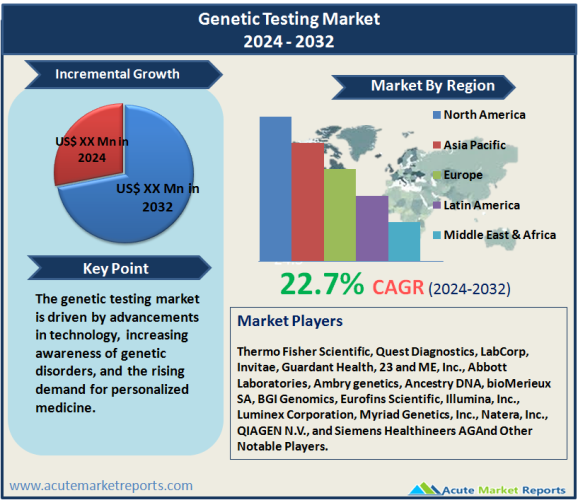

The genetic testing market is expected to grow at a CAGR of 22.7% during the forecast period of 2026 to 2034, driven by advancements in technology, increasing awareness of genetic disorders, and the rising demand for personalized medicine. Genetic testing involves analyzing DNA to identify changes or mutations that may lead to genetic disorders or predispositions to certain health conditions. In 2025, the market generated substantial revenue, largely due to the widespread adoption of next-generation sequencing (NGS) and the growing prevalence of genetic diseases. The market is expected to continue its robust growth from 2026 to 2034, propelled by technological innovations, increased funding for genetic research, and the expansion of direct-to-consumer genetic testing services. North America led the market in terms of revenue, thanks to its advanced healthcare infrastructure and strong investment in genetic research. However, the Asia-Pacific region is expected to register the highest CAGR during the forecast period of 2026 to 2034, fueled by economic growth, improved healthcare systems, and government initiatives in genomic research. Key players like Illumina, Thermo Fisher Scientific, Myriad Genetics, and 23andMe are driving the market through innovation and strategic partnerships, ensuring the continued development and accessibility of genetic testing technologies. Despite the challenges such as regulatory hurdles and ethical concerns, the market is expected to expand, offering new opportunities for improving health outcomes through early diagnosis, personalized treatment plans, and preventive healthcare measures. The comprehensive analysis of market segmentation by technology, application, product, channel, and end-user provides a clear understanding of the current landscape and future trends, highlighting the segments that are expected to lead in revenue generation and growth. Overall, the genetic testing market is set to play a crucial role in the future of healthcare, enabling more accurate diagnoses, better patient management, and the potential for groundbreaking discoveries in genetic research.ey conclusions from this analysis include the dominance of NGS technology in generating revenue, the rising demand for health and wellness genetic testing applications, and the significant role of online channels in distributing genetic tests.

Technological Advancements in genetic testing

Technological advancements have been a major driver of the genetic testing market. Next-generation sequencing (NGS) has revolutionized genetic testing by allowing the rapid and cost-effective sequencing of entire genomes. Companies like Illumina and Thermo Fisher Scientific have developed advanced NGS platforms that provide high accuracy and throughput, making genetic testing more accessible and affordable. NGS has enabled the identification of genetic mutations associated with a wide range of diseases, from rare genetic disorders to common conditions like cancer and cardiovascular diseases. The integration of NGS with bioinformatics tools has further enhanced the ability to interpret complex genetic data, leading to more accurate diagnoses and personalized treatment plans. For example, Illumina'sNovaSeq platform has been instrumental in large-scale genomic projects, such as the 100,000 Genomes Project in the UK, which aims to sequence 100,000 genomes to improve understanding of rare diseases and cancer. Another technological advancement driving the market is the development of CRISPR-Cas9 gene-editing technology, which allows precise modification of DNA sequences. While still in the research phase for many applications, CRISPR has shown promise in correcting genetic mutations that cause diseases, potentially leading to new treatments and preventive strategies. Companies like Editas Medicine and CRISPR Therapeutics are at the forefront of developing CRISPR-based therapies, which could significantly impact the genetic testing market by providing new diagnostic and therapeutic options. Additionally, the advent of digital PCR (dPCR) has improved the sensitivity and precision of genetic testing, particularly for detecting low-frequency mutations and monitoring minimal residual disease in cancer patients. Bio-Rad Laboratories and Thermo Fisher Scientific have developed dPCR platforms that are widely used in clinical and research settings. These technological advancements are expected to continue driving the growth of the genetic testing market, enabling more comprehensive and precise genetic analyses.

Increasing Awareness and Prevalence of Genetic Disorders

The increasing awareness and prevalence of genetic disorders are significant drivers of the genetic testing market. Genetic disorders affect millions of people worldwide, and early diagnosis through genetic testing can lead to better management and treatment outcomes. Public awareness campaigns and educational initiatives by organizations like the Genetic Alliance and the National Society of Genetic Counselors have played a crucial role in promoting the importance of genetic testing. These efforts have led to increased demand for genetic tests for a wide range of conditions, including inherited cancers, cardiovascular diseases, and rare genetic disorders. For instance, BRCA1 and BRCA2 gene mutations are associated with a higher risk of breast and ovarian cancers. Genetic testing for these mutations can help individuals understand their risk and take preventive measures, such as increased surveillance or prophylactic surgeries. Companies like Myriad Genetics offer BRCA testing, and their tests have been widely adopted in clinical practice. Similarly, genetic testing for Lynch syndrome, an inherited condition that increases the risk of colorectal cancer, has become more common. Identifying individuals with Lynch syndrome through genetic testing allows for targeted screening and early intervention, improving patient outcomes. Another factor contributing to the increasing prevalence of genetic disorders is the rise in the global incidence of chronic diseases with genetic components, such as diabetes, hypertension, and autoimmune disorders. Genetic testing can identify individuals at risk for these conditions, enabling early intervention and personalized treatment plans. For example, genetic testing for HLA-B27 can help diagnose ankylosing spondylitis, an autoimmune disorder that affects the spine. The growing prevalence of genetic disorders, coupled with increased public awareness, is driving the demand for genetic testing services.

Growing Demand for Personalized Medicine

The growing demand for personalized medicine is a major driver of the genetic testing market. Personalized medicine, also known as precision medicine, involves tailoring medical treatment to the individual characteristics of each patient, including their genetic profile. Genetic testing plays a crucial role in personalized medicine by providing insights into an individual's genetic makeup, which can inform treatment decisions and improve patient outcomes. Pharmacogenomics, the study of how genes affect a person's response to drugs, is a key component of personalized medicine. Genetic testing can identify genetic variations that influence drug metabolism, efficacy, and safety, allowing healthcare providers to select the most appropriate medications and dosages for each patient. For example, genetic testing for CYP2C9 and VKORC1 variants can guide the dosing of warfarin, a commonly used anticoagulant, reducing the risk of adverse effects and improving therapeutic outcomes. Companies like 23andMe and Invitae offer pharmacogenomic testing services that are integrated into clinical practice, helping physicians make informed decisions about drug therapy. Another area where genetic testing is driving personalized medicine is oncology. Genetic testing can identify specific mutations in cancer cells, enabling the use of targeted therapies that are more effective and have fewer side effects compared to traditional treatments. For instance, genetic testing for EGFR mutations in non-small cell lung cancer can identify patients who are likely to benefit from EGFR inhibitors like erlotinib and gefitinib. Companies like Foundation Medicine and Guardant Health offer comprehensive genomic profiling tests that identify actionable mutations in cancer patients, guiding treatment decisions and improving patient outcomes. Additionally, genetic testing is being used to identify individuals at risk for hereditary conditions, allowing for preventive measures and early intervention. For example, genetic testing for familial hypercholesterolemia, a genetic disorder that causes high cholesterol levels, can identify individuals at risk for early-onset cardiovascular disease. Early diagnosis and treatment can significantly reduce the risk of heart attacks and strokes in these individuals. The growing demand for personalized medicine, driven by the ability of genetic testing to provide actionable insights into an individual's health, is a significant driver of the genetic testing market.

Restraint

Ethical and Privacy Concerns

Despite the significant benefits of genetic testing, ethical and privacy concerns pose a major restraint to the market. Genetic testing involves the collection, storage, and analysis of sensitive genetic information, which raises concerns about data privacy and security. Individuals may be reluctant to undergo genetic testing due to fears that their genetic information could be misused by third parties, such as employers, insurance companies, or government agencies. The potential for genetic discrimination, where individuals are treated unfairly based on their genetic information, is a significant concern. For example, individuals with a genetic predisposition to certain diseases may face challenges in obtaining health insurance or employment if their genetic information is disclosed. While laws such as the Genetic Information Nondiscrimination Act (GINA) in the United States provide some protection against genetic discrimination, concerns about data privacy and security persist. Additionally, the storage and sharing of genetic data in databases and biobanks pose risks of data breaches and unauthorized access. High-profile data breaches in recent years have heightened public awareness and concern about the security of personal information, including genetic data. Companies offering genetic testing services must implement robust data security measures to protect genetic information and maintain public trust. Another ethical concern is the potential psychological impact of genetic testing. The results of genetic tests can reveal information about an individual's risk for certain diseases, which may cause anxiety, stress, or emotional distress. For example, individuals who learn that they carry a mutation associated with a high risk of cancer may experience a significant psychological burden. Genetic counseling is essential to help individuals understand their test results and make informed decisions about their health. However, access to genetic counseling services may be limited, particularly in low-resource settings, posing a barrier to the widespread adoption of genetic testing. The ethical and privacy concerns associated with genetic testing are significant restraints that need to be addressed to ensure the responsible and equitable use of genetic information.

Market Segmentation by Technology

In 2025, next-generation sequencing (NGS) generated the highest revenue in the genetic testing market. NGS technology allows for the rapid and cost-effective sequencing of entire genomes, making it the preferred choice for many genetic testing applications. Companies like Illumina and Thermo Fisher Scientific have developed advanced NGS platforms that provide high accuracy and throughput, enabling comprehensive genetic analyses. The ability to sequence multiple genes simultaneously and identify genetic mutations associated with various diseases has driven the adoption of NGS in clinical and research settings. The NGS segment is expected to continue its dominance, registering the highest CAGR during the forecast period of 2026 to 2034. The ongoing advancements in NGS technology, including the development of more efficient sequencing methods and reduced costs, are driving the growth of this segment. Additionally, the increasing use of NGS for personalized medicine, cancer genomics, and rare disease diagnosis is expected to further boost its adoption. In contrast, array technology, while significant, generated lower revenue in 2025 compared to NGS. However, it is also expected to witness substantial growth during the forecast period. Array technology is widely used for genotyping, gene expression profiling, and detecting copy number variations. Companies like Affymetrix (now part of Thermo Fisher Scientific) and Illumina offer array-based genetic testing solutions that are used in various applications, including pharmacogenomics and ancestry testing. The ability to analyze large numbers of genetic variants simultaneously and the lower cost compared to NGS make array technology a valuable tool in genetic testing. PCR-based testing, fluorescence in situ hybridization (FISH), and other technologies also play important roles in the genetic testing market. PCR-based testing is widely used for detecting specific genetic mutations, such as those associated with infectious diseases and inherited disorders. FISH is used for identifying chromosomal abnormalities and gene rearrangements, particularly in cancer diagnostics. While these technologies generated lower revenue in 2025 compared to NGS, they remain essential for specific genetic testing applications and are expected to see continued growth during the forecast period.

Market Segmentation by Application

In 2025, health and wellness genetic testing applications, which include predisposition/risk/tendency testing, generated the highest revenue in the genetic testing market. The increasing awareness of the role of genetics in health and the growing demand for personalized health insights have driven the adoption of health and wellness genetic tests. Companies like 23andMe and AncestryDNA offer direct-to-consumer genetic testing services that provide individuals with information about their genetic predisposition to various health conditions, such as cardiovascular diseases, diabetes, and certain cancers. These tests enable individuals to make informed decisions about their health and lifestyle, leading to better health outcomes. The health and wellness segment is expected to continue its dominance, registering the highest CAGR during the forecast period of 2026 to 2034. The rising demand for preventive healthcare and personalized medicine, coupled with advancements in genetic testing technologies, is driving the growth of this segment. Genetic disease carrier status testing also generated substantial revenue in 2025. Carrier testing helps identify individuals who carry a genetic mutation that could be passed on to their offspring, leading to genetic disorders. This type of testing is particularly important for couples planning to start a family, as it provides valuable information for making informed reproductive decisions. Companies like Counsyl (now part of Myriad Genetics) offer carrier screening tests for a wide range of genetic conditions, such as cystic fibrosis, spinal muscular atrophy, and Tay-Sachs disease. New baby screening, which includes newborn genetic testing for inherited disorders, also plays a significant role in the genetic testing market. Early diagnosis of genetic disorders through newborn screening allows for timely intervention and treatment, improving the health outcomes of affected infants. Programs like the Newborn Screening Program in the United States mandate the screening of all newborns for certain genetic conditions, driving the demand for newborn genetic testing. Ancestry and ethnicity testing, while popular, generated lower revenue in 2025 compared to health and wellness and genetic disease carrier status testing. However, this segment is also expected to witness growth during the forecast period, driven by the increasing interest in genealogy and the growing availability of affordable ancestry testing kits. Companies like 23andMe and AncestryDNA dominate this segment, offering comprehensive ancestry reports based on genetic data.

Market Segmentation by Product

In 2025, consumables generated the highest revenue in the genetic testing market. Consumables, including reagents, kits, and other laboratory supplies, are essential for performing genetic tests. The continuous demand for consumables in research and clinical laboratories, coupled with the increasing number of genetic tests being conducted, drives the revenue of this segment. Companies like Illumina, Thermo Fisher Scientific, and Qiagen offer a wide range of consumables for various genetic testing applications, including next-generation sequencing, PCR-based testing, and array technology. The consumables segment is expected to maintain its dominance, registering the highest CAGR during the forecast period of 2026 to 2034. The ongoing advancements in genetic testing technologies and the increasing adoption of genetic testing in clinical practice and research are expected to drive the demand for consumables. Equipment, which includes genetic testing instruments and platforms, also generated significant revenue in 2025. The growing adoption of advanced genetic testing technologies, such as next-generation sequencing and digital PCR, drives the demand for equipment. Companies like Illumina, Thermo Fisher Scientific, and Bio-Rad Laboratories provide cutting-edge genetic testing instruments that enable high-throughput and accurate genetic analyses. The continuous innovation in genetic testing equipment and the need for upgrading existing platforms to meet the increasing demand for genetic testing is expected to drive the growth of this segment. Software and services, while generating lower revenue in 2025 compared to consumables and equipment, play a crucial role in the genetic testing market. The interpretation of complex genetic data requires advanced bioinformatics tools and software solutions. Companies like Illumina and Thermo Fisher Scientific offer comprehensive bioinformatics platforms that facilitate the analysis and interpretation of genetic data. Additionally, genetic testing service providers, such as 23andMe and Invitae, offer genetic counseling and consultation services to help individuals understand their test results and make informed decisions about their health. The software and services segment is expected to witness substantial growth during the forecast period, driven by the increasing complexity of genetic data and the need for accurate data interpretation.

Market Segmentation by Channel

In 2025, the online channel generated the highest revenue in the genetic testing market. The convenience and accessibility of online genetic testing services have led to the widespread adoption of this distribution channel. Companies like 23andMe and AncestryDNA offer direct-to-consumer genetic testing kits that can be purchased online, allowing individuals to collect samples at home and receive test results through online platforms. The growing demand for personalized health insights and the increasing use of digital health platforms are driving the growth of the online channel. The online channel is expected to maintain its dominance, registering the highest CAGR during the forecast period of 2026 to 2034. The continuous advancements in digital health technologies and the expanding availability of online genetic testing services are expected to further boost the adoption of this distribution channel. The offline channel, which includes hospitals, clinics, and diagnostic laboratories, also generated substantial revenue in 2025. Traditional healthcare settings play a crucial role in genetic testing, particularly for diagnostic and clinical applications. Healthcare providers often order genetic tests for patients based on clinical indications, such as suspected genetic disorders or family history of inherited conditions. Diagnostic laboratories, such as Quest Diagnostics and LabCorp, offer a wide range of genetic testing services that are integrated into clinical practice. While the offline channel generated lower revenue in 2025 compared to the online channel, it remains essential for clinical genetic testing and is expected to see continued growth during the forecast period.

Market Segmentation by End-User

In 2025, hospitals and clinics generated the highest revenue in the genetic testing market. Hospitals and clinics are primary points of care for patients, and healthcare providers often order genetic tests as part of the diagnostic process. Genetic testing in hospitals and clinics is essential for diagnosing inherited disorders, guiding treatment decisions, and providing personalized medical care. The integration of genetic testing into routine clinical practice and the increasing number of genetic tests being performed in hospitals and clinics drive the revenue of this segment. The hospitals and clinics segment is expected to maintain its dominance, registering the highest CAGR during the forecast period of 2026 to 2034. The ongoing advancements in genetic testing technologies and the increasing adoption of genetic testing in clinical settings are expected to drive the growth of this segment. Diagnostic laboratories, which include commercial and academic laboratories, also generated significant revenue in 2025. Diagnostic laboratories play a crucial role in performing genetic tests ordered by healthcare providers. Companies like Quest Diagnostics, LabCorp, and Invitae offer a wide range of genetic testing services, including NGS, PCR-based testing, and array technology. The growing demand for genetic testing and the increasing complexity of genetic analyses drive the demand for diagnostic laboratory services. The diagnostic laboratories segment is expected to see substantial growth during the forecast period, driven by the increasing number of genetic tests being conducted and the need for specialized laboratory services. Other end-users, including research institutions and academic centers, also contribute to the genetic testing market. Research institutions conduct genetic testing as part of scientific studies and clinical trials, driving the demand for genetic testing technologies and services. Academic centers play a crucial role in advancing genetic research and training the next generation of geneticists and healthcare providers. While the revenue generated by this segment in 2025 was lower compared to hospitals clinics and diagnostic laboratories, it remains an important part of the genetic testing market and is expected to see continued growth during the forecast period.

Geographic Trends

In 2025, North America generated the highest revenue in the genetic testing market. The region's dominance is attributed to the high adoption of advanced genetic testing technologies, the presence of major genetic testing companies, and the strong emphasis on personalized medicine. The United States, in particular, has a well-established healthcare infrastructure and significant investment in genetic research, driving the growth of the genetic testing market. Companies like Illumina, Thermo Fisher Scientific, and 23andMe are based in North America and play a leading role in developing and commercializing genetic testing products and services. The high prevalence of genetic disorders and the increasing demand for personalized healthcare further contribute to the region's revenue. However, the Asia-Pacific region is expected to register the highest CAGR during the forecast period of 2026 to 2034. The rapid economic growth, improved healthcare infrastructure, and increasing awareness of genetic disorders in countries like China and India are driving the demand for genetic testing. Governments in the region are also investing in genomic research and precision medicine initiatives, further boosting the adoption of genetic testing technologies. For example, China's Precision Medicine Initiative aims to advance genomic research and integrate genetic testing into clinical practice, driving the growth of the genetic testing market in the region. The Asia-Pacific region's large population and the growing prevalence of genetic diseases also contribute to the expected growth. Europe, while generating lower revenue compared to North America and Asia-Pacific, remains an important market for genetic testing. The region has a well-established healthcare system and significant investment in genetic research and personalized medicine. Countries like the United Kingdom, Germany, and France are leading in the adoption of genetic testing technologies and services. The increasing prevalence of genetic disorders and the growing demand for personalized healthcare drive the growth of the genetic testing market in Europe. Other regions, including Latin America and the Middle East & Africa, are also witnessing growth in the genetic testing market, driven by improving healthcare infrastructure and increasing awareness of genetic disorders.

Competitive Trends

The genetic testing market is highly competitive, with key players driving innovation and commercialization of advanced genetic testing products and services. In 2025, Illumina dominated the market with its cutting-edge next-generation sequencing platforms, which are widely used in clinical and research settings. The company's NovaSeq and MiSeq platforms have set industry standards for high-throughput and accurate genetic sequencing, enabling comprehensive genomic analyses. Illumina's strategic partnerships and acquisitions, such as its acquisition of Pacific Biosciences, have further strengthened its market position. Thermo Fisher Scientific is another major player, offering a wide range of genetic testing technologies, including NGS, PCR, and array-based solutions. The company's Ion Torrent NGS platforms and Applied Biosystems PCR systems are widely used for genetic testing applications. Thermo Fisher's acquisition of Affymetrix expanded its array-based testing capabilities, further enhancing its product portfolio. Myriad Genetics is a leader in genetic testing for hereditary cancers, offering tests for BRCA1 and BRCA2 mutations and other genetic conditions. The company's MyRisk Hereditary Cancer test is widely used in clinical practice, helping individuals understand their genetic risk for cancer. Myriad's strategic focus on expanding its test offerings and geographic reach has contributed to its strong market presence. 23andMe is a prominent player in the direct-to-consumer genetic testing market, offering health and ancestry testing services. The company's user-friendly test kits and comprehensive reports have made genetic testing accessible to a broad consumer base. 23andMe's extensive genetic database and research collaborations also provide valuable insights into genetic associations with various health conditions. Other notable players in the genetic testing market include Quest Diagnostics, LabCorp, Invitae, Guardant Health, 23 and ME, Inc., Abbott Laboratories, Ambry genetics, Ancestry DNA, bioMerieux SA, BGI Genomics, Eurofins Scientific, Illumina, Inc., Luminex Corporation, Myriad Genetics, Inc., Natera, Inc., QIAGEN N.V., and Siemens Healthineers AG. These companies offer a wide range of genetic testing services, from diagnostic testing to comprehensive genomic profiling. Strategic partnerships, acquisitions, and investments in research and development are key strategies employed by these companies to strengthen their market positions and expand their product offerings. The competitive landscape of the genetic testing market is characterized by continuous innovation and a strong emphasis on advancing genetic testing technologies to improve healthcare outcomes.

Historical & Forecast Period

This study report represents analysis of each segment from 2024 to 2034 considering 2025 as the base year. Compounded Annual Growth Rate (CAGR) for each of the respective segments estimated for the forecast period of 2026 to 2034.

The current report comprises of quantitative market estimations for each micro market for every geographical region and qualitative market analysis such as micro and macro environment analysis, market trends, competitive intelligence, segment analysis, porters five force model, top winning strategies, top investment markets, emerging trends and technological analysis, case studies, strategic conclusions and recommendations and other key market insights.

Research Methodology

The complete research study was conducted in three phases, namely: secondary research, primary research, and expert panel review. key data point that enables the estimation of Genetic Testing Market By Technology (Next Generation Sequencing, Array Technology, PCR-based Testing, FISH, Others), By Application (Ancestry & Ethnicity, Traits Screening, Genetic Disease Carrier Status, New Baby Screening, Health and Wellness-Predisposition/Risk/Tendency), By Product (Consumables, Equipment, Software & Services), By Channel (Online, Offline), By End-User (Hospitals & Clinics, Diagnostic Laboratories, Others) - Growth, Share, Opportunities & Competitive Analysis, 2026 - 2034 market are as follows:

Market forecast was performed through proprietary software that analyzes various qualitative and quantitative factors. Growth rate and CAGR were estimated through intensive secondary and primary research. Data triangulation across various data points provides accuracy across various analyzed market segments in the report. Application of both top down and bottom-up approach for validation of market estimation assures logical, methodical and mathematical consistency of the quantitative data.

| ATTRIBUTE | DETAILS |

|---|---|

| Research Period | 2024-2034 |

| Base Year | 2025 |

| Forecast Period | 2026-2034 |

| Historical Year | 2024 |

| Unit | USD Million |

| Segmentation | |

Technology

|

|

Application

|

|

Product

|

|

Channel

|

|

End-User

|

|

|

Region Segment (2024-2034; US$ Million)

|

Key questions answered in this report