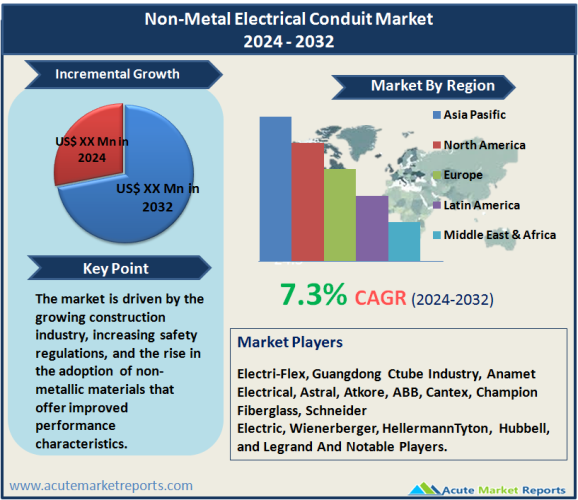

The non-metal electrical conduit market is primarily composed of conduits made from materials such as PVC, HDPE, and fiberglass. These conduits are used to protect and route electrical wiring in a variety of construction applications, offering advantages such as corrosion resistance, flexibility, and reduced weight compared to metal alternatives. The non-metal electrical conduit market is expected to grow at a CAGR of 7.3% during the forecast period of 2026 to 2034. The market is driven by the growing construction industry, increasing safety regulations, and the rise in the adoption of non-metallic materials that offer improved performance characteristics.

Driver 1: Growth in Global Construction Activity

Increasing Infrastructure Projects Globally : A significant driver of the non-metal electrical conduit market is the robust growth in global construction activities. As countries expand their infrastructure to accommodate growing populations and economic expansions, the demand for safe and efficient electrical installations has surged. This trend is particularly noticeable in emerging economies in Asia, Africa, and Latin America, where urbanization and industrialization are driving the construction of residential, commercial, and industrial buildings.

Rising Demand in Residential Construction : In the residential sector, there is a noticeable shift towards modern, energy-efficient, and safer housing solutions. Non-metal conduits, being highly adaptable and resistant to many environmental factors, are increasingly preferred for electrical installations. This shift is underpinned by the increased awareness among consumers and contractors about the benefits of non-metal conduits, including their ease of installation and lower overall maintenance cost.

Driver 2: Enhanced Safety Regulations

Stricter Building Codes and Safety Standards : Another pivotal driver for the non-metal electrical conduit market is the enhancement of safety regulations and building codes across the globe. Governments and regulatory bodies are continuously revising safety standards to reduce electrical hazards and improve building safety. Non-metal conduits, known for their non-conductive properties, significantly contribute to these safety measures by providing enhanced protection against electrical shocks and fires.

Promotion of Non-Conductive Materials : The push towards non-conductive materials in construction to improve safety is also promoting the use of non-metal conduits. Their use is particularly encouraged in environments where the risk of electrical hazards is high, such as in chemical plants, refineries, and other industrial applications where explosive gases or combustible dust may be present.

Driver 3: Technological Advancements in Material Science

Innovation in Conduit Materials : Technological advancements in material science have greatly expanded the capabilities and applications of non-metal electrical conduits. Innovations in thermoplastics and composites have led to the development of conduits that are not only lighter and more flexible but also exhibit superior durability and resistance to harsh environmental conditions.

Adoption of Smart and Sustainable Materials : There is an increasing trend towards the adoption of smart materials in conduit manufacturing that can adapt to environmental changes and offer diagnostics capabilities. Furthermore, the sustainability trend is pushing manufacturers to produce environmentally friendly conduits that contribute to green building certifications and reduce the ecological footprint of construction projects.

Restraint: High Initial Installation Cost

Perceived Cost Barriers : Despite their many advantages, non-metal electrical conduits often come with a higher initial installation cost compared to traditional metal conduits. This can be a significant restraint in the market, particularly in cost-sensitive regions and projects. The cost factor often influences contractors and builders who may opt for lower-cost alternatives, especially in regions where safety regulations are less stringent or where the benefits of non-metal conduits are not fully recognized. This perception impacts the adoption rates of non-metal conduits, although their total lifecycle cost, considering lower maintenance and longer durability, may be lower.

Market Segmentation by Trade Size

The non-metal electrical conduit market is intricately segmented by trade sizes ranging from ½ inch to over 6 inches, each catering to different installation requirements and applications. Among these, the trade sizes of ½ to 1 inch typically see the highest revenue due to their widespread use in both residential and commercial constructions, where smaller conduit sizes are sufficient for the majority of electrical wiring needs. These sizes are commonly used due to their flexibility, ease of installation, and cost-effectiveness in standard electrical systems. Conversely, the segment witnessing the highest CAGR is the 5 to 6 inch range, driven by increasing demand in industrial and large commercial projects where higher capacity conduits are required to manage larger bundles of wiring for higher voltage applications. This trend is supported by the growth in industrial infrastructure projects, such as manufacturing facilities and data centers, where large-diameter conduits are essential for extensive electrical networks and enhanced safety measures.

Market Segmentation by Classification

In the classification of non-metal electrical conduits, the segments include Polyvinyl Chloride (PVC), Reinforced Thermosetting Resin (RTRC/FRE), Rigid Non-Metallic (RNC), and Electrical Non-Metallic Tubing (ENT). The PVC segment commands the highest revenue in the market, attributed to its cost-effectiveness, corrosion resistance, and easy handling and installation features, making it highly preferable for a wide range of applications from residential buildings to industrial facilities. PVC's versatility and lower cost also make it a staple in both developed and developing markets. On the other hand, the segment expected to exhibit the highest CAGR is the RTRC/FRE conduits. These conduits are favored in more demanding environments that require materials with higher strength, durability, and resistance to harsh chemical and physical conditions. The growing industrial and energy sectors, which often involve exposure to extreme conditions, are increasingly adopting RTRC/FRE conduits, pushing the demand and technological development in this segment.

Geographic Trends

The non-metal electrical conduit market exhibits varied growth dynamics across different regions, driven by factors such as construction growth, infrastructure investment, and regulatory frameworks. Asia Pacific emerges as the region with the highest revenue contribution, primarily due to rapid urbanization, industrialization, and the extensive infrastructural developments occurring in countries like China and India. These markets have consistently demanded high volumes of non-metal conduits for residential, commercial, and industrial applications. Moreover, the region is also anticipated to exhibit the highest CAGR from 2026 to 2034, propelled by ongoing investments in building and construction, energy, and telecommunications sectors, which require extensive and advanced electrical infrastructure. In contrast, developed regions such as North America and Europe continue to generate significant revenue, supported by stringent safety regulations and a steady pace of technological upgrades in electrical systems that favor advanced conduit solutions.

Competitive Trends and Key Strategies Among Leading Players

The competitive landscape in the non-metal electrical conduit market is marked by the presence of major players such as Electri-Flex, Guangdong Ctube Industry, Anamet Electrical, Astral, Atkore, ABB, Cantex, Champion Fiberglass, Schneider Electric, Wienerberger, HellermannTyton, Hubbell, and Legrand. These companies collectively form a dynamic market environment through competitive strategies that include product innovation, mergers and acquisitions, and global expansion. In 2025, these players reported robust revenues, reflecting their strong market positions and operational efficiency. Moving forward, from 2026 to 2034, these companies are expected to intensify their focus on enhancing product portfolios with more sustainable, durable, and versatile conduit solutions. Strategic alliances and acquisition activities are anticipated to be prevalent as companies strive to enhance their geographic reach and technological capabilities in a bid to meet the growing demands of sophisticated electrical infrastructures. For instance, product innovation that integrates smart technologies for enhanced performance and monitoring capabilities in electrical conduits is expected to be a significant trend among the top players. Furthermore, the focus on entering emerging markets where infrastructure developments are ongoing will also be a key strategy to capture the growing demands of these regions.

Historical & Forecast Period

This study report represents analysis of each segment from 2024 to 2034 considering 2025 as the base year. Compounded Annual Growth Rate (CAGR) for each of the respective segments estimated for the forecast period of 2026 to 2034.

The current report comprises of quantitative market estimations for each micro market for every geographical region and qualitative market analysis such as micro and macro environment analysis, market trends, competitive intelligence, segment analysis, porters five force model, top winning strategies, top investment markets, emerging trends and technological analysis, case studies, strategic conclusions and recommendations and other key market insights.

Research Methodology

The complete research study was conducted in three phases, namely: secondary research, primary research, and expert panel review. key data point that enables the estimation of Non-Metal Electrical Conduit Market By Trade Size (½ to 1, 1 ¼ to 2, 2 ½ to 3, 3 to 4, 5 to 6, Others), By Classification (Polyvinyl Chloride (PVC), Reinforced Thermosetting Resin (RTRC/FRE), Rigid Non-Metallic (RNC), Electrical Non-Metallic Tubing (ENT)), By End Use (Residential, Commercial, Industrial, Utility) - Growth, Share, Opportunities & Competitive Analysis, 2026 - 2034 market are as follows:

Market forecast was performed through proprietary software that analyzes various qualitative and quantitative factors. Growth rate and CAGR were estimated through intensive secondary and primary research. Data triangulation across various data points provides accuracy across various analyzed market segments in the report. Application of both top down and bottom-up approach for validation of market estimation assures logical, methodical and mathematical consistency of the quantitative data.

| ATTRIBUTE | DETAILS |

|---|---|

| Research Period | 2024-2034 |

| Base Year | 2025 |

| Forecast Period | 2026-2034 |

| Historical Year | 2024 |

| Unit | USD Million |

| Segmentation | |

Trade Size

|

|

Classification

|

|

End Use

|

|

|

Region Segment (2024-2034; US$ Million)

|

Key questions answered in this report