The sun care market includes products designed to protect the skin from harmful ultraviolet (UV) radiation, prevent sunburn, and reduce the risk of skin cancer and premature skin aging. This market encompasses a wide range of products such as sunscreens, after-sun lotions, self-tanning products, and protective lip balms. These products vary in SPF ratings, formats (creams, sprays, sticks), and additional skin care benefits like moisturization and anti-aging properties. The sun care market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.7%. This robust growth rate reflects the increasing demand for sun protection products amid rising health consciousness and lifestyle shifts that involve greater time spent outdoors. The market is also benefiting from technological advancements in formulations that offer broader spectrum UV protection and longer-lasting effects. Moreover, the rise in travel and tourism activities, particularly in tropical and high-altitude regions where UV exposure is intense, continues to drive the demand for sun care products. With ongoing educational campaigns about sun safety and the aesthetic benefits of sun care products, the market is expected to maintain a strong growth trajectory through the forecast period.

Increased Awareness of Skin Health

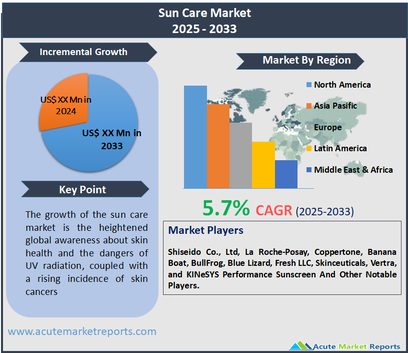

A significant driver for the growth of the sun care market is the heightened global awareness about skin health and the dangers of UV radiation, coupled with a rising incidence of skin cancers. Public health campaigns and educational initiatives have effectively disseminated information about the risks associated with prolonged sun exposure and the importance of regular sunscreen use. This public health messaging has been bolstered by support from healthcare providers and non-governmental organizations promoting skin cancer prevention. As a result, consumers are increasingly seeking products that offer effective protection against harmful UV rays, thereby driving the demand for a wide range of sun care products. This trend is evident in both developed and emerging markets, where a growing middle class is becoming more health-conscious and willing to invest in premium sun care products.

Inclusion of Sun Care in Daily Skincare Routines

An emerging opportunity within the sun care market is the integration of sun protection into daily skincare and makeup routines. Consumers are increasingly looking for multifunctional products that combine UV protection with other skincare benefits such as moisturization, anti-aging properties, and foundation coverage. The demand for such products presents a lucrative avenue for growth, especially as part of the broader trend towards holistic health and wellness. This consumer preference drives innovation among manufacturers to develop and market sun care products as essential everyday skincare, rather than only for use at the beach or during outdoor activities. This shift is expanding the user base and usage frequency, which could significantly boost market growth.

Regulatory and Safety Challenges

The primary restraint facing the sun care market stems from stringent regulatory challenges related to the safety and efficacy of sunscreen ingredients. In many countries, sunscreens are regulated as drugs rather than cosmetics, which subjects them to rigorous testing and approval processes that can be lengthy and costly. Concerns over the safety of certain chemical UV filters have led to stricter regulations and even bans in some regions, which complicate formulation and marketing. These challenges are compounded by increasing consumer scrutiny regarding ingredient safety, spurred by advocacy groups and informed consumers who demand transparency and prefer products with natural and fewer harmful substances.

Innovation and Competition in Sun Care Formulations

A major challenge in the sun care market is the need for continuous innovation amid intense competition and changing consumer preferences. Developing new formulations that not only effectively protect against a broader spectrum of UV radiation but also meet the cosmetic and skin health expectations of savvy consumers can be costly and resource-intensive. Additionally, with the market becoming more saturated, differentiating products in a way that appeals to diverse consumer segments such as those with specific skin types or environmental concerns requires substantial investment in research and development. Companies must navigate these complexities while also addressing calls for sustainability, such as reducing the environmental impact of sunscreen on marine ecosystems, which has become a significant concern for environmentally conscious consumers.

Market Segmentation by Form

In the sun care market, the product forms include creams, gels, lotions, liquids, sprays, lip balms, wipes, sticks, and other forms such as powders and colored sunscreens. Lotions hold the highest revenue within the market due to their widespread use and preference for their ease of application, effective coverage, and suitability for both face and body application. Lotions are favored for their hydrating properties, making them ideal for consumers with dry skin and for those seeking a balance between sun protection and skin care. However, sprays are projected to experience the highest Compound Annual Growth Rate (CAGR) from 2026 to 2034. The convenience and ease of use associated with sprays, particularly for reaching difficult areas and for quick application, make them increasingly popular among consumers leading active lifestyles. This form is also appealing for its non-greasy texture and uniform application, driving its growing adoption in the market.

Market Segmentation by SPF

The sun care market is segmented by SPF ratings, including SPF 6-14, SPF 15-29, SPF 30-50, and SPF 50+. SPF 30-50 dominates in terms of revenue due to its widespread recommendation by dermatologists for effective protection against the sun’s harmful UV rays. Products within this SPF range offer a balance between protection and usability, suitable for daily use without the heaviness associated with higher SPF products. On the other hand, SPF 50+ is expected to register the highest CAGR over the forecast period. This growth is driven by increasing consumer awareness about skin health and the rising prevalence of skin cancer, prompting people to opt for higher SPF products that provide more comprehensive protection against intense sun exposure, particularly in regions with high UV indices.

Geographic Segmentation

In 2025, the sun care market was dominated by North America in terms of revenue, driven by high consumer awareness about skin health, the prevalence of outdoor lifestyles, and stringent regulations regarding sun protection. The region's market leadership is supported by well-established healthcare guidelines recommending regular use of sunscreens to prevent skin cancer and premature aging. However, the Asia-Pacific region is expected to exhibit the highest CAGR from 2026 to 2034. This anticipated growth stems from increasing disposable incomes, expanding urban populations, and growing awareness of sun damage, particularly in countries like China, India, and Australia, where sunny climates contribute to a higher incidence of UV-related skin issues. The expanding beauty and personal care industry in these areas further complements the surge in demand for sun care products.

Competitive Trends and Top Players

The competitive landscape of the sun care market in 2025 included key players such as Shiseido Co., Ltd, La Roche-Posay, Coppertone, Banana Boat, BullFrog, Blue Lizard, Fresh LLC, Skinceuticals, Vertra, and KINeSYS Performance Sunscreen. These companies focused on expanding their product portfolios with innovative formulations that offer broad-spectrum UV protection, superior water resistance, and added skin care benefits like anti-aging and moisturizing properties. A common strategy among these players was leveraging advanced R&D capabilities to develop sunscreens that meet specific consumer needs, such as mineral-based formulas for sensitive skin and lightweight, non-greasy products for daily use. For the forecast period of 2026 to 2034, these companies are expected to intensify their efforts in sustainability, with a shift towards eco-friendly packaging and natural ingredient formulations to minimize environmental impact and cater to the green consumer trend. Additionally, strategic global expansions, particularly into high-growth markets in the Asia-Pacific region, will likely be pursued to capitalize on emerging consumer segments and reinforce global presence. These strategies will be crucial for maintaining competitiveness and market share in an increasingly aware and health-conscious global market.

Historical & Forecast Period

This study report represents analysis of each segment from 2024 to 2034 considering 2025 as the base year. Compounded Annual Growth Rate (CAGR) for each of the respective segments estimated for the forecast period of 2026 to 2034.

The current report comprises of quantitative market estimations for each micro market for every geographical region and qualitative market analysis such as micro and macro environment analysis, market trends, competitive intelligence, segment analysis, porters five force model, top winning strategies, top investment markets, emerging trends and technological analysis, case studies, strategic conclusions and recommendations and other key market insights.

Research Methodology

The complete research study was conducted in three phases, namely: secondary research, primary research, and expert panel review. key data point that enables the estimation of Sun Care Market By Form, By SPF, By Sports, By Price Category, By Region - Global Market Analysis & Forecast, 2025 to 2033 market are as follows:

Market forecast was performed through proprietary software that analyzes various qualitative and quantitative factors. Growth rate and CAGR were estimated through intensive secondary and primary research. Data triangulation across various data points provides accuracy across various analyzed market segments in the report. Application of both top down and bottom-up approach for validation of market estimation assures logical, methodical and mathematical consistency of the quantitative data.

| ATTRIBUTE | DETAILS |

|---|---|

| Research Period | 2024-2034 |

| Base Year | 2025 |

| Forecast Period | 2026-2034 |

| Historical Year | 2024 |

| Unit | USD Million |

| Segmentation | |

Form

|

|

SPF

|

|

Sports Type

|

|

Price Category

|

|

|

Region Segment (2024-2034; US$ Million)

|

Key questions answered in this report