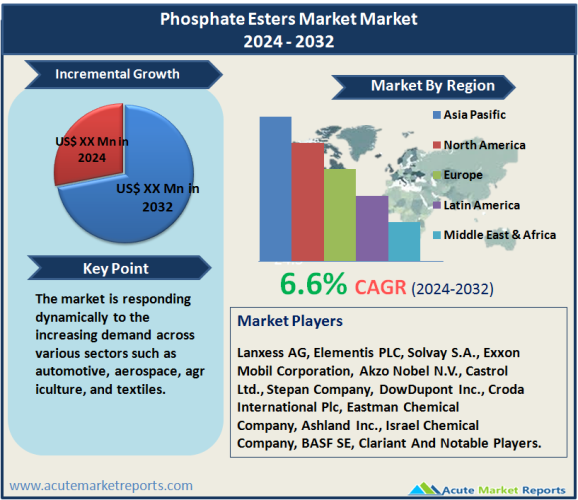

The phosphate esters market is expected to grow at a CAGR of 6.6% during the forecast period of 2026 to 2034. Phosphate esters are organophosphorus compounds widely used as lubricants, surfactants, and fire retardants in various industrial applications. They play a crucial role in enhancing the performance and safety of products across sectors such as automotive, aerospace, agriculture, and textiles. The demand for phosphate esters has been growing due to their superior properties including thermal stability, anti-wear characteristics, and fire resistance. This market is poised for growth, driven by increasing industrial activities and advancements in chemical manufacturing processes.

Drivers

Growing Demand in the Aerospace and Automotive Industries

The aerospace and automotive industries are significant consumers of phosphate esters, utilizing them primarily as hydraulic fluids and lubricants. These industries value phosphate esters for their high thermal stability and fire resistance, essential for ensuring safety and efficiency in high-temperature environments. As global automotive production increases and the aerospace sector continues to recover and expand post-pandemic, the demand for phosphate esters is expected to surge. This trend is supported by the rising investments in vehicle and aircraft modernization, where newer, more environmentally friendly, and safer materials are preferred. Innovations in hydraulic fluids that reduce environmental impact and enhance safety features are particularly driving the market forward.

Stringent Environmental and Safety Regulations

Environmental and safety regulations are becoming stricter across the globe, compelling industries to adopt non-toxic and less flammable materials. Phosphate esters are increasingly favored over other chemicals due to their lower toxicity and superior fire-resistant properties. Regulations such as the EU’s REACH and the U.S. EPA’s guidelines encourage the use of phosphate esters in various applications, including plasticizers in PVC manufacturing, flame retardants in textiles, and lubricants in machinery. These regulatory frameworks not only ensure safer working environments but also promote the use of phosphate esters in consumer products, boosting their market demand.

Advancements in Phosphate Ester Production Technologies

Technological advancements in the production of phosphate esters are allowing manufacturers to enhance the efficiency and environmental compatibility of their products. Modern synthesis processes have improved the yield and quality of phosphate esters, making them more effective and competitive in the market. Innovations in biodegradable and renewable raw material sources for phosphate ester production are particularly noteworthy. These advancements are reducing the ecological footprint of phosphate esters and aligning them with the global shift towards sustainable industrial practices. As these technologies continue to evolve, they are expected to drive the adoption of phosphate esters across a broader range of applications.

Restraint

High Production Cost and Availability of Raw Materials

Despite their advantages, the production of phosphate esters involves high costs related to raw materials and processing. The market for phosphate esters is often constrained by the fluctuating prices and availability of essential raw materials such as phosphorus and alcohol, which are integral in the synthesis of these chemicals. The cost-intensive nature of producing high-quality phosphate esters can limit their use, especially in developing regions where cheaper alternatives are still prevalent. Additionally, the complexity of the synthesis process, which requires significant energy and sophisticated equipment, adds to the overall production costs, making it challenging for manufacturers to scale their operations without impacting product pricing. This factor remains a significant restraint on the market, affecting its growth potential, particularly in cost-sensitive applications.

Market Segmentation by Type

In the phosphate esters market, types such as Triaryl, Trialkyl, Alkyl Aryl, and others each serve distinct roles across various industrial applications due to their unique properties. Triaryl phosphate esters are extensively used and generate the highest revenue within the market due to their excellent fire-retardant properties and stability, making them ideal for high-temperature applications in aerospace and automotive industries. On the other hand, Trialkyl phosphate esters are projected to experience the highest Compound Annual Growth Rate (CAGR). This growth is attributed to their increasing use as lubricants and hydraulic fluids, driven by their superior lubrication properties and biodegradability, which meet the growing environmental regulations and sustainability trends in industrial practices. Alkyl Aryl phosphate esters, with their combination of aryl and alkyl groups, offer balanced properties and are versatile in applications such as surfactants and fire retardants. The segment categorized as 'Others' includes various specialized phosphate esters that are tailored for niche applications, continually evolving with industrial innovation and technological advancements.

Market Segmentation by Application

The application-based segmentation of the phosphate esters market reveals a wide array of uses, each contributing to the market dynamics differently. Lubricants currently generate the highest revenue in the phosphate esters market, extensively used in automotive, industrial, and aerospace sectors due to their excellent thermal stability and fire resistance. These properties are critical in high-performance applications where safety and equipment reliability are paramount. Conversely, the surfactants application is expected to register the highest CAGR. The demand for phosphate ester-based surfactants is rising, particularly in household and industrial cleaning products, as they offer superior cleaning efficiency and are less toxic compared to traditional surfactants. This growth is further supported by the shifting consumer preferences towards safer and environmentally friendly cleaning products. Other applications such as fire retardants, agrochemicals, plasticizers, and hydraulic fluids also significantly contribute to the market, with each finding specialized roles driven by the unique properties of phosphate esters that enhance product performance and safety standards in various environmental conditions.

Geographic Trends

The phosphate esters market exhibits distinct geographic trends influenced by industrial development, regulatory environments, and technological advancements across regions. Asia Pacific is identified as the region with the highest Compound Annual Growth Rate (CAGR), expected from 2026 to 2034. This rapid growth is driven by increasing industrial activities in countries like China, India, and South Korea, where there is rising demand for phosphate esters in applications such as lubricants, fire retardants, and surfactants. The region benefits from expanding manufacturing sectors, significant investments in infrastructure, and favorable government policies supporting chemical industry growth. In terms of revenue, North America holds the largest share, attributed to its advanced industrial base and stringent regulatory standards requiring high-performance and environmentally safe chemicals. North American industries such as automotive, aerospace, and agriculture heavily rely on the unique properties of phosphate esters, supporting their dominant revenue position. Both regions demonstrate a strong integration of phosphate esters in various industrial processes, with Asia Pacific's growth potential particularly underscored by its expanding economic activities and increasing environmental awareness.

Competitive Trends and Key Players

The competitive landscape of the phosphate esters market is shaped by the strategic initiatives of key players like Lanxess AG, Elementis PLC, Solvay S.A., Exxon Mobil Corporation, Akzo Nobel N.V., Castrol Ltd., Stepan Company, DowDupont Inc., Croda International Plc, Eastman Chemical Company, Ashland Inc., Israel Chemical Company, BASF SE, and Clariant. In 2025, these companies reported robust revenues driven by their innovative product offerings and strategic global expansions. Looking ahead from 2026 to 2034, these players are expected to focus on advancing their technological capabilities and enhancing their product portfolios to meet the stringent environmental regulations and the evolving needs of various end-user industries. Strategies such as mergers and acquisitions, capacity expansions, and new product developments are prevalent among these firms to sustain their competitiveness and capture larger market shares. For instance, companies like BASF SE and Solvay S.A. are heavily investing in research and development to produce more environmentally friendly and efficient phosphate esters. Furthermore, the shift towards sustainable practices is prompting companies like Croda International Plc and Eastman Chemical Company to innovate in biodegradable and renewable raw material-based phosphate esters, aligning with global sustainability trends. The strategic emphasis across the board is on enhancing product efficiency, environmental compatibility, and operational flexibility, positioning these companies to leverage growth opportunities in both established and emerging markets during the forecast period.

Historical & Forecast Period

This study report represents analysis of each segment from 2024 to 2034 considering 2025 as the base year. Compounded Annual Growth Rate (CAGR) for each of the respective segments estimated for the forecast period of 2026 to 2034.

The current report comprises of quantitative market estimations for each micro market for every geographical region and qualitative market analysis such as micro and macro environment analysis, market trends, competitive intelligence, segment analysis, porters five force model, top winning strategies, top investment markets, emerging trends and technological analysis, case studies, strategic conclusions and recommendations and other key market insights.

Research Methodology

The complete research study was conducted in three phases, namely: secondary research, primary research, and expert panel review. key data point that enables the estimation of Phosphate Esters Market By Type (Triaryl, Trialkyl, Alkyl Aryl, Others), By Application (Surfactants, Fire retardants, Lubricants, Agrochemicals, Plasticizers, Hydraulic fluids, Others) - Growth, Share, Opportunities & Competitive Analysis, 2026 - 2034 market are as follows:

Market forecast was performed through proprietary software that analyzes various qualitative and quantitative factors. Growth rate and CAGR were estimated through intensive secondary and primary research. Data triangulation across various data points provides accuracy across various analyzed market segments in the report. Application of both top down and bottom-up approach for validation of market estimation assures logical, methodical and mathematical consistency of the quantitative data.

| ATTRIBUTE | DETAILS |

|---|---|

| Research Period | 2024-2034 |

| Base Year | 2025 |

| Forecast Period | 2026-2034 |

| Historical Year | 2024 |

| Unit | USD Million |

| Segmentation | |

Type

|

|

Application

|

|

|

Region Segment (2024-2034; US$ Million)

|

Key questions answered in this report