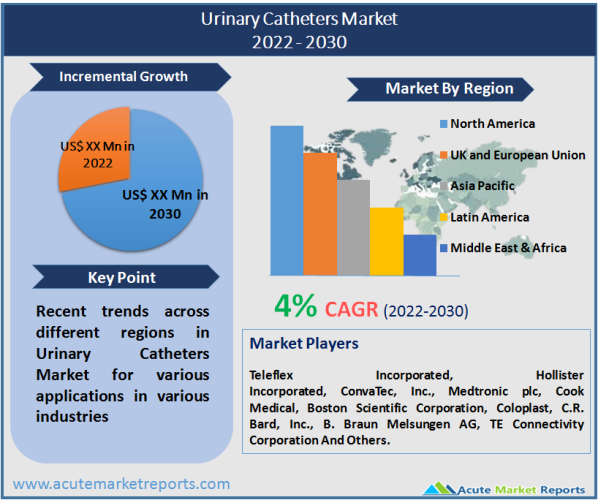

The market for urinary catheters was worth US$ 1.5 billion globally in 2018, and it is anticipated to grow at a CAGR of 4% from 2021 to 2034.Favorable reimbursement policies and growing demand for innovative urinary catheters are two key drivers of rising demand for urinary catheters, which in turn is boosting the market for urinary catheters. Urinary catheter demand is rising due to a rise in medical procedures performed around the world.

Patients with urine incontinence, urinary retention, and other urological problems use urinary catheters. A flexible tube called a urinary catheter, which is typically put into the patient's bladder by a medical expert, is used to drain the bladder and collect urine in a drainage pack.

There are three types of urinary catheters: external (condom) catheters, intermittent (short-term) catheters, and indwelling (Foley) catheters. A flexible tube with lumens on both ends is called an indwelling (Foley) catheter. Through the urethra, this kind of urinary catheter is inserted into the bladder. An adjustable catheter called an intermittent catheter is used to empty the bladder at regular intervals. For elderly male dementia patients, an external or condom urinary catheter is typically used (loss of cerebrum work). The male genital area is covered by a condom-shaped urinary catheter that has a tube leading to a drainage bag where urine is collected.

Due to the rapid advancement in healthcare, rise in the number of elderly people, and enhanced healthcare infrastructure, the market for urinary catheters is anticipated to see attractive growth prospects over the forecast period. The most frequently performed operation in hospitals is bladder catheterization, which drives the demand for urinary catheters. Urinary catheters are frequently required due to the rising incidence of prostate cancer and the increasing number of prostate procedures performed in hospitals.

Growing Adoption of Intermittent Self-Catheters (ISCs)

Patients with urine retention or incontinence issues can be effectively managed with intermittent self-catheters (ISCs). The global market for urinary catheters is driven by improvements in healthcare, an increase in surgical operations, and greater consumer awareness of these devices, which presents lucrative potential for market participants. Urine leakage humiliation and its effects on physical and mental health have prompted an increase in the usage of these devices among the elderly population. Also encouraging people to adopt healthier lifestyles assisted by the use of such devices is the general rise in health consciousness.

Increasing Incidence of Urological Conditions

An infection of the urinary system, comprising the urethra, bladder, ureters, and kidney, is referred to as a urinary tract infection (UTI). The most prevalent urological condition, UTIs, require the use of foley catheters, according to the National Healthcare Safety Network (NHSN). Additionally, the Centers for Disease Control and Prevention (CDC) reports that 15–25% of hospitalised patients get a foley catheter annually. Similarly, between 75,000 and 150,000 people, or 5–10% of nursing home residents, need foley catheters.

Expanding Geriatric Population Base

Due to the relatively high incidence of bladder infections among those 60 and older, the geriatric population has been identified as the main foley catheter user demographic. Among the elderly population, primarily men, diseases such urinary retention, BPH, bladder obstruction, urinary incontinence, and prostate cancer have become more prevalent. In addition to the aforementioned illnesses, elderly women have exponentially higher rates of asymptomatic bacteriuria (ASB) than younger women.

Emerging economies have huge growth prospects

Major market participants have huge growth prospects in emerging economies including China, India, South Korea, Brazil, and Mexico. This is due to factors such as their lax regulatory requirements, improved healthcare facilities, expanding patient populations, and rising healthcare costs.

Compared to wealthy nations, the regulatory regulations in the Asia-Pacific region are more flexible and business-friendly. This has led major companies in the urinary catheters market to concentrate on growing nations, along with the escalating competition in mature areas. For instance, B. Braun launched a subsidiary in Zambia in 2017 and five new medical production facilities in Penang, Malaysia, in April 2018.

Opportunities for growth resulting from the growing adoption of intermittent self-catheters (ISCs)

Patients with urine retention or incontinence issues can be effectively managed with intermittent self-catheters (ISCs). The global market for urinary catheters is driven by improvements in healthcare, an increase in surgical operations, and greater consumer awareness of these devices, which presents lucrative potential for market participants. Urine leakage humiliation and its effects on physical and mental health have prompted an increase in the usage of these devices among the elderly population. Also encouraging people to adopt healthier lifestyles assisted by the use of such devices is the general rise in health consciousness.

Catheterization complications and availability of substitutes are a challenge

To avoid urinary tract infections (UTIs) or catheter-associated UTIs, special precautions must be taken during catheterization (CAUTIs). In order to address temporary incontinence, there are numerous alternative invasive and non-invasive therapy techniques available. Given the drawbacks of catheterization, it is anticipated that the market for urinary catheters will be constrained by their accessibility.

Approvals by Regulatory Bodies in Emerging Nations

The market for urinary catheters has enormous potential for growth in developing nations like Mexico, Brazil, China, India, and Brazil. Future growth potential can be ascribed to a rising number of regulatory body approvals, an expanding patient population, rising healthcare costs, and advancements in the healthcare infrastructure.

The global market for urinary catheters is divided into segments based on application, including benign prostatic hyperplasia, general surgery, and urine incontinence. The market for urinary catheters in 2019 was dominated by the urinary incontinence segment. The greatest CAGR is anticipated for this market segment over the forecast period. The significant share and rapid expansion of this market segment are primarily due to the rising prevalence of obesity, geriatric population increase, and urine incontinence.

Foley catheters are expected to do well in the future

In 2050, there will be more than 2 billion people in the globe who are 60 years of age or older, up from 900 million in 2015, according to the World Health Organization's (WHO) census. Players who produce medical devices like foley catheters are predicted to benefit greatly from this.Through the assessment period, North America is anticipated to dominate the regional market for foley catheters globally. The US's robust healthcare industry and the high levels of medical spending in the region are largely responsible for the region's dominance. Additionally, compared to other locations, the region has a relatively high rate of urinary tract infections. For instance, according to a recent survey, urinary tract infections were the fourth most prevalent infection, accounting for 12.9% of infections in healthcare settings and afflicting 67.7% of these patients.

Urine incontinence afflictions account for the major share of the market

When treating BPH-afflicted men's prostate glands, urinary catheters are most frequently used. According to the American Academy of Family Physicians (AAFP), there were 250,000 BPH operations performed in the United States in 2015, along with about 2 million office visits. This disorder is also linked to pregnancy and may also result from harm or injury to the urethra, penis, or bladder.Urinary catheter use in prostate gland surgery, which accounts for around 37% of total revenue, is still the most lucrative segment of the urinary catheter industry. Urinary incontinence, which is acknowledged to be an underdiagnosed and treatable illness, is second.

Coated catheters held the biggest market share for urinary catheters

The market for urinary catheters is divided into coated and uncoated catheters based on the kind of catheter used. In 2019, coated catheters held the biggest market share for urinary catheters. Additionally, it is anticipated that during the forecast period, this segment will have the greatest CAGR. The multiple benefits of coated catheters, including quicker and more pleasant insertion, a low risk of catheter-associated urinary tract infection, a decreased risk of urethral injury, and higher patient satisfaction, are primarily responsible for this market's rise.

Hospital industry had the biggest market share for urinary catheters' in 2022

Urinary catheters' biggest market share in 2022 belonged to the hospital industry, which was followed by home health and long-term care facilities. For patients with incontinence or other urological problems, hospitals offer a wide range of services; it is projected that this trend would continue during the projection period. The majority of hospitals also include urology departments that commonly use disposable urinary catheters. In the coming years, long-term care institutions are expected to expand at a profitable rate, closely followed by hospitals.

Increase in per capita healthcare spending across the globe give a boost to urinary catheter market

Both established and emerging economies are currently experiencing an increase in per capita healthcare spending, which has enabled the implementation of high-quality patient care choices. Many governments and regulatory agencies are implementing cost-containment strategies to ease the burden of healthcare, particularly in developed nations. Various government and radiation service provider initiatives, such as outcome-based pricing, profit & risk sharing, price regulation, and competitive tendering, have fuelled the transition from a volume-to-value-based system. The value-based healthcare system aids businesses in getting the most out of their healthcare expenditures and enhances outcomes through integrated care pathways, but it also places pricing pressure on manufacturers and reduces investments in R&D for cutting-edge medical treatment technology.

4.5 to 6.8 cases of urinary retention per 1,000 men per year

Similar to this, according to the American Academy of Family Physicians (AAFP), there are 4.5 to 6.8 cases of urinary retention per 1,000 men per year. If the bladder is merely drained, 70% of men will likely experience recurrent urine retention within a week despite the use of foley catheters, necessitating the use of a foley catheter once more. Benign prostatic hyperplasia (BPH), which accounts for roughly 53% of cases of urine retention in males, has been determined to be the main cause in a recent study by the AAPF.

The largest regional market for urinary catheters in 2019 was North America.

North America, Europe, Asia Pacific, and the Rest of the World are the regions that make up the urinary catheters market. The largest regional component of the global market in 2019 was North America, followed by Europe. The market is expanding in North America due to elements including the region's rising geriatric population, high prevalence of diseases, accessibility of cutting-edge interventional devices (such as urinary catheters), and an increase in surgical operations.

Europe is the second largest market for urinary catheters

Europe, which will likely continue to be the second-most lucrative region throughout the assessment period, will follow the US closely. Similar to North America, the region's growth is fueled by the rising prevalence of urinary disorders and government assistance for the creation of cutting-edge medical tools. A WHO survey revealed that indwelling catheterization is linked to a sizable fraction of mortality from urinary infections. Indwelling catheterization increases patient hospital stays, which directly costs the National Health Services €2 billion. High-performing catheters with little side effects are now necessary as a result of this.

Rise in acquisitions and mergers and new products in the urinary catheters market

Manufacturers are constantly working to create innovative goods with a strong emphasis on patient comfort. Recent developments in the global urinary catheters market include fixed occlude devices and an increase in the prevalence of locally established haemodialysis. The market for urinary catheters is exhibiting several trends, including a rise in acquisitions and mergers as well as technological advancements in urinary catheters.

To acquire a competitive advantage, urinary catheter market participants are raising output

The demand for catheterizations is rising as a result of rising rates of neurological diseases, urine incontinence, diabetes, and surgical operations. To acquire a competitive advantage in the healthcare industry, urinary catheter market participants are raising output. To reduce the danger of infection, industry participants in the urinary catheters market should concentrate on creating low-risk, painless, and cosy devices. Companies in the urinary catheters industry should quicken product development and open up new revenue streams to gain an advantage over rivals. By maximising income prospects, manufacturers are able to grow in the market by expanding their online and offline distribution channels in healthcare facilities, pharmacies, and other locations.

Historical & Forecast Period

This study report represents analysis of each segment from 2024 to 2034 considering 2025 as the base year. Compounded Annual Growth Rate (CAGR) for each of the respective segments estimated for the forecast period of 2026 to 2034.

The current report comprises of quantitative market estimations for each micro market for every geographical region and qualitative market analysis such as micro and macro environment analysis, market trends, competitive intelligence, segment analysis, porters five force model, top winning strategies, top investment markets, emerging trends and technological analysis, case studies, strategic conclusions and recommendations and other key market insights.

Research Methodology

The complete research study was conducted in three phases, namely: secondary research, primary research, and expert panel review. key data point that enables the estimation of Urinary Catheters Market By Product, By Applications, By Type, By Gender, By End-Use - Growth, Share, Opportunities & Competitive Analysis, 2025 – 2033 market are as follows:

Market forecast was performed through proprietary software that analyzes various qualitative and quantitative factors. Growth rate and CAGR were estimated through intensive secondary and primary research. Data triangulation across various data points provides accuracy across various analyzed market segments in the report. Application of both top down and bottom-up approach for validation of market estimation assures logical, methodical and mathematical consistency of the quantitative data.

| ATTRIBUTE | DETAILS |

|---|---|

| Research Period | 2024-2034 |

| Base Year | 2025 |

| Forecast Period | 2026-2034 |

| Historical Year | 2024 |

| Unit | USD Million |

| Segmentation | |

Product

|

|

Applications

|

|

Type

|

|

Gender

|

|

End-use

|

|

|

Region Segment (2024-2034; US$ Million)

|

Key questions answered in this report