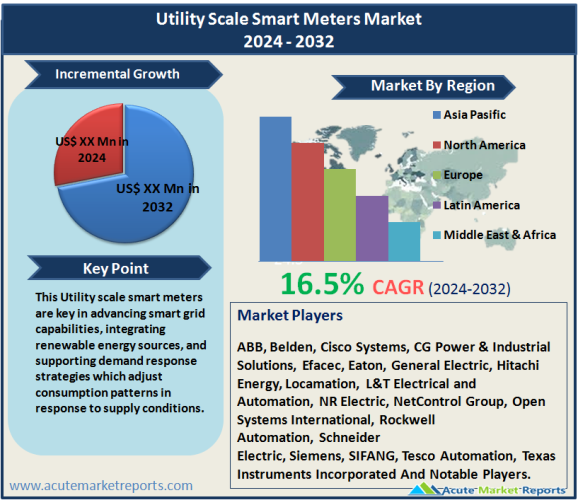

The utility scale smart meters market is expected to grow at a CAGR of 16.5% during the forecast period of 2026 to 2034. Utility scale smart meters, integral components in modern energy management and grid optimization, facilitate the precise measurement and reporting of energy usage from large-scale utility resources. These meters support the transition to a more efficient and flexible energy grid by enabling real-time data transmission between consumers and utility providers. This technology is pivotal for improving energy distribution, optimizing grid operations, and enhancing the responsiveness of utilities to changing load conditions. Utility scale smart meters are key in advancing smart grid capabilities, integrating renewable energy sources, and supporting demand response strategies which adjust consumption patterns in response to supply conditions.

Government Policies and Regulations

Governments worldwide are implementing policies and regulations that mandate or encourage the installation of smart meters. These policies are driven by the need to enhance energy efficiency, reduce carbon footprints, and manage electricity supplies more effectively. For instance, the European Union has set ambitious targets for smart meter coverage as part of its energy efficiency directives, aiming for at least 80% coverage by 2021 in member states. Such regulatory frameworks are crucial in driving the adoption of smart metering solutions across the utility sector, promoting investments and technology upgrades in the infrastructure.

Technological Advancements in Metering Solutions

The rapid development of IoT and communication technologies has significantly enhanced the capabilities of smart meters. Modern meters support advanced features like real-time data processing, remote monitoring, and predictive analytics, enabling utilities to make informed decisions about grid management and maintenance. Innovations such as the integration of AI and machine learning for predictive maintenance and load forecasting further bolster the market growth. These technological enhancements not only improve the functionality of smart meters but also increase their attractiveness to utilities aiming to future-proof their operations.

Increasing Demand for Energy Management Solutions

As global energy consumption rises, so does the need for effective management solutions. Utility scale smart meters play a pivotal role in addressing these needs by providing detailed insights into energy usage patterns and helping to optimize consumption. This is particularly relevant in regions experiencing rapid industrial growth and urbanization, which put additional stress on energy infrastructures. Smart meters help utilities manage loads more efficiently, prevent outages, and ensure reliable service to consumers, driving their adoption in both developed and developing regions.

Restraint

High Initial Investment and Integration Challenges

One significant restraint in the market is the high initial cost associated with deploying utility scale smart meters. These costs include not only the meters themselves but also the associated communication infrastructure and data management systems. Furthermore, integrating these advanced meters with existing utility systems can be complex and resource-intensive. Utilities may face technical challenges in retrofitting old systems with new technologies, which can deter investment in smart metering projects. Despite the long-term benefits of smart meters, these upfront costs and integration challenges can slow down their adoption, particularly in regions with older infrastructure or less financial flexibility.

Market Segmentation by Technology

The utility scale smart meters market is primarily segmented by technology into Advanced Metering Infrastructure (AMI) and Automatic Meter Reading (AMR). AMI technology, offering two-way communication capabilities between the meter and the utility, is anticipated to exhibit the highest Compound Annual Growth Rate (CAGR) due to its enhanced functionality that supports real-time data transmission, remote monitoring, and utility management enhancements. This technology has been pivotal in energy conservation efforts and peak load management, which are critical in regions with stringent energy use regulations. AMI's ability to integrate with home energy management systems further drives its adoption. Conversely, AMR technology, which automates the collection of consumption data from meters to a central database using one-way communication, still captures the highest revenue segment. This prevalence is attributed to its lower cost compared to AMI and its widespread use in mature markets where utilities are gradually transitioning to smarter systems. AMR’s simplicity and reliability make it a preferred choice for regions with less complex utility needs and slower regulatory changes regarding smart grid technologies.

Market Segmentation by Product

Segmentation of the utility scale smart meters market by product includes Smart Gas, Smart Water, and Smart Electric meters. Smart Electric meters are expected to dominate the market both in terms of CAGR and revenue generation. Their widespread adoption is driven by the global push towards energy efficiency and grid modernization. Electric meters are integral to managing electricity supply in residential, commercial, and industrial sectors, making them crucial for energy conservation and management efforts. These meters facilitate precise energy usage tracking, peak time savings indication, and provide utilities with the data needed for demand-side management. On the other hand, Smart Water meters, which help in the detection of leaks and water conservation, and Smart Gas meters, which ensure the safety and efficient management of gas resources, also contribute significantly to the market. However, the pivotal role of electricity in energy transition strategies and the higher cost associated with electric grid management inherently position Smart Electric meters as the segment leader in both growth potential and revenue contribution.

Regional Analysis

The utility scale smart meters market is globally segmented into various regions, including North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa. The Asia Pacific region is anticipated to exhibit the highest Compound Annual Growth Rate (CAGR) during the forecast period of 2026 to 2034, fueled by rapid industrialization, urbanization, and the increasing adoption of smart grid technologies in countries like China, India, and Japan. These nations are heavily investing in energy infrastructure to support their growing economies and urban populations, thus driving demand for advanced metering solutions. Moreover, government initiatives aimed at enhancing energy efficiency and reducing carbon emissions are further propelling the market growth in this region. Conversely, North America is currently the largest revenue-generating region in the utility scale smart meters market. The region's dominance can be attributed to the early adoption of smart technologies, well-established utility infrastructure, and stringent regulatory frameworks mandating the use of smart meters. The presence of leading technology providers and a focus on renewing aging grid infrastructure also significantly contribute to its high revenue share.

Competitive Trends

In terms of competitive trends within the utility scale smart meters market, the landscape is marked by the presence of several key players, including ABB, Belden, Cisco Systems, CG Power & Industrial Solutions, Efacec, Eaton, General Electric, Hitachi Energy, Locamation, L&T Electrical and Automation, NR Electric, NetControl Group, Open Systems International, Rockwell Automation, Schneider Electric, Siemens, SIFANG, Tesco Automation, and Texas Instruments Incorporated. These companies are engaged in fierce competition and are continuously innovating to enhance their market presence. Key strategies employed by these firms include mergers and acquisitions, partnerships, and the development of new technologies that integrate with IoT and cloud computing to offer enhanced metering solutions. For instance, in 2025, General Electric and Schneider Electric reported significant revenue from their smart metering solutions, underscoring their dominant positions in the market. Moving forward, from 2026 to 2034, these players are expected to focus on expanding their geographic reach, especially in high-growth markets such as the Asia Pacific. Investments in R&D are anticipated to remain robust, with a strong emphasis on enhancing the data analytics capabilities of smart meters to offer more comprehensive energy management solutions. Additionally, customization of products to meet local regulations and consumer expectations is likely to be a crucial strategy for sustaining competitive advantage in this evolving market. These strategic initiatives are expected to drive their growth and enable them to capitalize on the increasing global demand for utility scale smart meters, reinforcing their market positions through the forecast period.

Historical & Forecast Period

This study report represents analysis of each segment from 2024 to 2034 considering 2025 as the base year. Compounded Annual Growth Rate (CAGR) for each of the respective segments estimated for the forecast period of 2026 to 2034.

The current report comprises of quantitative market estimations for each micro market for every geographical region and qualitative market analysis such as micro and macro environment analysis, market trends, competitive intelligence, segment analysis, porters five force model, top winning strategies, top investment markets, emerging trends and technological analysis, case studies, strategic conclusions and recommendations and other key market insights.

Research Methodology

The complete research study was conducted in three phases, namely: secondary research, primary research, and expert panel review. key data point that enables the estimation of Utility Scale Smart Meters Market By Technology (AMI, AMR), By Product (Smart Gas, Smart Water, Smart Electric) - Growth, Share, Opportunities & Competitive Analysis, 2026 - 2034 market are as follows:

Market forecast was performed through proprietary software that analyzes various qualitative and quantitative factors. Growth rate and CAGR were estimated through intensive secondary and primary research. Data triangulation across various data points provides accuracy across various analyzed market segments in the report. Application of both top down and bottom-up approach for validation of market estimation assures logical, methodical and mathematical consistency of the quantitative data.

| ATTRIBUTE | DETAILS |

|---|---|

| Research Period | 2024-2034 |

| Base Year | 2025 |

| Forecast Period | 2026-2034 |

| Historical Year | 2024 |

| Unit | USD Million |

| Segmentation | |

Technology

|

|

Product

|

|

|

Region Segment (2024-2034; US$ Million)

|

Key questions answered in this report