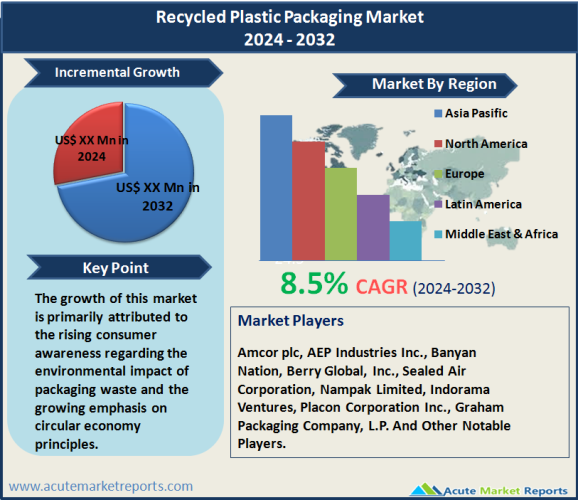

The recycled plastic packaging market is expected to grow at a CAGR of 8.5% during the forecast period of 2026 to 2034. Recycled plastic packaging market has garnered significant attention due to increasing environmental concerns and stringent regulations regarding waste management. This market involves the process of collecting and processing post-consumer and post-industrial plastic waste into reusable packaging materials. The shift towards sustainable practices is driving the adoption of recycled plastic packaging across various industries including food & beverages, healthcare, personal care, and others. The growth of this market is primarily attributed to the rising consumer awareness regarding the environmental impact of packaging waste and the growing emphasis on circular economy principles.

Driver: Government Initiatives and Regulations

Governments worldwide are implementing policies and regulations that mandate or encourage the use of recycled materials in packaging. For instance, the European Union's strategy for plastics in a circular economy proposes that by 2034, all plastic packaging placed on the EU market should be either reusable or recyclable. Such regulatory frameworks compel manufacturers to incorporate recycled plastics in their packaging solutions, thereby boosting market growth. Additionally, incentives and subsidies for recycling activities can lower the overall costs associated with recycled plastic packaging, making it more competitive against conventional plastic packaging. These regulations not only promote environmental sustainability but also support the economic viability of recycling infrastructure, further propelling the market forward.

Driver: Consumer Awareness and Demand for Sustainable Products

The surge in consumer awareness regarding the environmental hazards associated with single-use plastics has significantly influenced purchasing behaviors. More consumers are now demanding sustainable and eco-friendly packaging options, driving companies to incorporate recycled plastics in their packaging to enhance brand image and meet consumer expectations. The rise of social media and digital platforms has also played a pivotal role in educating and influencing consumer choices, leading to a higher adoption of recycled plastic packaging. Companies leveraging recycled content are often viewed favorably by environmentally conscious consumers, which can translate into increased customer loyalty and market share.

Driver: Technological Advancements in Recycling Processes

Technological innovations have greatly improved the efficiency and effectiveness of plastic recycling processes, making recycled plastic packaging more viable and appealing to manufacturers. Advanced sorting and processing technologies have enhanced the quality of recycled plastics, addressing concerns regarding the aesthetic and functional properties of recycled materials. These technological advancements ensure that recycled plastics meet the stringent quality standards required for packaging applications, thus broadening their applicability across various sectors. Furthermore, innovations in biodegradable plastics and compostable materials are creating new opportunities within the recycled plastic packaging market, as they complement traditional recycling methods and help reduce the reliance on virgin plastics.

Restraint: Contamination and Quality Issues in Recycled Plastics

One major restraint in the recycled plastic packaging market is the issue of contamination and the subsequent quality of the recycled materials. Recycled plastics often contain residues from previous uses, such as food, chemicals, or other materials, which can compromise the integrity and safety of the recycled packaging. This is particularly concerning in industries such as food and beverages and healthcare, where packaging safety is crucial. The variability in the quality of recycled plastics can lead to inconsistent product properties, affecting the performance and appearance of the packaging. These challenges necessitate rigorous sorting and processing techniques, which can increase the costs and complexity of recycling, thus hindering market growth. Despite these challenges, ongoing research and development are focused on improving the purification processes to enhance the quality and expand the use of recycled plastics in packaging applications.

Market Segmentation by Plastic Type

In the recycled plastic packaging market, segmentation by plastic type reveals a diverse landscape of materials, each with specific properties and recycling technologies. Polyethylene Terephthalate (PET) stands out due to its extensive use in beverage bottles and food containers, driving its demand as the segment with the highest revenue. PET's properties, such as clarity, strength, and barrier to moisture, make it highly recyclable and a preferred choice for consumer goods. This segment not only leads in terms of market share but is also projected to exhibit the highest Compound Annual Growth Rate (CAGR). The emphasis on PET recycling is spurred by stringent regulations and consumer preference for sustainable packaging solutions. High-Density Polyethylene (HDPE) and Polypropylene (PP) follow closely, known for their sturdiness and versatility, respectively. HDPE is commonly used in sturdier containers and milk jugs, while PP's resistance to heat makes it ideal for applications requiring sterilization. Low-Density Polyethylene (LDPE), used in film applications such as plastic wraps and bags, contributes significantly to market dynamics due to its widespread use in retail. Polystyrene (PS), although less commonly recycled due to its complex chemical structure, finds niche applications in the packaging of electronics and appliances. The 'Others' category, which includes materials like Polyvinyl Chloride (PVC) and ABS, highlights the potential for growth in less common types of recycled plastics, as new technologies and improved recycling processes emerge.

Market Segmentation by Source

Segmentation of the recycled plastic packaging market by source highlights various primary sources of recycled plastics, each contributing differently to market growth and revenue generation. Plastic bottles, encompassing materials like PET and HDPE, dominate this category, providing the highest revenue and the fastest growth rate. The ubiquity of plastic bottles in consumer markets, coupled with established collection and recycling systems, makes this segment pivotal. The focus on plastic bottles is driven by their significant volume in waste streams and high recyclability, which supports the production of high-quality recycled materials suitable for various packaging applications. Plastic films, including materials such as LDPE, also play a crucial role due to their extensive use in shopping bags, agricultural films, and packaging wraps. Although recycling rates for films are lower compared to bottles, innovations in collection and sorting technologies are enhancing recycling efficiencies, indicating potential for high growth. Polymer foam and fibers represent smaller segments but are gaining traction with advancements in recycling technologies that address challenges related to their structure and composition. The 'Others' category encapsulates additional sources like rigid containers and engineered plastics, expanding the scope of recyclable materials entering the packaging sector. Each source category contributes uniquely to the dynamics of the recycled plastic packaging market, influenced by factors such as material properties, application areas, and technological developments in recycling processes.

Geographic Segmentation and Trends

In the recycled plastic packaging market, geographic segmentation reveals varying trends and growth dynamics across different regions. The Asia-Pacific region emerges as the standout leader both in terms of highest revenue generation and highest Compound Annual Growth Rate (CAGR) forecasted from 2026 to 2034. This dominance is attributed to increasing industrialization, expanding consumer markets, and heightened environmental regulations in populous countries such as China and India. Furthermore, the region benefits from a robust manufacturing base and government incentives promoting sustainable packaging solutions, driving both demand and technological advancements in recycled plastics. Europe also shows significant market activity, supported by stringent EU directives aimed at reducing plastic waste and enhancing recycling rates. North America, with its well-established recycling infrastructure and growing consumer preference for sustainable products, contributes notably to the global market dynamics. In contrast, Latin America and the Middle East & Africa, though smaller in revenue share, are expected to experience gradual growth due to rising awareness about plastic waste and its environmental impacts.

Competitive Trends and Key Strategies

The recycled plastic packaging market is characterized by intense competition among key players such as Amcor plc, AEP Industries Inc., Banyan Nation, Berry Global, Inc., Sealed Air Corporation, Nampak Limited, Indorama Ventures, Placon Corporation Inc., and Graham Packaging Company, L.P. These companies are strategically positioned across various geographic regions, contributing to their competitive edge in the market. In 2025, these firms focused heavily on expanding their recycling capacities and innovating eco-friendly packaging solutions to meet both regulatory requirements and consumer preferences. For instance, Amcor plc and Berry Global, Inc. have been at the forefront in adopting advanced recycling technologies and developing sustainable materials that offer both functionality and environmental benefits. Companies like Sealed Air Corporation and Indorama Ventures have emphasized partnerships and acquisitions to broaden their market reach and enhance their product portfolios with recycled content. Nampak Limited and Placon Corporation Inc., on the other hand, have concentrated on optimizing their operational efficiencies and expanding into new markets to capitalize on the growing demand for recycled packaging solutions. Looking ahead from 2026 to 2034, these companies are expected to intensify their efforts in research and development, aiming to overcome existing material limitations and to cater to the stringent quality requirements of industries such as food and healthcare. The strategic focus for these players will likely revolve around enhancing the quality of recycled plastics while reducing production costs to remain competitive in a market that is increasingly driven by both regulatory pressures and consumer demands for sustainability.

Historical & Forecast Period

This study report represents analysis of each segment from 2024 to 2034 considering 2025 as the base year. Compounded Annual Growth Rate (CAGR) for each of the respective segments estimated for the forecast period of 2026 to 2034.

The current report comprises of quantitative market estimations for each micro market for every geographical region and qualitative market analysis such as micro and macro environment analysis, market trends, competitive intelligence, segment analysis, porters five force model, top winning strategies, top investment markets, emerging trends and technological analysis, case studies, strategic conclusions and recommendations and other key market insights.

Research Methodology

The complete research study was conducted in three phases, namely: secondary research, primary research, and expert panel review. key data point that enables the estimation of Recycled Plastic Packaging Market By Plastic Type (PET (Polyethylene Terephthalate), HDPE (High-Density Polyethylene), LDPE (Low-Density Polyethylene), PP (Polypropylene), PS (Polystyrene), Others), By Source (Plastic Bottles, Plastic Films, Polymer Foam, Fibers, Others), By Recycling Process (Mechanical Recycling, Chemical Recycling), By End-use (Food and Beverage, Consumer Goods, Healthcare, Industrial, Others) - Growth, Share, Opportunities & Competitive Analysis, 2026 - 2034 market are as follows:

Market forecast was performed through proprietary software that analyzes various qualitative and quantitative factors. Growth rate and CAGR were estimated through intensive secondary and primary research. Data triangulation across various data points provides accuracy across various analyzed market segments in the report. Application of both top down and bottom-up approach for validation of market estimation assures logical, methodical and mathematical consistency of the quantitative data.

| ATTRIBUTE | DETAILS |

|---|---|

| Research Period | 2024-2034 |

| Base Year | 2025 |

| Forecast Period | 2026-2034 |

| Historical Year | 2024 |

| Unit | USD Million |

| Segmentation | |

Plastic Type

|

|

Source

|

|

Recycling Process

|

|

End-use

|

|

|

Region Segment (2024-2034; US$ Million)

|

Key questions answered in this report