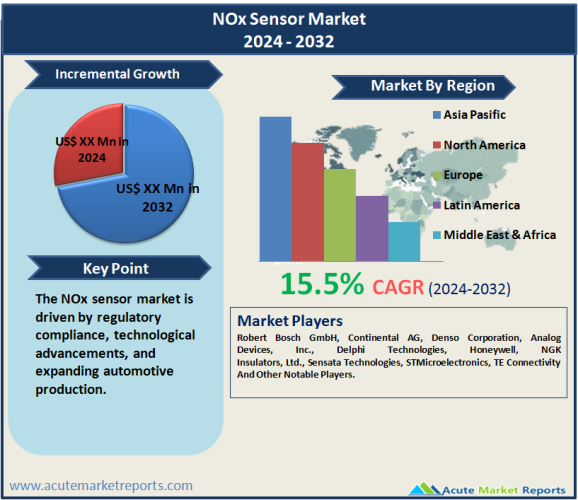

The NOx sensor market is poised for substantial growth driven by increasing regulatory norms globally, particularly aimed at reducing vehicle emissions. TheNOx sensor market is expected to grow at a CAGR of 15.5% during the forecast period of 2026 to 2034, driven by regulatory compliance, technological advancements, and expanding automotive production. While cost constraints present challenges, innovations in sensor technology and strategic initiatives by key market players are expected to propel market expansion across diverse applications and geographic regions. Nitrogen Dioxide sensors led in revenue in 2025, while Nitric Oxide sensors are poised for the highest CAGR from 2026 to 2034. Powertrain applications dominated revenue in 2025, with Vehicle Security Systems projected for the highest CAGR. Geographically, Asia Pacific shows the highest forecasted CAGR, while North America maintains a significant revenue share. Competitive dynamics highlight strategic expansions and technological innovations among key players like Robert Bosch GmbH, Continental AG, and Denso Corporation. Overall, the NOx sensor market is set to expand further, driven by ongoing regulatory pressures and technological advancements in emissions control technologies across the automotive sector.As the automotive industry continues to prioritize emission reduction and compliance with stringent environmental norms, the demand for NOx sensors is anticipated to escalate, shaping the future landscape of emission control technologies in vehicles globally.

Drivers of Market Growth

Regulatory Compliance and Emission Standards

Regulatory mandates worldwide continue to be a primary driver for the NOx sensor market. Governments are enforcing stringent emission norms to curb air pollution, compelling automakers to integrate advanced emission control systems. For instance, the Euro 6 standards in Europe and EPA regulations in the United States have mandated lower emission limits, driving the demand for NOx sensors in both light and heavy-duty vehicles. The adoption of selective catalytic reduction (SCR) systems, where NOx sensors play a crucial role in optimizing efficiency, has further propelled market growth.

Increasing Automotive Production and Sales

The global automotive industry's growth has been instrumental in driving the demand for NOx sensors. As vehicle production and sales volumes escalate, particularly in emerging economies like China and India, the need for emission control technologies, including NOx sensors, has surged. Automakers are increasingly focusing on developing vehicles that comply with stringent emission norms while offering enhanced performance and fuel efficiency, thereby bolstering the market for NOx sensors.

Advancements in Sensor Technology

Technological advancements in NOx sensors have significantly enhanced their performance and reliability, further fueling market expansion. Innovations in sensor materials, such as ceramic-based sensors offering improved durability and accuracy, have gained prominence. Additionally, the integration of IoT and AI technologies in automotive systems has enabled real-time monitoring and adjustment of emission levels, driving the adoption of sophisticated NOx sensing solutions in next-generation vehicles.

Restraint

Cost Constraints and Affordability

Despite the growing demand, cost constraints pose a significant challenge to market growth. The initial high costs associated with NOx sensor procurement and installation, especially in commercial vehicles and heavy-duty applications, remain a deterrent to widespread adoption. Moreover, the maintenance and calibration expenses of NOx sensors add to the overall ownership costs for vehicle owners and fleet operators. Addressing these cost barriers through economies of scale and technological innovations will be crucial for accelerating market penetration across diverse automotive segments.

Market Segmentation: Type

In 2025, Nitrogen Dioxide sensors commanded the highest revenue in the NOx sensor market, driven by their extensive application in diesel vehicles and industrial emissions monitoring systems. However, Nitric Oxide sensors exhibited the highest Compound Annual Growth Rate (CAGR) during the forecast period from 2026 to 2034, propelled by increasing adoption in gasoline-powered vehicles and stringent emission regulations governing NOx emissions.

Market Segmentation: Application

Among various applications, Powertrain systems generated the highest revenue in 2025 for NOx sensors, owing to their critical role in optimizing engine performance and emissions control. Conversely, Vehicle Security Systems demonstrated the highest CAGR during the forecast period of 2026 to 2034, driven by the integration of NOx sensors in automotive security technologies for vehicle tracking and anti-theft systems, enhancing overall vehicle safety and compliance with regulatory standards.

Geographic Segmentation

The NOx sensor market exhibits dynamic geographic trends, with Asia Pacific projected to register the highest CAGR during the forecast period from 2026 to 2034. This growth is primarily attributed to the rapid expansion of automotive production facilities in countries like China and India, coupled with stringent emission regulations aimed at curbing air pollution. North America, particularly the United States, is expected to maintain a significant revenue share due to robust investments in automotive R&D and the adoption of advanced emission control technologies.

Competitive Trends: Top Players and Key Strategies

The competitive landscape of the NOx sensor market in 2025 was characterized by intense rivalry among key players such as Robert Bosch GmbH, Continental AG, Denso Corporation, Analog Devices, Inc., Delphi Technologies, Honeywell, NGK Insulators, Ltd., Sensata Technologies, STMicroelectronics, and TE Connectivity. These companies focused on expanding their product portfolios through strategic collaborations and acquisitions, aimed at enhancing technological capabilities and geographical presence. During the forecast period from 2026 to 2034, market leaders are expected to prioritize R&D investments to innovate next-generation NOx sensing technologies and strengthen their market position amidst evolving regulatory landscapes and competitive pressures.

Historical & Forecast Period

This study report represents analysis of each segment from 2024 to 2034 considering 2025 as the base year. Compounded Annual Growth Rate (CAGR) for each of the respective segments estimated for the forecast period of 2026 to 2034.

The current report comprises of quantitative market estimations for each micro market for every geographical region and qualitative market analysis such as micro and macro environment analysis, market trends, competitive intelligence, segment analysis, porters five force model, top winning strategies, top investment markets, emerging trends and technological analysis, case studies, strategic conclusions and recommendations and other key market insights.

Research Methodology

The complete research study was conducted in three phases, namely: secondary research, primary research, and expert panel review. key data point that enables the estimation of NOx Sensor Market By Type (Nitric Oxide, Nitrogen Dioxide), By Application (Powertrain, Body Electronics, Vehicle Security System, Others) - Growth, Share, Opportunities & Competitive Analysis, 2026 - 2034 market are as follows:

Market forecast was performed through proprietary software that analyzes various qualitative and quantitative factors. Growth rate and CAGR were estimated through intensive secondary and primary research. Data triangulation across various data points provides accuracy across various analyzed market segments in the report. Application of both top down and bottom-up approach for validation of market estimation assures logical, methodical and mathematical consistency of the quantitative data.

| ATTRIBUTE | DETAILS |

|---|---|

| Research Period | 2024-2034 |

| Base Year | 2025 |

| Forecast Period | 2026-2034 |

| Historical Year | 2024 |

| Unit | USD Million |

| Segmentation | |

Type

|

|

Application

|

|

|

Region Segment (2024-2034; US$ Million)

|

Key questions answered in this report