Power electronics for the renewable energy market are a critical component of the sustainable energy landscape, enabling the efficient conversion and management of renewable energy sources. The power electronics for renewable energy market is expected to grow at a CAGR of 7.5% during the forecast period of 2026 to 2034, driven by the global emphasis on clean energy, technological advancements, government policies, and incentives. While the intermittent nature of renewable energy sources remains a challenge, the industry is actively working on solutions to enhance grid stability and energy reliability. The market segmentation by device type and application provides valuable insights

Growing Global Emphasis on Clean Energy

One of the primary drivers of the power electronics for the renewable energy market is the increasing global emphasis on clean and sustainable energy sources. Governments, industries, and consumers worldwide are recognizing the need to transition away from fossil fuels to mitigate climate change and reduce environmental impact. Renewable energy sources, such as solar, wind, and hydroelectric power, play a pivotal role in this transition. Power electronics facilitate the efficient conversion and integration of these intermittent energy sources into the grid. The growing investments in renewable energy projects and incentives to adopt clean energy technologies are propelling the demand for power electronics in the sector. According to the International Energy Agency (IEA), global renewable electricity capacity is expected to expand by almost 50% by 2026, highlighting the significant growth potential for power electronics in this sector.

Technological Advancements and Efficiency Gains

Continuous technological advancements in power electronics have driven efficiency gains and cost reductions, making renewable energy more competitive. Innovations in power semiconductor devices, smart grid technology, and energy storage solutions have enhanced the performance of power electronics systems. This, in turn, has improved the overall efficiency of renewable energy generation, transmission, and utilization. Advanced power electronics contribute to reducing energy losses and enhancing grid stability, making renewable energy sources a more reliable and viable option for the energy industry. Research published in the journal "IEEE Transactions on Industrial Electronics" highlights the advancements in power electronics that have significantly improved the efficiency of photovoltaic systems and wind turbines.

Government Policies and Incentives

Government policies and incentives at the national and regional levels have played a crucial role in driving the adoption of power electronics for renewable energy. Subsidies, tax credits, feed-in tariffs, and renewable portfolio standards encourage investments in renewable energy projects and the deployment of power electronics systems. Furthermore, regulations promoting grid integration and clean energy goals have created a conducive environment for the growth of Power Electronics for the Renewable Energy market. The U.S. Investment Tax Credit (ITC) and the Production Tax Credit (PTC) have significantly boosted the installation of renewable energy projects, contributing to the increased demand for power electronics systems.

Restraint for the Power Electronics for Renewable Energy Market

While the Power Electronics for Renewable Energy market holds promising prospects, a significant restraint is the intermittent nature of renewable energy sources. Solar and wind power generation, for instance, are subject to fluctuations in energy production due to weather conditions. Power electronics can mitigate these fluctuations, but the intermittent nature of renewable sources still poses challenges to grid stability and energy supply reliability. The industry needs to invest in robust energy storage solutions and advanced grid management systems to address these challenges effectively. Grid instability and energy supply issues have been observed during periods of low renewable energy generation, which highlights the need for advanced power electronics and energy storage solutions to maintain a stable and reliable energy supply.

Market Segmentation by Device Type (Power Discrete, Power Module, Power IC): Power Module Dominates the Market

The power electronics for the renewable energy market can be segmented by device type into three categories: power discrete, power module, and power IC. In 2025, the "power module" segment generated the highest revenue. Power modules are favored for their compact design and high power density, making them suitable for renewable energy systems. For the period from 2026 to 2034, the "power IC" segment is expected to exhibit the highest CAGR. Integrated circuits (ICs) offer advantages in terms of miniaturization and efficient power management, making them a preferred choice as the market progresses.

Market Segmentation by Application (Power Generation, Power Transmission, Power Distribution, Power Control): Power Generation Dominates the Market

The power electronics for the renewable energy market can be segmented by application into four categories: power generation, power transmission, power distribution, and power control. In 2025, the "power generation" segment witnessed the highest revenue. Efficient power electronics systems are essential for optimizing energy production from renewable sources. For the period from 2026 to 2034, the "power control" segment is expected to experience the highest CAGR. Power control applications, including energy storage and grid management, are increasingly crucial for ensuring the reliable integration of renewable energy into the power grid.

North America Remains the Global Leader

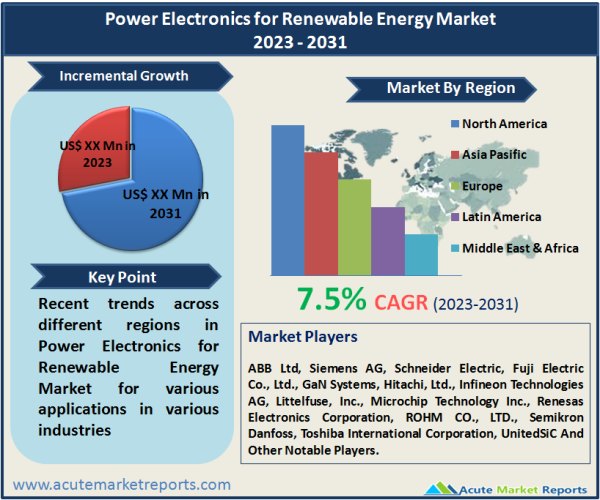

The power electronics for renewable energy market exhibits geographic variations in demand and growth. Geographic trends indicate that regions with abundant renewable energy resources and strong policy support tend to lead in renewable energy adoption and the use of power electronics systems. For instance, regions like Europe and North America have experienced significant growth due to their focus on clean energy and advanced grid infrastructure. When considering the region with the highest CAGR during the forecast period from 2026 to 2034, Asia-Pacific is expected to exhibit the most substantial growth. Asia-Pacific's rapid industrialization and population growth have intensified the demand for renewable energy solutions, including power electronics for grid integration. In terms of revenue percentage, North America is expected to maintain its position as the region with the highest revenue percentage throughout the forecast period. The region's continued investments in renewable energy projects and the adoption of advanced power electronics systems contribute to its prominent share in the Power Electronics for Renewable Energy market.

Competitive Trends, Top Players, and Key Strategies

The power electronics for renewable energy market features several key players, each employing specific strategies to maintain and expand their market presence. The top players in the market include established companies like ABB Ltd, Siemens AG, Schneider Electric, Fuji Electric Co., Ltd., GaN Systems, Hitachi, Ltd., Infineon Technologies AG, Littelfuse, Inc., Microchip Technology Inc., Renesas Electronics Corporation, ROHM CO., LTD., Semikron Danfoss, Toshiba International Corporation, UnitedSiC, and others. In 2025, ABB Ltd held a significant market share, offering a wide range of power electronics solutions for renewable energy applications. The company's strategy revolved around innovation, enhancing the efficiency of power conversion systems, and expanding its global reach. Siemens AG, another industry leader, excelled in providing power electronics for power transmission and distribution applications in renewable energy. Their strategy emphasized strengthening partnerships with utilities and government bodies to support grid integration projects. Schneider Electric, with a focus on power control and energy management, positioned itself as a key player in the renewable energy market. Their strategy centered on providing comprehensive energy management solutions for the optimization of renewable energy systems. For the forecast period from 2026 to 2034, these companies are expected to continue their strategies, focusing on innovation, customization, sustainability, and expanding their global footprint. They will explore new markets and technologies to maintain their competitive edge in the evolving power electronics for the renewable energy market.

Historical & Forecast Period

This study report represents analysis of each segment from 2024 to 2034 considering 2025 as the base year. Compounded Annual Growth Rate (CAGR) for each of the respective segments estimated for the forecast period of 2026 to 2034.

The current report comprises of quantitative market estimations for each micro market for every geographical region and qualitative market analysis such as micro and macro environment analysis, market trends, competitive intelligence, segment analysis, porters five force model, top winning strategies, top investment markets, emerging trends and technological analysis, case studies, strategic conclusions and recommendations and other key market insights.

Research Methodology

The complete research study was conducted in three phases, namely: secondary research, primary research, and expert panel review. key data point that enables the estimation of Power Electronics for Renewable Energy Market By Device Type (Power Discrete, Power Module, Power IC), By Component (Converters, Inverters, Transformers, Voltage Control Devices, Others), By Application (Power Generation, Power Transmission, Power Distribution, Power Control), By Power Range (Up to 1 MW, 1 MW to 3 MW, 3 MW to 5 MW, Above 5 MW), By End-Use (Solar PV, Wind, Hydro, Fuel Cell, Others) - Growth, Share, Opportunities & Competitive Analysis, 2026 - 2034 market are as follows:

Market forecast was performed through proprietary software that analyzes various qualitative and quantitative factors. Growth rate and CAGR were estimated through intensive secondary and primary research. Data triangulation across various data points provides accuracy across various analyzed market segments in the report. Application of both top down and bottom-up approach for validation of market estimation assures logical, methodical and mathematical consistency of the quantitative data.

| ATTRIBUTE | DETAILS |

|---|---|

| Research Period | 2024-2034 |

| Base Year | 2025 |

| Forecast Period | 2026-2034 |

| Historical Year | 2024 |

| Unit | USD Million |

| Segmentation | |

Device Type

|

|

Component

|

|

Application

|

|

Power Range

|

|

End-Use

|

|

|

Region Segment (2024-2034; US$ Million)

|

Key questions answered in this report