim to increase their market share but also to set industry standards in terms of quality, sustainability, and innovation, shaping the market dynamics and future growth trajectory. These competitive strategies are crucial for maintaining their leading positions in the market, especially as the demand for eco-friendly and high-performance printing solutions becomes more pronounced.

Historical & Forecast Period

This study report represents analysis of each segment from 2024 to 2034 considering 2025 as the base year. Compounded Annual Growth Rate (CAGR) for each of the respective segments estimated for the forecast period of 2026 to 2034.

The current report comprises of quantitative market estimations for each micro market for every geographical region and qualitative market analysis such as micro and macro environment analysis, market trends, competitive intelligence, segment analysis, porters five force model, top winning strategies, top investment markets, emerging trends and technological analysis, case studies, strategic conclusions and recommendations and other key market insights.

Research Methodology

The complete research study was conducted in three phases, namely: secondary research, primary research, and expert panel review. key data point that enables the estimation of Lithographic Printing Chemicals Market By Product (Inks, Fountain solutions, Cleaning solutions, Others), By Application (Consumer electronics, Publication, Packaging, Promotion, Others) - Growth, Share, Opportunities & Competitive Analysis, 2026 - 2034 market are as follows:

Market forecast was performed through proprietary software that analyzes various qualitative and quantitative factors. Growth rate and CAGR were estimated through intensive secondary and primary research. Data triangulation across various data points provides accuracy across various analyzed market segments in the report. Application of both top down and bottom-up approach for validation of market estimation assures logical, methodical and mathematical consistency of the quantitative data.

| ATTRIBUTE | DETAILS |

|---|---|

| Research Period | 2024-2034 |

| Base Year | 2025 |

| Forecast Period | 2026-2034 |

| Historical Year | 2024 |

| Unit | USD Million |

| Segmentation | |

Product

|

|

Application

|

|

|

Region Segment (2024-2034; US$ Million)

|

Key questions answered in this report